Why Capital One Closes Credit Cards Without Warning

Jun 29, 2026

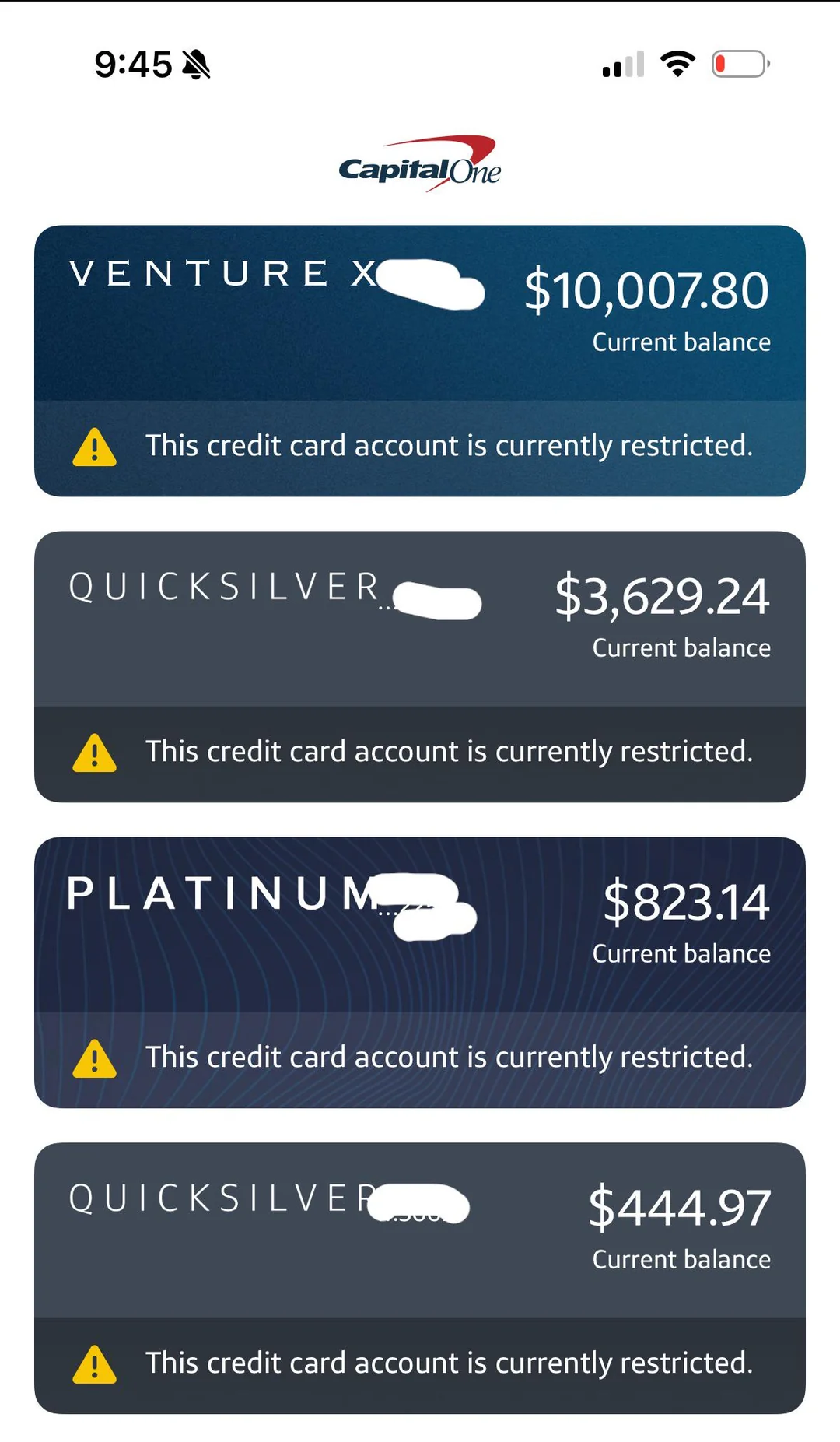

Capital One is closing credit cards without warning, and a lot of people are only finding out after their accounts are already frozen or shut down.

Imagine opening your banking app like you always do.

Then you realize every Capital One card you own is gone.

Tens of thousands in available credit wiped out overnight.

No missed payment with Capital One.

No warning call.

No long explanation.

Just closed.

That is the part that scares people.

And the worst part is that sometimes the behavior that gets flagged looks responsible from your side.

Paying aggressively.

Moving fast.

Keeping old cards open but unused.

Fixing a payment mistake right away.

From your point of view, you are doing the right thing.

From Capital One’s point of view, it can look like risk.

Quick Answer

Capital One may close credit cards because of credit cycling, returned payments, new negative information on your credit report, suspicious activity, or long-term inactivity. Returned payments are one of the biggest red flags because they can make the bank think you have liquidity stress, even if it was an honest mistake. Capital One can also reduce limits or close inactive accounts, and a closed card can hurt your utilization if you lose available credit.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

1. Credit Cycling

Credit cycling is one of the fastest ways to get flagged.

And most people do not even realize they are doing it.

Here is what it looks like.

You have a $5,000 credit limit.

You spend close to $5,000.

Then you pay it off quickly.

Then you spend another $5,000 during the same billing cycle.

From your side, this looks responsible.

You paid fast.

You avoided interest.

You managed cash flow.

But from the bank’s side, it can look like you spent $10,000 on a $5,000 approval.

That is the problem.

Banks approve you for a certain exposure level. When you repeatedly run balances up and down inside the same cycle, it can look like you are bypassing the limit they gave you.

Why Credit Cycling Looks Risky

Credit cycling can trigger concern for a few reasons.

First, rewards payouts can spike.

If you are earning rewards on spend that is way above your approved limit, the bank may question whether the account is being used the way they intended.

Second, fraud systems may start watching.

High-volume spending, fast paydowns, and repeated reuse of the same credit line can look like suspicious money movement.

That does not mean you are doing anything illegal.

But fraud systems do not always start with your intentions.

They start with patterns.

And if the pattern looks risky, the account can get reviewed.

Sometimes that review leads to a warning.

Sometimes it leads to a limit cut.

Sometimes it leads to a shutdown.

Even if every payment was made on time.

How to Avoid Credit Cycling Problems

The cleanest move is simple:

Do not repeatedly max out and pay down the same card in one billing cycle unless you are comfortable with the risk.

If you need to make a large purchase, consider:

-

Calling Capital One before the purchase

-

Splitting the purchase across cards

-

Requesting a credit limit increase first

-

Waiting for the statement to close before reusing the limit heavily

-

Using a card with a higher limit

-

Using a business card if the expense is for business

The goal is to avoid making a $5,000 limit look like a $15,000 spending account.

Banks do not love that.

2. New Negative Information on Your Credit Report

Capital One does not only look at your Capital One account.

They can also monitor your broader credit profile.

That means a problem with another lender can still affect your Capital One relationship.

A missed payment somewhere else.

A new collection.

A charge-off.

A sudden score drop.

Even a credit report error that has not been fixed yet.

Capital One may see that and decide your risk has changed.

And once the bank thinks your risk has changed, it may reduce exposure.

That can mean:

-

Lower credit limits

-

Frozen accounts

-

Closed cards

-

No new approvals

-

Fewer upgrade or increase options

This is why I always tell people to monitor all three credit reports.

Not just the card you are worried about.

Universal Default: The Brutal Logic Behind It

A couple years ago, I covered an interview with a senior bank underwriter, and they mentioned something most people have never heard of.

It is called universal default.

The idea is simple but brutal.

If one lender sees signs of trouble, other lenders may assume they could be next.

So a missed payment on Card A can trigger action on Card B, even if Card B has never been late.

That is why one late payment can create a chain reaction.

Capital One may not care that the late payment was not with them.

Their logic is:

“If this borrower is struggling somewhere else, we might be next.”

So they reduce risk before they take the loss.

That can feel unfair.

But from the bank’s side, it is risk management.

3. Returned Payments

Returned payments are the one people underestimate.

A returned payment happens when a payment gets drafted but does not go through.

Maybe the money had not settled yet.

Maybe you selected the wrong bank account.

Maybe autopay pulled from an account that was empty.

Maybe you moved money too late.

From your side, it feels like a mistake.

From the bank’s side, it can look like one of the strongest risk signals possible.

Because a returned payment tells the bank:

“This person tried to pay, but the money was not there.”

That is different from just paying close to the due date.

A clean payment is one thing.

A bounced payment is another.

Why Capital One May React So Fast

A returned payment is not just treated like a normal late payment.

It can look like a failed attempt to pay.

And once that happens, Capital One may not only look at the one card where the payment bounced.

They may reevaluate your entire relationship.

That is why people sometimes lose multiple Capital One cards after one payment issue.

Even if:

-

The payment was fixed quickly

-

The customer was never 30 days late

-

The account had years of history

-

The mistake was caused by autopay

-

The wrong bank account was selected

-

The customer paid manually right after

Capital One may still see liquidity stress.

And banks act fast on liquidity stress.

Real Returned Payment Data Points

One Reddit user described an autopay situation where the payment pulled from an empty account. They fixed the payment, but Capital One reportedly closed all four of their cards without warning, including older accounts.

A community member named Derrek shared a similar situation.

He had multiple accounts linked to his Capital One Platinum and Secured Platinum. When he paid the bills, the wrong account autofilled. He did not catch it. Both payments were returned.

He paid them from the correct account as soon as he received the email.

A couple days later, both accounts were closed.

That is the part people do not expect.

You can fix the payment and still lose the relationship.

Do Not Force Payments

This is why I always say:

Do not force payments.

An early payment that bounces is worse than a clean payment that posts on time.

If you use autopay, make sure the money is already sitting in the account.

Not “it should be there by tomorrow.”

Not “the transfer is pending.”

Actually there.

If cash flow is tight, do not let autopay guess for you.

Manually manage the payment.

Confirm the funds.

Then pay.

Returned payments do not look like accidents to banks.

They look like high risk.

4. Inactivity

This one catches people off guard because inactivity feels safe.

You get better cards.

Better rewards.

Lower interest.

Higher limits.

So you take the old Capital One card and put it in the sock drawer.

No harm, right?

Not always.

Capital One says if you do not use a credit card for a period of time, the issuer may reduce your limit or close the account due to inactivity.

That means doing “nothing” can still create a problem.

From your side, you are avoiding debt.

From Capital One’s side, the account is unproductive risk.

They have a credit line open.

They are taking on exposure.

But they are earning nothing from the account.

No swipe fees.

No interest.

No annual fee, depending on the card.

At some point, the bank may decide the line is not worth keeping open.

Why Inactivity Closures Can Hurt

When an inactive card closes, the damage is not always obvious right away.

But it can affect your credit profile in a few ways.

Your total available credit drops.

Your utilization can jump.

Your account mix may change.

Your average age of accounts may eventually be affected.

That is why people sometimes see their score dip after an old card closes.

The biggest immediate issue is usually utilization.

For example, if you had $50,000 in total limits and Capital One closes a $10,000 card, you just lost 20% of your available credit.

If your balances stay the same, your utilization goes up.

That can hurt.

How to Keep Old Cards Alive

You do not need to spend heavily on an old card.

You just need to keep it active.

The easiest strategy is to put one small recurring charge on it.

Something like:

-

Streaming service

-

Gym membership

-

Cloud storage

-

Phone bill

-

Small subscription

-

Gas purchase every few months

Then set autopay to pay the statement balance in full.

But remember the returned payment warning.

Autopay is only safe if the linked bank account always has funds.

A $7 subscription is enough to keep a card active.

A bounced $7 autopay can create a much bigger problem.

The Hidden Problem: Capital One Looks at the Whole Relationship

One thing people need to understand about Capital One is that they do not always evaluate one card in isolation.

A problem on one account can affect the relationship.

That is why returned payments are so dangerous.

That is why credit report changes matter.

That is why suspicious activity can create a broader review.

If Capital One decides the borrower is risky, it may reduce exposure across multiple cards.

That is what makes shutdowns feel so brutal.

You think you have four separate cards.

Capital One may see one relationship.

And if the relationship looks risky, they can move across the board.

What to Do If Capital One Closes Your Card

If Capital One closes your card, move quickly.

First, find out why.

Call and ask for the closure reason.

You may not get a full explanation, but get whatever information they will give you.

Second, check whether the account can be reopened.

Capital One says there are very few exceptions where a closed account can be reopened, so you should treat closure as close to permanent.

Third, protect your rewards.

If your account is suspended, restricted, delinquent, defaulted, or closed, your redemption options may change, and you may lose unredeemed rewards.

Fourth, watch your utilization.

If the closure removes a large limit, your score may drop because your utilization increased.

Fifth, stop applying emotionally.

Do not panic-apply for three new cards the same day.

Figure out the reason first.

Then choose the next move.

Helpful resource: If Capital One shuts you down or keeps denying you, my 9 Credit Cards That Reveal Your Starting Limit Before Approval can help you research cards where you may be able to see your limit before fully committing.

How to Reduce the Risk of a Capital One Shutdown

Here is the simple checklist.

Do not cycle your limit aggressively.

Do not let payments bounce.

Do not ignore old cards for years.

Do not assume Capital One only watches your Capital One payment history.

Do not leave credit report errors sitting there.

Do not run suspicious-looking activity through a personal card.

Do not make rapid, unusual payment and spending patterns without a reason.

Do not use autopay from an account that might be empty.

And if you are going to make a large purchase or unusual payment, think before you swipe.

Capital One is not impossible to work with.

But they can be quick to reduce risk.

That is the game.

What I Would Do Instead

If you want to keep your Capital One relationship healthy, I would do this:

-

Use each card at least occasionally

-

Keep one small recurring charge on older cards

-

Pay from a bank account that always has enough money

-

Avoid repeated max-pay-max-pay cycles

-

Keep utilization low across all cards

-

Monitor all three credit reports

-

Fix credit report errors fast

-

Keep backup cards with other issuers

-

Redeem rewards instead of letting huge balances sit forever

-

Do not rely on one bank for all your available credit

That last point is important.

Never let one issuer control your whole credit life.

If Capital One closes your cards and that wipes out most of your available credit, you were too concentrated.

Diversify your lenders.

Helpful resource: Before applying for another card, my Free Credit Card & Loan Pre-Approval Master List can help you check soft-pull pre-approval options before risking more hard inquiries.

Frequently Asked Questions

Why did Capital One close my credit card?

Capital One may close a credit card because of inactivity, returned payments, suspected fraud, new negative information on your credit report, credit risk, or account behavior that violates internal risk rules. The exact reason depends on your account.

Can Capital One close all my cards at once?

Yes, it can happen. If Capital One sees a serious risk signal, it may review the broader relationship, not just one card. Returned payments and suspicious activity are two situations where multiple accounts can be affected.

What is credit cycling?

Credit cycling is when you spend close to your credit limit, pay it down quickly, then spend close to the limit again in the same billing cycle. It can make your spending look much higher than the limit Capital One approved.

Will Capital One close my card for inactivity?

It can. Capital One says credit card issuers may reduce limits or close inactive accounts after a period of non-use. There is no universal timeline, so it is smart to use old cards occasionally.

Can a returned payment get my Capital One account closed?

Yes, based on data points, returned payments can lead to Capital One closures, sometimes across multiple cards. Even if you fix the payment quickly, the returned payment can still be treated as a serious risk signal.

Can a closed Capital One card be reopened?

Sometimes people try, but Capital One says there are very few exceptions where a closed account can be reopened. Treat closure as likely permanent unless Capital One tells you otherwise.

Conclusion

Capital One shutdowns feel random, but they usually come down to risk.

Credit cycling can make you look like you are bypassing your approved limit.

New negative information can make Capital One think another lender’s problem may become their problem next.

Returned payments can make the bank think you are under liquidity stress.

Inactivity can make your credit line look like unproductive risk.

The move is not to live in fear.

The move is to understand the patterns.

Use your cards.

Pay cleanly.

Avoid bounced payments.

Do not cycle limits aggressively.

Monitor your credit.

And do not keep all your available credit with one bank.

Because when a bank shuts down a card, the account may be gone in seconds.

But the damage to your credit profile can last much longer.