Why Banks Are Closing Credit Card Accounts Right Now

Jun 29, 2026

What if you did everything right.

You pay on time. You keep your balances under control. You avoid late payments. Then one day, the bank shuts down your credit card anyway.

No big warning. No dramatic phone call. Just an account closure, a lower credit limit, or a letter telling you the relationship changed.

That sounds random, but it usually is not.

Banks are watching the economy, your credit report, your payment behavior, your balances, your cash flow, and their own risk exposure. And right now, the data shows lenders are getting more cautious, even while some borrowers are still getting approved.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Banks are closing more credit accounts because consumer debt is high, delinquencies are elevated, and lenders are trying to reduce risk before things get worse. The New York Fed reported that lender-initiated account closures rose to 9.1%, a new series high, while credit rejection rates actually dropped to 15.9%. That means strong borrowers can still get approved, but banks are quietly cutting accounts and limits where their risk models see trouble. (Federal Reserve Bank of New York)

The Credit Data Looks Good at First

The latest New York Fed credit access data looks positive if you only read the headline.

Credit applications rose to their highest level since October 2022, and the overall rejection rate dropped to 15.9%, the lowest level since June 2021. That sounds like banks are opening the approval gates again. (Federal Reserve Bank of New York)

But buried inside that same report is the part people need to pay attention to:

9.1% of respondents said a lender closed one of their accounts in the past 12 months.

That was a new series high.

So yes, more people are getting approved. But at the same time, banks are also closing accounts they do not want on their books anymore.

That is the confusing part.

The front door looks open. The back door is where the risk cuts are happening.

Why Banks Are Tightening Behind the Scenes

Banks do not wait until everything breaks.

They adjust early.

Right now, lenders are looking at a consumer credit market with a lot of pressure building up.

New York Fed data showed total household debt at $18.794 trillion in Q1 2026. Credit card balances stood at $1.252 trillion after a seasonal decline, and 4.8% of outstanding household debt was in some stage of delinquency. Student loan delinquency also moved higher, with 10.3% of balances 90+ days delinquent. (Federal Reserve Bank of New York)

That is not a small issue.

And it lines up with another major warning sign: a separate analysis from The Century Foundation and Protect Borrowers estimated that about 111 million Americans cannot pay their credit card balances in full each month. (The Century Foundation)

That is why banks are nervous.

When more people carry balances, request credit limit increases, and have less emergency cash available, banks start asking a simple question:

Is this normal credit usage, or is this financial stress?

Why Approvals Can Be Easier While Accounts Get Closed

This is the part most people miss.

Credit tightening does not always look like every bank denying every application overnight.

That is not usually how it starts.

Instead, banks do two things at the same time.

They still approve strong borrowers. That explains why rejection rates can fall.

But they also cut risk on accounts they no longer like. That explains why account closures can rise at the same time.

So both things can be true:

You may still be able to get approved for a new credit card.

And banks may still be getting stricter with existing accounts.

That is not a contradiction. That is risk management.

The Signals Banks Watch Before Closing Accounts

Most credit card shutdowns are not random.

Banks are watching signals on your profile, especially when the overall economy is already flashing warning signs.

Here are the big ones:

-

Balances creeping up

-

High credit utilization

-

Carrying debt month-to-month instead of paying in full

-

Sudden changes in spending patterns

-

Sudden changes in payment behavior

-

Recent missed payments

-

Rising debt across multiple accounts

-

Signs your cash flow is getting tighter

-

Accounts sitting inactive for too long

One of these by itself may not cause a shutdown.

But when a few of them stack together, your account can start looking riskier to the bank.

And once your profile starts matching the same risk trends banks are already worried about, your account is more likely to get reviewed.

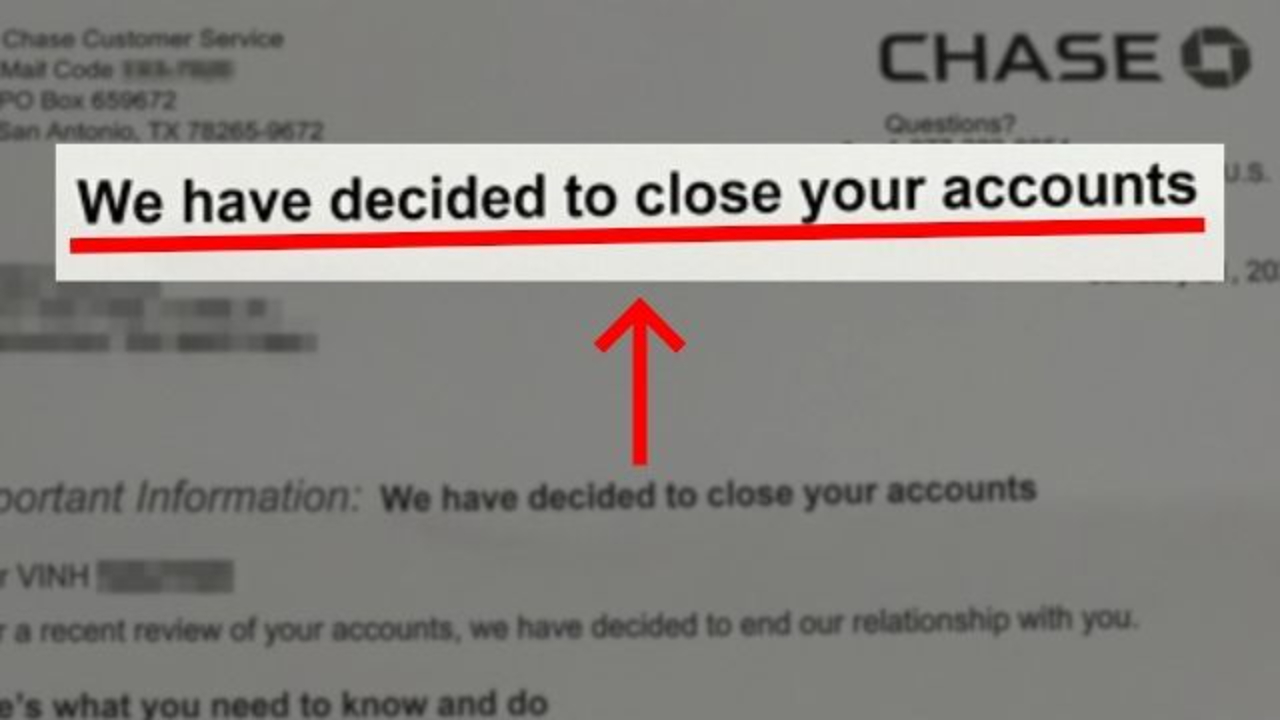

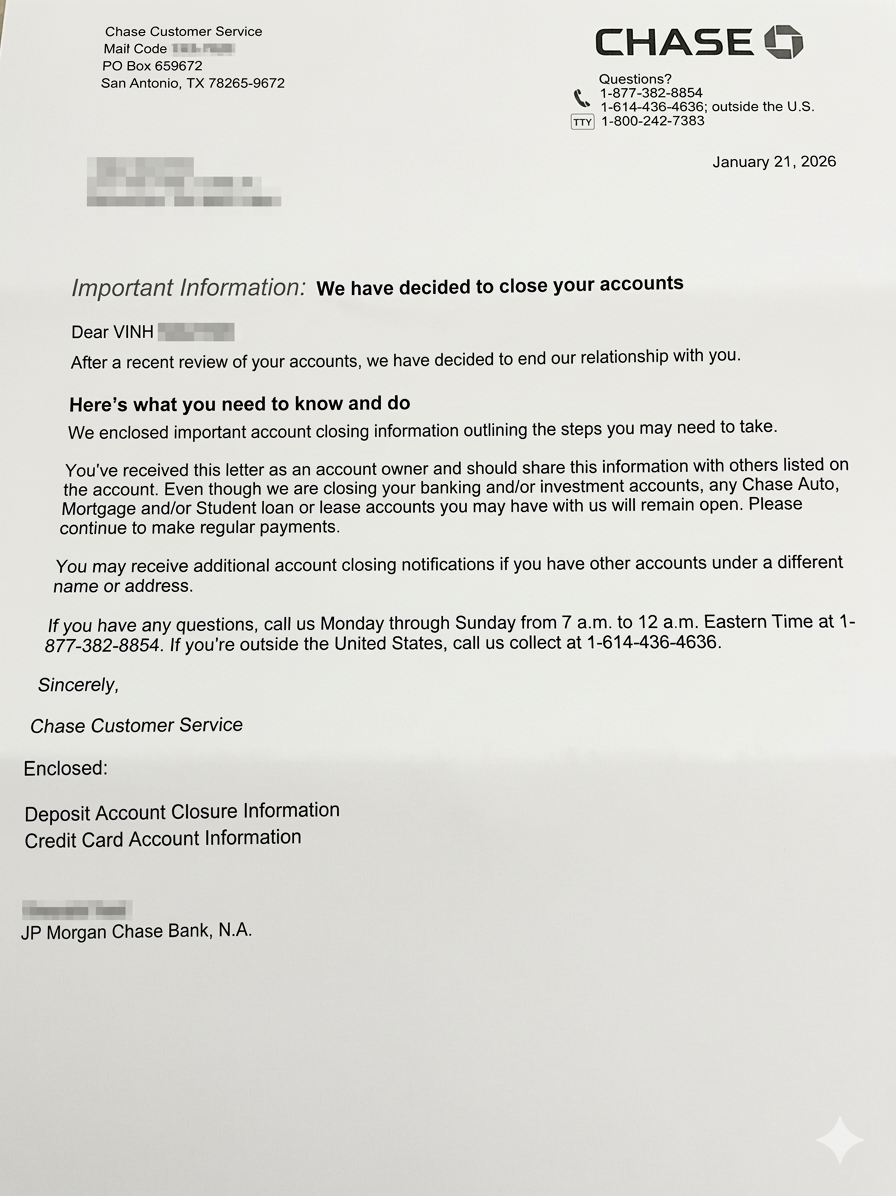

Yes, Banks Can Close Your Credit Card

This is where people get mad.

And I get it.

You may feel like, “I never missed a payment. How can they just close my card?”

But credit card issuers generally reserve the right to close an account. The CFPB says most card issuers reserve the right to close accounts at any time and are allowed to do so under the law. (Consumer Financial Protection Bureau)

That does not mean it feels fair.

But it does mean you need to understand the game you are playing.

A credit card limit is not permanent. It is access to borrowed money that the bank can reduce or remove when they think the risk has changed.

Why a Closed Credit Card Can Hurt Your Credit Score

A closed credit card can hurt you in a few ways.

The biggest issue is usually utilization.

When a bank closes your card, you lose that available credit. If you still owe balances on other cards, your overall utilization can jump fast.

TransUnion explains that closing accounts lowers your total available credit, which can increase your credit utilization ratio. That matters because utilization is part of credit scoring. (TransUnion)

The NFCC also points out that if a credit card is closed while you still owe a balance, you are still responsible for paying that balance, and the closure can hurt your score through utilization and other factors. (nfcc.org)

This is why account closures can create a snowball effect.

The bank closes a limit. Your utilization jumps. Your score drops. Then another lender sees the higher utilization and gets nervous too.

That is how one account closure can turn into a bigger credit problem.

Credit Limit Cuts Are Part of the Same Pattern

Banks do not always close the full account.

Sometimes they just cut the credit limit.

This can feel less dramatic, but it can still hurt.

If you had a $20,000 credit limit and the bank cuts it to $5,000, your available credit drops overnight. If you carry balances, your utilization can rise even if you did not spend another dollar.

That is why credit limit decreases can feel like a silent account closure.

The account is still open, but the bank has reduced its exposure to you.

And when banks are worried about rising delinquencies, high balances, or weaker consumer cash flow, credit limit cuts become one of the easiest ways for them to protect themselves.

Credit Limit Increase Requests Are Also Being Watched

One important detail from the New York Fed report is that people are increasingly asking for credit limit increases. The report said the likelihood of requesting a credit card limit increase rose slightly. (Federal Reserve Bank of New York)

That does not automatically mean everyone asking for a credit limit increase is in trouble.

Sometimes a credit limit increase is smart. It can help lower utilization and give you more flexibility.

But when millions of people start asking for more available credit at the same time, banks pay attention.

They want to know whether the demand is healthy or whether people are trying to create breathing room because cash is getting tight.

That is a big difference.

What Smart Borrowers Should Do Right Now

This is not the time to panic.

But it is also not the time to act sloppy.

If banks are getting more careful, you need to make your profile look as low-risk as possible.

Keep Utilization Low

High balances are one of the loudest risk signals on a credit report.

You do not need to carry a balance to build credit. Paying on time matters, but keeping balances low matters too.

If you are using a large percentage of your limits, banks may see that as stress.

Pay in Full When Possible

Banks like profitable customers, but they do not like risky customers.

If you are carrying balances across multiple cards month after month, that can make your profile look weaker.

Paying in full when possible sends a cleaner signal.

Avoid Sudden Risky Behavior

Do not max out cards.

Do not open a bunch of accounts you do not need.

Do not run up balances and then only make minimum payments.

That is exactly the kind of behavior banks watch during a tightening cycle.

Keep Good Accounts Active

Inactivity can also create problems.

If you have a card you care about, use it occasionally and pay it off. You do not need to spend a lot. You just want to show the account is still active and useful.

Build More Than One Banking Relationship

Depending on one bank is risky.

If that bank cuts your limits or shuts down your card, you do not want your whole credit strategy falling apart.

Having multiple healthy banking relationships gives you more options.

Helpful resource: If you want to diversify your credit options before applying, my Free Credit Card & Loan Pre-Approval Master List can help you compare soft-pull pre-approval tools before taking unnecessary hard pulls.

Should You Apply for New Credit Before Things Get Tighter?

Maybe.

But this depends on your profile.

If your credit is clean, your utilization is low, your income is stable, and you actually need another card, this may be a smart time to lock in credit while approvals are still strong.

But if your balances are high, your recent inquiries are stacking up, or you are already stretched thin, applying for more credit could backfire.

This is where people mess up.

They hear “banks are tightening” and rush to apply for everything.

That is not the strategy.

The strategy is to apply only when your profile looks strong enough to get approved without making you look desperate for credit.

Helpful resource: If you hate applying blind, my 9 Credit Cards That Reveal Your Starting Limit Before Approval can help you find options where you may be able to see your limit before fully committing.

Frequently Asked Questions

Why did my bank close my credit card if I never missed a payment?

A perfect payment history helps, but it does not make you immune. Banks may close or reduce accounts because of high utilization, inactivity, rising debt across your credit report, internal risk concerns, or broader tightening inside the bank.

Can a credit card company close my account without warning?

Yes. Most credit card issuers reserve the right to close accounts, and the CFPB says they are generally permitted to do so under the law. (Consumer Financial Protection Bureau)

Does a closed credit card hurt my credit score?

It can. The biggest issue is usually utilization. When a card closes, your available credit drops, which can make your balances look higher compared to your total limits. That can hurt your score.

Should I request a credit limit increase right now?

Only if your profile is strong. If your utilization is low, income is stable, and payment history is clean, a credit limit increase may help. But if your balances are high or your profile looks stressed, asking for more credit may not be the best move.

How do I reduce the chance of my credit card being closed?

Keep balances low, pay on time, avoid sudden risky spending, keep important cards active, and do not rely on one bank. Also review your credit reports so you can catch problems before lenders do.

Should I apply for more credit if banks are tightening?

Only if it makes sense for your profile. Strong borrowers may still get approved right now, but weak applications can lead to hard pulls, denials, and more risk signals. A good internal link here would be a post like “What to Do Before Applying for a Credit Card.”

Conclusion

Banks are not closing accounts for no reason.

They are reacting to risk.

Consumer debt is high. Delinquencies are elevated. More people are leaning on credit. More people are asking for limit increases. And banks are watching closely.

That does not mean you should be scared.

It means you should be strategic.

Keep utilization low. Pay on time. Avoid looking desperate for credit. Keep strong accounts active. Build more than one banking relationship. And apply only when your profile gives the bank a clear reason to say yes.

Because when banks start tightening, the sloppy profiles get cut first.