When to Pay Your Credit Card Bill to Raise Your Credit Score

Jun 28, 2026

Most people think paying a credit card bill is simple.

You wait for the due date.

You pay on time.

You move on.

That is fine if your only goal is avoiding late fees and interest.

But if your goal is raising your credit score, the timing matters a lot more than people realize.

The reason is simple: your credit card issuer usually reports your balance to the credit bureaus around your statement closing date, not necessarily your payment due date.

That reported balance is what affects your credit utilization.

And credit utilization can move your score quickly from month to month.

So if you are getting ready to apply for a mortgage, auto loan, personal loan, or new credit card, paying on the right days can make a real difference.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

The best time to pay your credit card bill for score optimization is usually before your statement closing date, because that is when many card issuers report your balance to the credit bureaus. A simple strategy is to pay most of the balance a couple of days before the statement closes, let a small balance report, then pay the rest before the due date so you avoid interest. This can help lower reported utilization, but the exact impact depends on your credit profile, balance, limits, and issuer reporting schedule.

Why Payment Timing Affects Your Credit Score

Your credit card payments affect your score in two major ways.

First, there is payment history.

This is whether you pay on time.

Miss a payment, and your score can take a major hit.

Second, there is credit utilization.

This is how much of your available revolving credit you are using.

Utilization is calculated like this:

Credit card balance ÷ credit limit × 100 = utilization percentage

So if you have a $1,000 limit and a $500 balance, your utilization is 50%.

That is high.

If you have a $1,000 limit and a $50 balance, your utilization is 5%.

That is much better.

This is why payment timing matters.

You could pay your card in full every month and still have a high balance report if you pay after the statement closes.

That is the part most people miss.

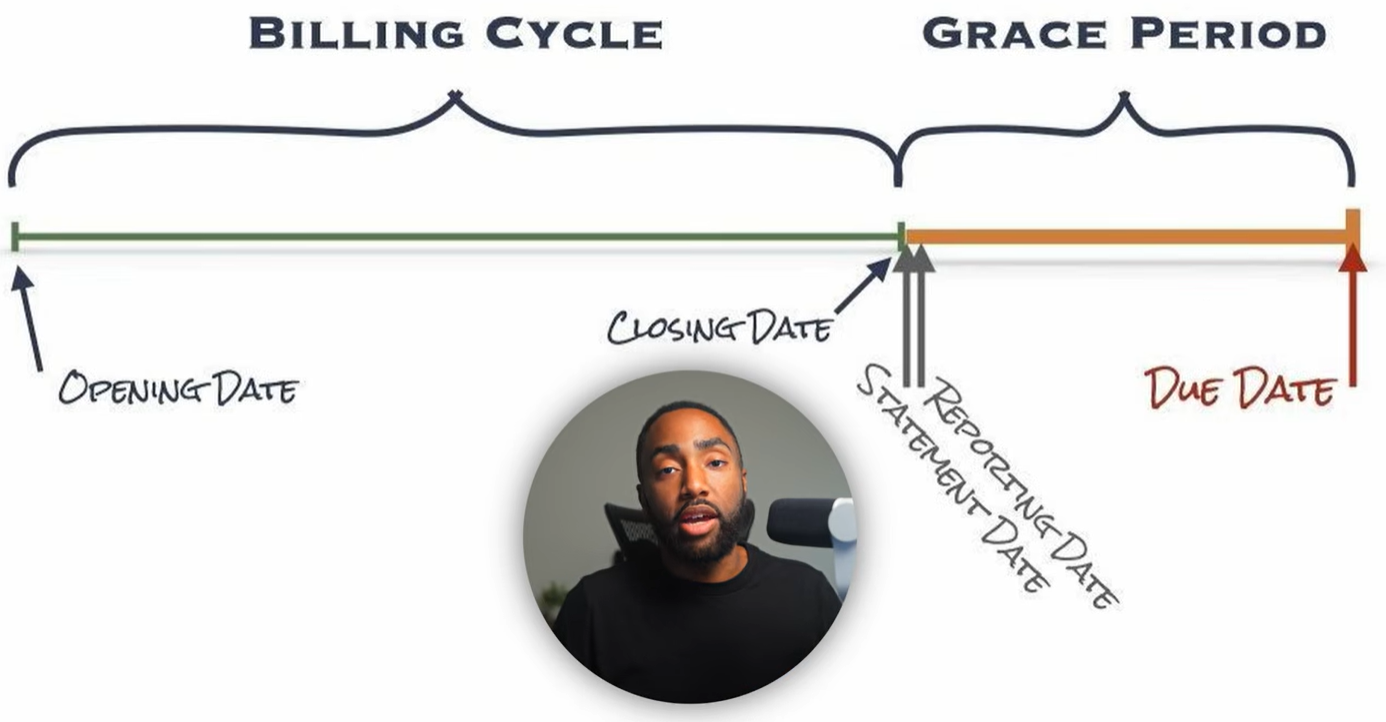

Your Due Date Is Not the Same as Your Statement Closing Date

There are three important dates on a credit card account:

-

Billing cycle opening date

-

Statement closing date

-

Payment due date

The billing cycle is the period where your purchases are counted for that statement.

The statement closing date is when the issuer finalizes that month’s statement.

The payment due date is when your payment must be made to avoid late fees and interest.

For credit score purposes, the statement closing date is often the most important date.

That is because many card issuers report your balance to the credit bureaus around the time your statement closes.

So if your statement closes with a high balance, that high balance may show up on your credit report even if you pay the card off a few days later.

This is why someone can say:

“I pay in full every month, so why did my score drop?”

The answer is usually reported utilization.

They paid in full, but they paid after the balance was already reported.

The Big Credit Card Payment Myth

One of the biggest myths is that you need to carry a balance to build credit.

That is false.

You do not need to pay interest to build credit.

You do not need to leave debt sitting on your card month after month.

You do not need to make only the minimum payment.

Carrying a balance can cost you money and create unnecessary debt.

The credit scoring system wants to see responsible use.

That does not mean you need to donate interest to the bank.

You can use the card, let a small balance report, and still pay in full before the due date.

That is the cleaner strategy.

Does Paying Early Reduce Your Rewards?

No.

Paying your credit card bill early does not reduce your cash back, points, or miles.

Rewards are usually earned when you make eligible purchases.

The payment date does not erase those rewards.

So if you use a credit card for rewards and then pay before the statement closes, you can still earn the rewards while managing utilization.

This is useful if you spend heavily on your cards but do not want a high balance reporting to the credit bureaus.

Why Paying Weekly Is Not Always Enough

Some people pay their card every week.

That is not bad.

It can help with budgeting.

It can also prevent balances from getting out of control.

But paying weekly is not always the best strategy for credit score optimization.

Here is why.

If your statement closes on the 15th, and you make several purchases on the 13th and 14th, your next weekly payment may not happen until after the statement closes.

That means the higher balance could still report.

So weekly payments may help, but they do not guarantee low utilization reporting.

If your goal is score optimization, you need to know your statement closing date.

Helpful resource: If you are rebuilding or trying to strengthen your credit profile, Kovo Credit Builder may be worth reviewing as part of your credit-building plan: https://offers.calbartoncashback.com/Kovo

The Problem With the 15/3 Credit Card Payment Method

You may have heard of the 15/3 method.

The common version says to make one payment 15 days before your due date and another payment 3 days before your due date.

The problem is that the method is often explained in a confusing way.

The score impact does not come from making two payments just because they are two payments.

Your credit card issuer does not give you bonus points for making multiple payments in the same cycle.

What matters most is the balance that gets reported to the credit bureaus.

If the 15/3 method helps you lower the balance before your statement closes, it can help.

But if the timing does not line up with the reporting date, it may not do much for your score.

So instead of obsessing over “15 days” and “3 days,” focus on the statement closing date.

That is the date that usually matters most for utilization.

The Two-Day Payment Strategy

The better strategy is simple.

Pay most of your balance a couple of days before your statement closing date.

Then pay the remaining balance after the statement closes but before the payment due date.

Here is the basic version:

-

Pay about 90% to 95% of your balance two days before your statement closing date.

-

Let a small balance report.

-

Pay the remaining balance before the due date.

The point is not the exact percentage.

The point is to make sure a low balance reports.

For many people, reporting a small balance is better than reporting a huge balance.

And in some scoring situations, reporting a tiny balance may score better than reporting zero on every card.

This is why some people use a low nonzero balance strategy before applying for major credit.

Why a Small Reported Balance Can Help

Credit scoring models often reward low utilization.

Not high utilization.

Not maxed-out cards.

Low utilization.

A commonly used target is keeping reported utilization under 10%.

For example:

-

$1,000 limit with $50 reported = 5% utilization

-

$5,000 limit with $250 reported = 5% utilization

-

$10,000 limit with $500 reported = 5% utilization

That range can show activity without making you look overextended.

The goal is to show that you use credit, but you are not relying on it too heavily.

That is the sweet spot.

Why Zero Balance Reporting Can Be Tricky

Paying all your cards to zero is not bad.

It is responsible.

But from a scoring standpoint, some people notice that having every revolving account report $0 can cause a small score dip compared to having one card report a very small balance.

That is why many credit people use what is often called the AZEO strategy.

AZEO stands for:

All Zero Except One.

That means all cards report $0 except one card that reports a small balance.

This is not something everyone needs to do every month.

But if you are preparing for a major application, like a mortgage or auto loan, it can be worth testing.

The Strategy Before a Big Loan Application

If you are a few months away from applying for a mortgage, auto loan, or personal loan, credit card reporting becomes more important.

A high reported balance can lower your score temporarily.

A lower score can affect:

-

Approval odds

-

Interest rate

-

Loan terms

-

Monthly payment

-

Required down payment

-

How much you can borrow

That is why you want your reported balances cleaned up before applying.

The best time to optimize is not the day before the application.

It is usually 30 to 60 days before, because you need time for updated balances to report.

If your cards report lower balances this month, your credit score may update after the bureaus receive that new information.

How to Find Your Statement Closing Date

You can usually find your statement closing date in your credit card account.

Look for:

-

Statement date

-

Closing date

-

Billing cycle end date

-

Next statement date

You can also check your monthly statement.

The closing date is usually listed near the top.

Once you know that date, set a reminder two to three days before it.

That is when you make the payment designed to lower the balance that reports.

Do not confuse this with your due date.

The due date protects you from late fees and interest.

The closing date is what helps you control reported utilization.

Example of How This Works

Let’s say your card has a $10,000 limit.

You spent $4,000 this month.

If that $4,000 reports, your utilization on that card is 40%.

That could hurt your score.

Now let’s say your statement closes on the 20th.

You pay $3,500 on the 18th.

That leaves $500 to report.

Now your utilization is 5%.

Then after the statement closes, you pay the remaining $500 before the due date.

Now you got the low utilization benefit without carrying debt or paying interest.

That is the whole strategy.

Do You Need to Do This on Every Card?

Not always.

If your utilization is already low, this may not make a big difference.

If you only have one card and the balance is small, it may be simple.

If you have 10, 20, or 30 cards, doing this on every card can become a lot of work.

That is why you should use this strategy when it matters most.

For example:

-

Before a mortgage application

-

Before an auto loan application

-

Before applying for new credit cards

-

Before requesting a credit limit increase

-

Before refinancing debt

-

When your utilization is temporarily high

You do not need to obsess over this every single week forever.

Use it as a tool.

What If You Have a Lot of Credit Cards?

If you have a lot of cards, the goal is to keep the system simple.

You can do that by:

-

Setting statement closing reminders

-

Using autopay for at least the minimum payment

-

Paying high-balance cards before they report

-

Letting only one card report a small balance

-

Keeping most cards at $0 before statement close

-

Avoiding heavy spending right before the closing date

This is not about micromanaging every $5 purchase.

It is about controlling what the credit bureaus see.

That is what affects the score.

What Not to Do

Do not carry a balance just to build credit.

Do not make only minimum payments if you can afford to pay more.

Do not assume paying by the due date means your utilization reported low.

Do not rely on the 15/3 method unless you understand your statement closing date.

Do not let high balances report right before a major loan application.

Do not forget that interest can still apply if you fail to pay the statement balance by the due date.

The goal is to lower reported utilization and avoid interest.

Both matter.

Frequently Asked Questions

What is the best day to pay my credit card bill?

The best day for score optimization is usually a couple of days before your statement closing date. That helps lower the balance that may be reported to the credit bureaus.

Should I pay my credit card before the due date or statement date?

You should always pay by the due date to avoid late fees and interest. But if you want to lower reported utilization, you may also want to pay before the statement closing date.

Does paying my credit card early hurt my rewards?

No. Paying early should not reduce the rewards you earn on eligible purchases. Rewards are typically tied to purchases, not the day you pay the bill.

Is the 15/3 credit card payment trick real?

The 15/3 method is often misunderstood. Multiple payments do not automatically boost your score. The real benefit comes from lowering your balance before it reports to the credit bureaus.

Should I let a small balance report?

In many cases, letting one card report a small balance can be better than having every card report zero. But this depends on your profile and is most useful when optimizing before a major application.

Can paying before the statement closing date raise my score fast?

It can help if your reported utilization drops. Scores can update once the lower balances are reported to the bureaus, but the exact timing and score change will vary.

Final Thoughts

If you want to raise your credit score, paying on time is the foundation.

But timing your payment around the statement closing date is the next level.

The due date keeps you safe from late fees and interest.

The statement closing date helps control what balance gets reported.

That reported balance affects utilization.

And utilization can move your score quickly.

So if you are preparing for a major application, do not just pay whenever.

Find your statement closing date.

Pay most of the balance a couple of days before that date.

Let a small balance report if that fits your strategy.

Then pay the rest before the due date.

That is how you use payment timing to help your score without carrying debt or paying interest.