U.S. Bank Unsecured Quick Loan: Up to $50,000 for Small Businesses

Jun 30, 2026

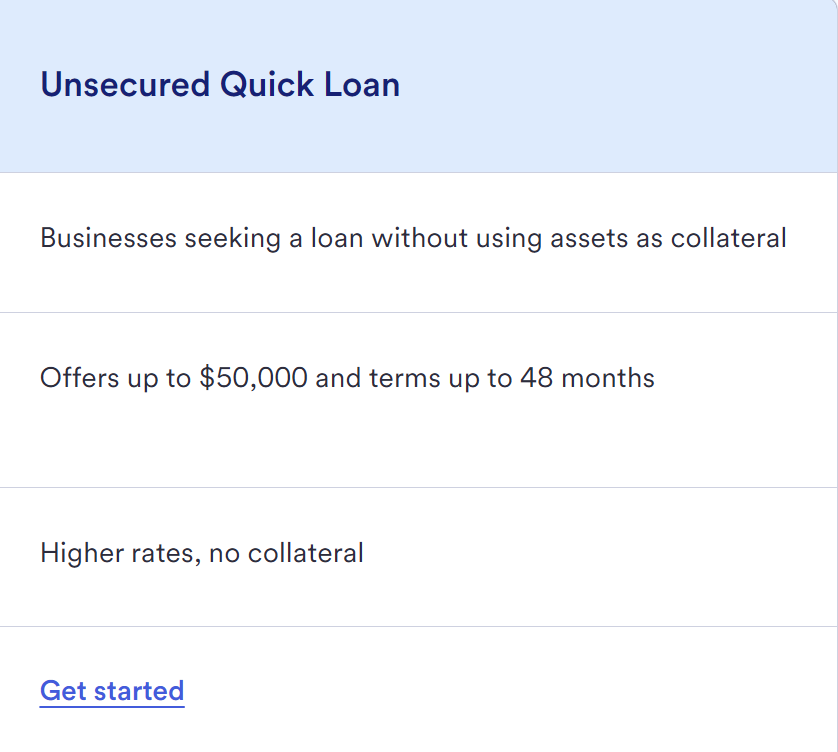

U.S. Bank is offering an unsecured business Quick Loan that can go up to $50,000.

No collateral.

Fixed payments.

Online application.

And in some cases, funding can move fast.

That matters because business opportunities do not always wait.

Maybe you just landed a dream client.

Maybe you found a bulk inventory deal.

Maybe you need to cover equipment, payroll, marketing, or a short-term cash flow gap.

If the money is needed now, waiting weeks for a traditional bank loan can kill the opportunity.

That is where the U.S. Bank Unsecured Quick Loan gets interesting.

But let’s be clear from the beginning.

This is not a no-PG loan.

This is not guaranteed.

And “no-doc” is not the same as “they will never ask for documents.”

U.S. Bank can still review your credit, revenue, time in business, cash flow, debt load, and loan purpose before approving you.

Quick Answer

The U.S. Bank Unsecured Quick Loan is a fixed-term small business loan with no collateral required, loan amounts up to $50,000, and terms up to 48 months. U.S. Bank says it may consider your credit score, time in business, annual revenue, cash flow, debt load, and how you plan to use the funds. Some applicants may not need to upload tax returns upfront, but U.S. Bank can request tax returns, financial statements, or legal documents in some cases, and a personal guaranty is required.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: Before applying for bank funding, my Fundable Business Plan Template can help you organize your business model, use of funds, revenue plan, and repayment story before a lender asks questions.

What Is the U.S. Bank Unsecured Quick Loan?

The U.S. Bank Unsecured Quick Loan is a business term loan.

That means you receive a lump sum of money and repay it over a fixed period.

Unlike a business line of credit, you are not repeatedly drawing, repaying, and reusing the same credit line.

This is a one-time loan.

U.S. Bank lists the unsecured version as offering up to $50,000 with terms up to 48 months.

The biggest advantage is that it does not require collateral.

So you are not pledging equipment, vehicles, inventory, or other business assets to secure the loan.

That makes it cleaner and faster than some secured business loans.

But because it is unsecured, the lender may care even more about your credit, revenue, cash flow, and repayment ability.

U.S. Bank Quick Loan vs. Secured Quick Loan

U.S. Bank has more than one Quick Loan option.

The secured Quick Loan can offer higher amounts because it is backed by business assets.

The unsecured Quick Loan is different.

It is designed for businesses that want funding without using assets as collateral.

Here is the simple breakdown:

-

Secured Quick Loan: Can offer larger funding amounts, but requires collateral.

-

Unsecured Quick Loan: Offers up to $50,000, but does not require collateral.

-

Business term loan: Usually for larger funding needs starting above Quick Loan levels.

-

Business line of credit: Better for ongoing or repeated cash flow needs.

So if you need a smaller lump sum and do not want to pledge collateral, the unsecured Quick Loan is the one to look at.

Who the U.S. Bank Quick Loan Is For

This loan is best for a business that needs a specific amount of money for a specific purpose.

Examples include:

-

Inventory

-

Equipment

-

Marketing

-

Hiring

-

Buildout costs

-

Short-term cash flow

-

Business expansion

-

One-time large purchase

-

Seasonal working capital

-

A project that should produce revenue

This is not the kind of loan I would use for random spending.

A fixed-term loan should have a clear job.

If the loan does not help the business make money, save money, or stabilize cash flow, think twice before taking it.

Who May Qualify?

Based on the script and U.S. Bank’s public lending guidance, here are the main factors to pay attention to:

-

Time in business

-

Personal credit profile

-

Annual revenue

-

Cash flow

-

Debt load

-

Business purpose

-

State eligibility

-

Existing U.S. Bank relationship

-

Industry type

-

Documentation readiness

The script says the business should be at least 6 months old and the owner should have a 680+ FICO score.

U.S. Bank’s public page confirms that lenders may consider time in business and lists at least 6 months minimum as a factor for term loan eligibility.

The 680 FICO point should be treated as an insider data point unless U.S. Bank confirms it for this exact product.

Eligible States Matter

The script says U.S. Bank’s eligible states include:

-

Arizona

-

Arkansas

-

California

-

Colorado

-

Idaho

-

Illinois

-

Indiana

-

Iowa

-

Kansas

-

Kentucky

-

Minnesota

-

Missouri

-

Montana

-

Nebraska

-

Nevada

-

New Mexico

-

North Dakota

-

Ohio

-

Oregon

-

South Dakota

-

Tennessee

-

Utah

-

Washington

-

Wisconsin

-

Wyoming

It also says some ZIP codes in North Carolina, South Carolina, and Texas may be eligible.

And if you are outside the eligible footprint, the script says you may need to be a U.S. Bank customer for at least 12 months before applying.

That is important because U.S. Bank is not equally available everywhere.

Before applying, check your ZIP code and eligibility directly with U.S. Bank.

Do not waste a hard pull if your location is not eligible.

Existing U.S. Bank Customers May Have an Advantage

The script included a useful point from a U.S. Bank sales support specialist:

If you do not live in an eligible state, being an existing U.S. Bank customer for 12 months may help open the door.

That lines up with how U.S. Bank often behaves.

They are relationship-heavy.

A checking account, savings account, business account, or prior banking relationship can matter.

That does not mean a relationship guarantees approval.

But it can make the application look less cold.

If you are outside U.S. Bank’s main footprint and want this loan later, opening a business banking relationship early may be worth considering.

Industries That May Be Disqualified

Before applying, check your industry.

The script says U.S. Bank does not accept applications from certain industries, including:

-

Payday lending

-

Auto title lending

-

Private prisons

-

Immigration detention centers

-

For-profit colleges

-

For-profit adoption agencies

-

Marijuana, cannabis, or CBD

-

Adult entertainment

-

Sexual encounter or dating/companion services

-

Virtual currency, crypto, or NFTs

-

Debt settlement

-

For-profit debt resolution

-

Life settlement funds

-

Mountaintop removal

-

New coal mining

-

Coal-fired power plants

-

Businesses illegal under local, state, or federal law

The script also says renting space to a business involved in one of those industries could create problems.

This list needs review before publishing because restricted-industry rules can change and may vary by product.

But the lesson is simple:

If your industry is high-risk, controversial, heavily regulated, or restricted by banks, check before applying.

What Documents Do You Need?

This is where the loan gets interesting.

The script says the application did not require uploading documents upfront.

No bank statements.

No tax returns.

No ID upload.

No financial statements.

But that does not mean U.S. Bank will never ask for documents.

U.S. Bank’s own page says that, in some cases, it may need tax returns, financial statements, or legal documents like articles of incorporation.

So the clean way to say it is this:

The application may feel no-doc upfront, but it can become low-doc or full-doc if the system flags your application.

That is a big difference.

“No-Doc” Until It Isn’t

This is the phrase to remember:

No-doc until it isn’t.

You may be able to get through the online application without uploading anything.

But if your request amount is higher, your revenue is unclear, your business is newer, your credit file is borderline, or your loan purpose needs review, U.S. Bank can ask for more.

The script says a U.S. Bank insider named Bill explained that requests over $40,000 may be more likely to trigger tax return requests.

That sounds reasonable, but treat it as a data point.

Not a published rule.

If you are requesting the high end, be ready to prove the business can support it.

How Much Can You Request?

Publicly, U.S. Bank says the unsecured Quick Loan offers up to $50,000 and terms up to 48 months.

But the script says the application showed an option to request $65,500 with terms as long as 60 months and an APR of 7.49%.

That is interesting.

But it needs review before publishing as a current claim.

It may have been based on a specific application path, profile, internal offer, secured option, relationship offer, or product routing.

For the main article, I would anchor the public claim at up to $50,000 because that is what U.S. Bank publicly lists for the unsecured version.

Then mention the $65,500 experience as a data point that needs verification.

The 20% Revenue Rule of Thumb

The script says Bill from inside sales gave a helpful rule of thumb:

U.S. Bank may often lend around 20% of gross annual revenue.

So if your business has $150,000 in annual gross revenue, a realistic approval may be closer to $30,000.

That makes sense from an underwriting perspective.

A bank does not want the loan amount to overwhelm the business.

But this should be treated as an insider data point, not an official U.S. Bank formula.

Still, it is a useful way to think.

If your revenue is $75,000 per year, asking for $50,000 may be a stretch.

If your revenue is $300,000 per year, a $50,000 request may look more reasonable.

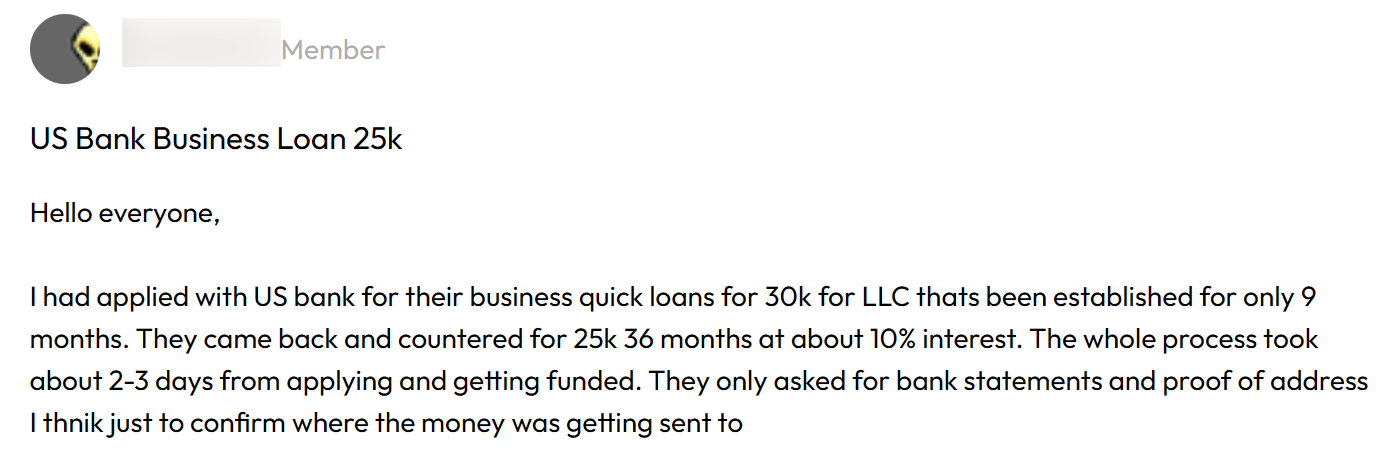

Real Data Point: $25,000 Funded in 2–3 Days

One borrower shared this data point:

They applied for $30,000.

U.S. Bank countered at $25,000.

The loan was for 36 months at around 10% interest.

Their business was only 9 months old.

They were funded in 2–3 days.

They said U.S. Bank did not ask for tax returns, but did ask for bank statements and proof of address.

Their scores were:

-

Experian: 732

-

TransUnion: 688

-

Equifax: 709

That is a solid data point.

It shows a newer business can potentially get approved.

But notice the key details:

They did not get the full $30,000.

They had multiple scores around or above the high-600s.

They still had to provide some documentation.

And the loan was not free money.

It had a real interest rate and repayment term.

Why the Counteroffer Matters

The counteroffer is one of the most important parts of that data point.

They asked for $30,000.

U.S. Bank offered $25,000.

That tells you the bank may not simply approve or deny.

It may adjust the amount based on what the business can support.

That is useful.

If you apply for more than the bank is comfortable with, you might still get a smaller approval.

But do not count on that.

A request that is too aggressive can still trigger more review or denial.

How the Application Works

The script says the process starts on the U.S. Bank website.

The path is:

Business → Business Loans → Unsecured Quick Loan

From there, you can apply online.

The script says there was no need to schedule a branch meeting and that the U.S. Bank sales support specialist said applying online or in person makes no difference.

That is useful if true.

But I would still say this:

If you already have a strong U.S. Bank relationship or a helpful banker, a conversation may still be worth having.

But if the application is the same, applying online can save time.

What Information You Enter

The application may ask for personal and business basics, including:

-

Legal name

-

Social Security number

-

Annual income

-

Contact information

-

Business name

-

Entity type

-

NAICS code

-

Formation date

-

Ownership breakdown

-

Tax ID or EIN

-

Business address

-

Gross annual sales

If there are owners with 20% or more ownership, expect to list them.

If you are the sole owner, the application should be simpler.

But make sure every detail matches your business records.

Mismatched addresses, entity names, ownership details, or EIN information can slow down underwriting.

The 4506-C Warning

The script says there was no place to upload tax returns during the application.

But it also says the applicant had to agree that U.S. Bank could request IRS tax return transcripts using Form 4506-C if needed.

That matters.

Even if the loan starts as no-doc, you may be giving permission for tax transcript access later.

So do not apply using numbers you cannot support.

If the system asks for transcripts and your stated revenue does not match reality, that can create problems.

Be accurate.

Be reasonable.

Be ready.

What Should You Put for Loan Purpose?

Loan purpose matters.

U.S. Bank says lenders may consider how you plan to use the funds.

So do not treat this like a meaningless checkbox.

Strong purposes usually connect to revenue, growth, or operating stability.

Examples include:

-

Inventory

-

Equipment

-

Business expansion

-

Hiring

-

Marketing

-

Operational expenses

-

Short-term cash flow gap

-

One-time large purchase

-

Preparing for seasonal demand

The stronger your use of funds, the better your story.

A lender wants to believe the loan helps the business grow or operate better.

Loan Purposes to Be Careful With

The script warns against selecting “debt consolidation” or vague working capital with no explanation.

That makes sense.

Debt consolidation can suggest the business is already under pressure.

And vague answers do not help underwriting understand how the money will be used.

That does not mean those purposes are always denied.

But if you choose a purpose that sounds like rescue funding instead of growth funding, expect more scrutiny.

A better approach is to explain clearly how the funds support revenue or operations.

The Pros

The U.S. Bank Unsecured Quick Loan has several strong points.

No Collateral Required

The unsecured version does not require business assets as collateral.

That makes it useful for businesses without equipment, vehicles, or inventory to pledge.

Fixed-Term Structure

You know the term and payment schedule.

That can be easier to plan around than some short-term business funding products with daily or weekly payments.

Online Application

The streamlined online application can save time compared with a traditional full-document bank loan.

Potentially Fast Funding

U.S. Bank says some loans may offer quick decisions, and the data point showed funding in 2–3 days.

Bank Relationship Value

Responsible repayment may help build trust with U.S. Bank for future credit cards, lines of credit, or larger lending products.

The Cons

This loan also has real drawbacks.

A Personal Guaranty Is Required

U.S. Bank says a personal guaranty is required for small business loans and lines of credit.

That means if the business fails to repay, you may be personally responsible.

Do not confuse unsecured with no personal guarantee.

They are not the same.

No Collateral Does Not Mean No Risk

Unsecured means no specific asset is pledged as collateral.

But the debt still has to be repaid.

If you default, the lender can still pursue collection according to the loan agreement and law.

No True Soft-Pull Preapproval

The script says there is no soft-pull preapproval tool for this loan.

U.S. Bank says exploring options or getting a financing recommendation may not impact credit, but a formal application may involve a credit check.

So do not apply casually.

Documents Can Still Be Requested

Even if no documents are required upfront, U.S. Bank can ask for tax returns, financial statements, bank statements, proof of address, or legal documents in some cases.

Higher Amounts May Trigger More Review

Requests above $40,000 may be more likely to need documentation, according to the script’s insider data point.

When This Loan Makes Sense

This loan may make sense when you have a clear short-term business need and a plan to repay.

Examples:

-

You need inventory for a seasonal sales push.

-

You need equipment to fulfill a contract.

-

You have a new client project and need upfront working capital.

-

You need to hire help before revenue hits.

-

You have a cash flow gap tied to receivables.

-

You want to build a deeper U.S. Bank relationship.

This is a tool for a business with a plan.

Not a lifeline for a business with no path to repay.

When This Loan Does Not Make Sense

This loan may not be right if:

-

Your cash flow is unstable.

-

You are already behind on bills.

-

You cannot afford fixed payments.

-

You are borrowing without a clear use.

-

You are trying to cover long-term losses.

-

Your industry is restricted.

-

You do not want a personal guarantee.

-

Your credit profile is not ready.

-

You cannot support your stated revenue.

-

You need a revolving line instead of a term loan.

A fast loan can help a strong business move faster.

But it can also make a struggling business worse.

How to Improve Your Odds Before Applying

Here is what I would do before applying:

-

Check state and ZIP code eligibility.

-

Make sure the business is at least 6 months old.

-

Unlock all three credit bureaus.

-

Pay down personal credit card utilization.

-

Avoid recent hard inquiries.

-

Organize bank statements.

-

Organize tax returns.

-

Confirm business address and entity details.

-

Know your gross annual revenue.

-

Know your monthly cash flow.

-

Choose a clear loan purpose.

-

Request an amount the revenue can support.

Do not go into a bank loan application sloppy.

Banks like clean files.

Requesting Less May Help

If you want the cleanest possible experience, requesting less may help.

The script suggests keeping the request under $30,000 if your goal is to maximize the odds of avoiding tax return requests.

That is not a guaranteed rule.

But it is a smart idea.

A $25,000 request may be easier to approve than a $50,000 request.

Especially for a newer business.

The higher the loan amount, the more the bank may want proof.

Shorter Terms May Look Better

The script also recommends choosing shorter repayment terms, like 12 to 24 months, if the business can afford it.

That can reduce lender risk because the money comes back faster.

But do not choose a short term just to impress the bank if the payment will strain your cash flow.

The best term is the one your business can actually handle.

A shorter term with missed payments is worse than a longer term paid perfectly.

Why Bank Statements Matter

Even if tax returns are not required, bank statements can matter.

Bank statements show:

-

Deposits

-

Cash flow

-

Overdrafts

-

Ending balances

-

Business activity

-

Revenue consistency

-

Payment behavior

-

Existing loan payments

-

Cash cushion

If your bank statements are messy, fix that before applying.

No lender wants to see constant overdrafts, bounced payments, or deposits that do not match the revenue story.

Why a Business Plan Helps

U.S. Bank says a clear business plan and financial documentation can help strengthen an application.

That does not always mean you need a 40-page document.

But you should know:

-

What the business does

-

How it makes money

-

Who the customers are

-

How the loan will be used

-

How the loan helps revenue

-

How the loan will be repaid

-

What contracts or opportunities support the request

This is especially important if you get manually reviewed.

Helpful resource: If you need to organize this before applying, my Fundable Business Plan Template can help you turn your numbers, loan purpose, and repayment story into something cleaner for lenders.

U.S. Bank Quick Loan vs. No-PG Business Cards

The script originally compared this with no-PG business cards.

That comparison is useful, but only if we are clear.

The U.S. Bank Unsecured Quick Loan requires a personal guaranty.

Many no-PG business cards do not.

But they are different products.

A term loan gives you a lump sum and fixed payments.

A no-PG business card or corporate card gives you a spending line that may need to be paid in full.

One is not automatically better.

They solve different problems.

If you need upfront cash for a specific project, a loan may fit.

If you need ongoing business spending capacity without personal credit reporting, a no-PG business card may fit better.

Frequently Asked Questions

Is the U.S. Bank Quick Loan unsecured?

Yes, the U.S. Bank Unsecured Quick Loan does not require collateral. But unsecured does not mean no personal guarantee. U.S. Bank says a personal guaranty is required for small business loans and lines of credit.

How much can you borrow with the U.S. Bank Unsecured Quick Loan?

U.S. Bank publicly lists the unsecured Quick Loan as offering up to $50,000 with terms up to 48 months. The actual amount depends on borrower qualifications and use of funds.

Does U.S. Bank require tax returns for the Quick Loan?

Not always upfront. U.S. Bank says that in some cases it may need tax returns, financial statements, or legal documents like articles of incorporation.

What credit score do you need for the U.S. Bank Quick Loan?

The script says a 680+ FICO score is recommended or required based on insider conversations. Verify this directly with U.S. Bank before applying because public underwriting standards may vary.

Does the U.S. Bank Quick Loan require a personal guarantee?

Yes. U.S. Bank says business owners must provide a personal guaranty to obtain small business credit.

How fast can you get funded?

U.S. Bank says its online process may provide quick decisions and fast funding. One data point in the script reported funding in 2–3 days after being approved for $25,000.

Conclusion

The U.S. Bank Unsecured Quick Loan is one of the more interesting bank loan options for small business owners who need fast capital without pledging collateral.

Up to $50,000.

Terms up to 48 months.

No collateral required.

Online application.

Potentially fast funding.

That is a strong setup.

But do not confuse easy application with easy approval.

U.S. Bank can still review your credit, time in business, revenue, cash flow, debt load, documents, industry, and use of funds.

And yes, a personal guaranty is required.

So the best move is to apply with a clean profile and a clear plan.

Know your numbers.

Know your loan purpose.

Keep your request realistic.

Have bank statements and tax returns ready just in case.

And make sure the loan helps the business make money, save money, or move faster.

Because fast funding is only powerful when it is tied to a smart business move.