Uber Stopped Accepting Discover Cards: Why This Matters for Capital One Customers

Jun 29, 2026

Uber stopped accepting Discover cards inside the app for many U.S. users.

And that is a much bigger story than people realize.

Because this is not just about one Discover card getting declined after work.

This is about the payment network behind your card.

And now that Capital One owns Discover and has started issuing some Capital One cards on the Discover network, this could affect more people than just traditional Discover cardholders.

Think about that for a second.

You open Uber after a long day, try to book a ride or order food, and your card suddenly does not work because the network behind it is not accepted in the app.

That is annoying by itself.

But the bigger question is even scarier:

What happens if your favorite Capital One card slowly moves from Visa or Mastercard onto the Discover network, and more merchants start pushing back?

Quick Answer

Uber and Uber Eats stopped allowing some users to add new Discover cards in the app, with reports saying the app shows messages like “Discover cards are not accepted by Uber.” Some previously linked Discover cards may still work, but new Discover card additions appear blocked for many users. This matters because Capital One has started issuing some Quicksilver, Savor, and VentureOne cards on the Discover network after acquiring Discover, so acceptance issues may eventually matter to some Capital One customers too.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: Before applying for another card, my Free Credit Card & Loan Pre-Approval Master List can help you check soft-pull pre-approval options so you are not wasting hard pulls on cards that may not fit your wallet.

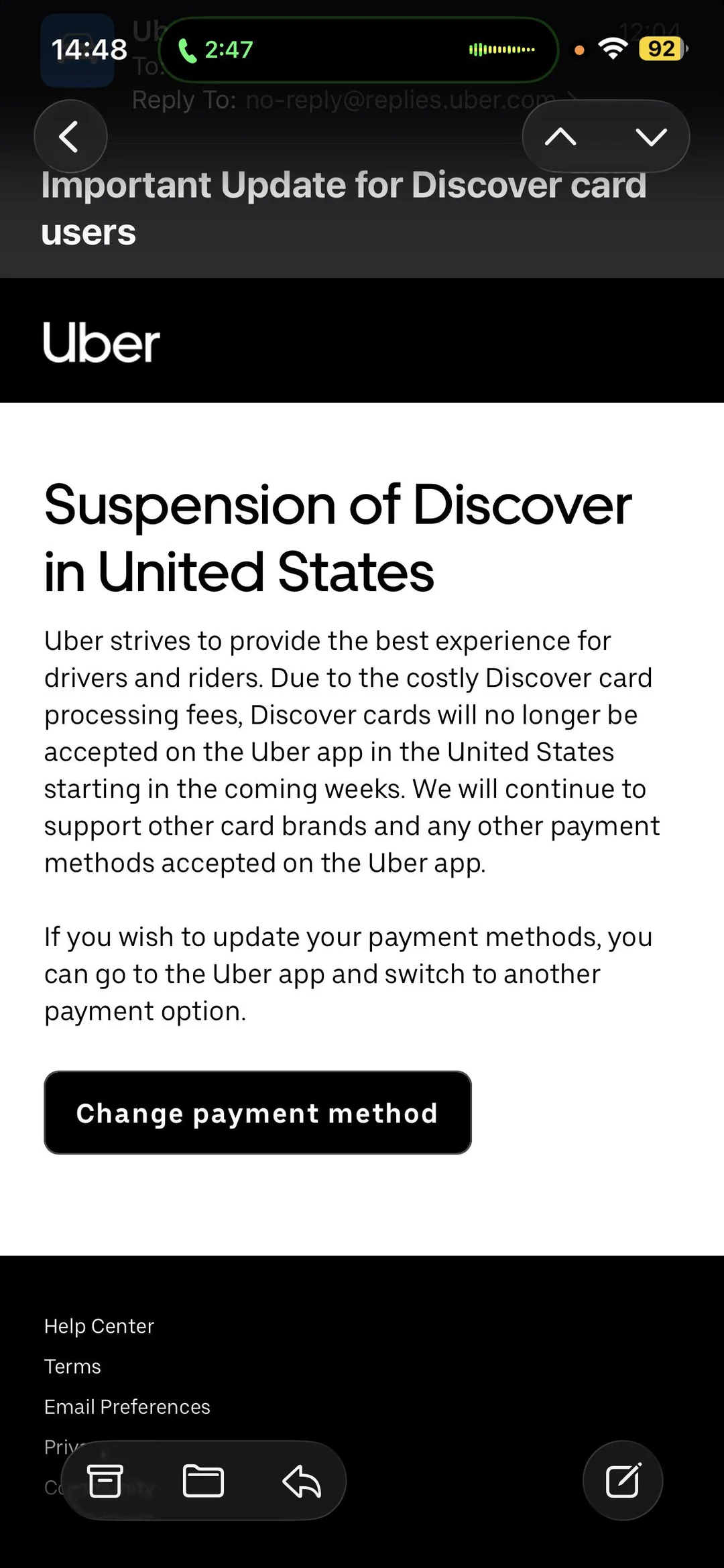

What Happened With Uber and Discover?

Users started reporting that Uber and Uber Eats no longer allowed them to add Discover cards inside the app.

Some people received notices.

Others found out the hard way when they tried to add a Discover card and saw an error message saying:

“Discover cards are not accepted by Uber.”

Doctor of Credit also reported that Uber and Uber Eats no longer allowed adding Discover cards in the app, though some people with Discover cards already saved in the app were still able to use them.

That distinction matters.

This does not appear to mean every existing Discover card instantly stopped working for every user.

But it does mean new Discover card usage through Uber became a problem for many people.

And for a mainstream app like Uber, that is not a tiny inconvenience.

That is a major acceptance issue.

Uber Says This Is About Discover Processing Fees

Uber’s stated explanation is that Discover processing fees are costly.

And on the surface, that sounds believable.

Card networks and issuers charge merchants to process payments. Some networks cost more than others. If Uber believes Discover costs too much, it may decide not to accept those cards or may use non-acceptance as negotiation leverage.

But this explanation raised eyebrows immediately.

Why?

Because American Express has historically had a reputation for higher merchant acceptance costs than Visa and Mastercard, and Uber still accepts Amex.

That is why a lot of people online think the “fees” explanation may not be the whole story.

It may be part of the story.

But it also looks like a negotiation.

Why People Think This Is Really About Capital One and Discover

Here is where the story gets bigger.

Capital One completed its acquisition of Discover in 2025. Capital One said the deal brought the companies together and positioned them to build a stronger payments network.

After that, reports started showing that Capital One began issuing some cards on the Discover network.

PaymentsJournal reported that updated benefits guides showed new versions of cards like Savor, Quicksilver, and VentureOne being issued on the Discover rails.

Doctor of Credit also reported that Capital One benefits guides appeared for Venture, Savor, and Quicksilver cards using the Discover network.

That changes the whole conversation.

Because now this is not just about people with Discover It cards.

This could affect some Capital One customers too.

If your Capital One card runs on Discover instead of Visa or Mastercard, merchant acceptance starts to matter in a different way.

Most People Never Think About the Payment Network

Most people look at the bank name.

They see:

Capital One

And they assume:

“Okay, this card should work everywhere.”

But that is not how card acceptance works.

The network matters.

A credit card can be issued by Capital One, Chase, Amex, Citi, Wells Fargo, or any other bank.

But the actual network may be:

-

Visa

-

Mastercard

-

American Express

-

Discover

That network controls where the card can be accepted.

Visa and Mastercard have massive acceptance.

Amex is also widely accepted, especially in the U.S., though still not everywhere.

Discover has strong domestic acceptance, but it has historically been weaker internationally and can still run into specific merchant acceptance problems.

So if a Capital One card moves onto Discover rails, the card may still be a Capital One card.

But the acceptance experience can feel different.

That is what people are worried about.

Why This Matters for New Capital One Customers

This is the part Capital One customers need to pay attention to.

Some new Capital One customers expected a Mastercard or Visa product and instead received a card running on the Discover network.

For people who only use cards domestically at major merchants, that may not be a problem most days.

But when a massive app like Uber stops accepting Discover cards for new additions, people start asking:

Is this what the future looks like?

That is the real anxiety.

Nobody wants their everyday card to become less useful.

Nobody wants to find out at checkout, during travel, or inside a rideshare app that their card does not work anymore.

And nobody wants to sign up expecting one type of network only to feel like they got moved to a weaker acceptance setup.

This Is the First Real Stress Test

To me, this feels like one of the first public stress tests of the Capital One + Discover strategy.

Capital One did not buy Discover just to own another credit card portfolio.

The real prize is the network.

If Capital One can move more of its own transaction volume onto the Discover network, it may reduce dependence on Visa and Mastercard and keep more economics inside its own ecosystem.

That could be a massive strategic win for Capital One.

But for cardholders, the question is simpler:

Will the card work where I need it to work?

That is all consumers care about.

Rewards do not matter if the card gets rejected.

A great welcome bonus does not matter if your app will not accept the network.

A strong cash back setup does not matter if merchants start pushing back.

The Questions Cardholders Are Asking

This Uber situation raises a bunch of real questions.

People are now asking:

-

Will other apps stop accepting Discover too?

-

Will this affect Capital One cards issued on Discover?

-

Will merchants use this as leverage in negotiations?

-

Will Discover acceptance become more of a problem domestically?

-

Will international acceptance become an even bigger concern?

-

Will Capital One offer cardholders a Visa or Mastercard alternative?

-

Will existing Capital One cards eventually migrate to Discover?

Those are valid questions.

And the reason they matter is because Uber is not some tiny merchant.

This is one of the most mainstream apps in the country.

So if Uber can say no to Discover, other companies may be watching.

This Could Be a Negotiation Tactic

A lot of people believe Uber is playing hardball.

And honestly, that theory makes sense.

Companies fight over payment costs all the time.

Sometimes access gets limited.

Sometimes one side applies pressure.

Sometimes the customer gets stuck in the middle.

We have seen similar fights with cable companies, streaming services, sports networks, app stores, and payment platforms.

This feels similar.

Uber may be saying:

“If you want acceptance here, the economics need to work for us.”

And Capital One may now care a lot more because Discover acceptance is part of its long-term strategy.

That gives Uber leverage.

Especially during the transition period.

This Could Backfire on Uber

Here is the ironic part.

This could also backfire on Uber.

Some Discover users are already talking about workarounds or switching behavior.

That could include:

-

Using Lyft instead

-

Buying Uber gift cards

-

Trying PayPal or Apple Pay routing

-

Using a Visa or Mastercard backup

-

Moving spend to another rideshare card

-

Using cards that bonus Lyft instead

That matters because credit card users are not always passive.

If Uber makes the payment experience annoying, some users may shift spend somewhere else.

And if Capital One customers start getting dragged into this because their new cards are issued on Discover, frustration could grow.

Uber may have leverage.

But customers have choices too.

The Bigger Lesson: Card Infrastructure Matters

This whole story highlights something most people ignore.

The infrastructure behind your card matters just as much as the rewards.

A 3% or 5% earning rate sounds great.

But it means nothing if the card does not work where you need it.

A high limit is great.

But it does not help if the app rejects the network.

A sleek card design is nice.

But it does not matter if your payment fails while you are trying to get home.

This is why I do not like being overly dependent on:

-

One bank

-

One card

-

One payment network

-

One rewards ecosystem

-

One fintech app

-

One issuer relationship

Things change fast.

A merger happens.

A payment agreement breaks.

A merchant pushes back.

A network transition starts.

And suddenly your favorite card becomes less convenient overnight.

Why You Need Backup Cards

This is the practical lesson.

Always have backup cards on different networks.

A smart wallet should usually include more than one network.

For example:

-

A Visa

-

A Mastercard

-

An Amex, if it fits your spending

-

A Discover, if you like the rewards

-

A debit card or backup bank card for emergencies

That way, if one network gets rejected, you are not stuck.

This matters even more if you travel.

Discover acceptance can be much weaker outside the U.S. compared with Visa and Mastercard. If your primary travel card moves to Discover, you need to think twice before relying on it internationally.

Helpful resource: If you want to compare cards before adding a backup, my 9 Credit Cards That Reveal Your Starting Limit Before Approval can help you research options that may show your starting limit before you fully commit.

What Discover Cardholders Should Do Now

If you currently use Discover with Uber or Uber Eats, check your app now.

Do not wait until you need a ride.

Here is what I would do:

-

Open Uber and Uber Eats

-

Check whether your Discover card is still saved

-

Try adding it again only if you are okay testing it

-

Add a Visa or Mastercard backup

-

Check whether PayPal or Apple Pay works for your setup

-

Consider buying Uber Cash or gift cards only if it makes sense

-

Do not rely on one card for transportation

The worst time to find out your card does not work is when you are standing outside trying to get home.

Test it before you need it.

What Capital One Customers Should Watch

If you are a Capital One customer, look at your actual network.

Do not just look at the bank.

Check whether your card says:

-

Visa

-

Mastercard

-

Discover

If you are applying for a new Quicksilver, Savor, VentureOne, or similar Capital One card, review the terms and benefits guide before applying.

You want to know what network you are getting.

Because if the card runs on Discover, it may still be a good card.

But you need to understand the acceptance tradeoff.

That is especially true if you use the card for:

-

Uber

-

Subscriptions

-

International travel

-

Small businesses

-

Online services

-

Payment apps

-

Travel bookings

The card can have great rewards and still be annoying if the acceptance does not match your lifestyle.

What Happens Next?

This is the part everyone is watching.

A few things could happen.

Uber could reverse course.

Capital One and Discover could negotiate behind the scenes.

Uber could keep blocking new Discover cards.

Other merchants could start pushing back.

Capital One could adjust which cards go onto Discover.

Or the whole thing could quietly fade away after a deal gets worked out.

But I do think this is only the beginning.

If Capital One is serious about scaling Discover as a real competitor to Visa and Mastercard, there will probably be more friction over the next few years.

That does not mean Discover is doomed.

It means building a major payments network is hard.

And consumers may feel some bumps along the way.

Frequently Asked Questions

Does Uber accept Discover cards?

Recent reports show Uber and Uber Eats stopped allowing many users to add new Discover cards in the app. Some users with Discover cards already saved may still be able to use them, but the experience appears inconsistent.

Why did Uber stop accepting Discover cards?

Uber reportedly pointed to costly Discover processing fees. Some users and credit card watchers believe the fee explanation may also be part of a broader negotiation between Uber, Discover, and Capital One.

Does this affect Capital One cards?

It may affect some Capital One cards if they are issued on the Discover network. Capital One has started issuing some cards, including certain Quicksilver, Savor, and VentureOne products, on Discover rails after acquiring Discover.

How do I know what network my Capital One card uses?

Look at the logo on the card or check the card details and benefits guide. Your card may say Visa, Mastercard, or Discover depending on the product and when it was issued.

Is Discover accepted everywhere?

Discover has broad U.S. acceptance, but it is not accepted everywhere. Acceptance can also be weaker internationally compared with Visa and Mastercard. Specific merchants or apps may choose not to accept Discover.

Should I avoid Discover-network Capital One cards?

Not automatically. A Discover-network Capital One card may still be useful if the rewards, APR, limit, and benefits fit your needs. But you should have a Visa or Mastercard backup, especially for travel, apps, subscriptions, and merchants where Discover acceptance may be uncertain.

Conclusion

Uber blocking new Discover cards is not just a Discover story.

It is a warning shot for the whole Capital One and Discover merger.

Because if more Capital One cards start moving onto the Discover network, acceptance becomes a bigger issue for everyday cardholders.

Most people do not think about payment networks until something breaks.

Then suddenly, it matters.

The lesson is simple:

Do not build your wallet around one card, one issuer, or one network.

Rewards are great.

Cash back is great.

Low APRs are great.

But none of it matters if the card does not work when you need it.

So check your cards.

Know your networks.

Keep backups.

And if you are applying for new Capital One cards, pay attention to whether you are getting Visa, Mastercard, or Discover.

Because in the new Capital One–Discover era, that small logo on your card may matter a lot more than people think.