SoFi Approved Me for a $51,000 Personal Loan With No Docs

Jun 28, 2026

SoFi approved me for a $51,000 personal loan with no documents required.

No W-2s.

No pay stubs.

No tax returns.

No bank statements.

And the money landed in my SoFi checking account the same day.

That part shocked me.

I have tested a lot of banks, credit cards, personal loans, and funding products over the years. A $51,000 personal loan getting approved and funded in a few hours is not normal with most traditional lenders.

But this one moved fast.

I applied in the morning.

The decision came back in under 20 minutes.

By mid-afternoon, the funds were sitting in my account.

That is why I wanted to break down the full data point, because this was one of the cleanest personal loan approvals I have ever seen.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

SoFi approved me for a $51,000 personal loan with no income documents and same-day funding. My Experian FICO 8 score was around 765, utilization was about 12%, and I had a long relationship with SoFi through checking, savings, and their credit card. SoFi pulled Experian only in my case, but your result may vary based on your credit profile, income, debt-to-income ratio, loan amount, and SoFi relationship.

Why I Tested SoFi’s Personal Loan

I had been staring at a SoFi pre-approval email for two days.

The offer was sitting right there.

But I still had that moment of hesitation.

I had used 0% APR credit cards for a kitchen and bathroom renovation, and those promo periods were getting close to expiring.

That meant the balances were about to move from 0% interest to much higher interest rates.

So on paper, a personal loan made sense.

The loan could consolidate the balances, simplify the payments, and stop the credit card interest from kicking in.

But even with everything I know about credit and funding, I still had that little voice in my head.

Do I really need to do this right now?

Part of me wanted to wait.

The other part was curious.

I had been banking with SoFi for years. My checking, savings, and credit card were already with them.

So I wanted to know:

Would SoFi actually deliver the smooth, fast personal loan experience they advertise?

Or would I end up stuck in a manual review waiting for documents?

Pre-Approval Is Not Final Approval

This is important.

A pre-approval is not a guarantee.

With credit cards, a strong pre-approval can sometimes mean you are most of the way there.

But personal loans are different.

The loan amounts are bigger.

The repayment terms are longer.

The underwriting can be more serious.

There is more room for things to go sideways.

That is why I was still cautious even though my credit profile was strong.

I had seen enough personal loan data points to know what can happen.

Some people get pre-approved, then get asked for W-2s, pay stubs, tax returns, or bank statements.

Some people get a strong initial offer, then the final approval changes.

Some people get pushed into manual review.

So even with a 765 Experian FICO 8 and a long SoFi relationship, I still had that little bit of doubt before hitting submit.

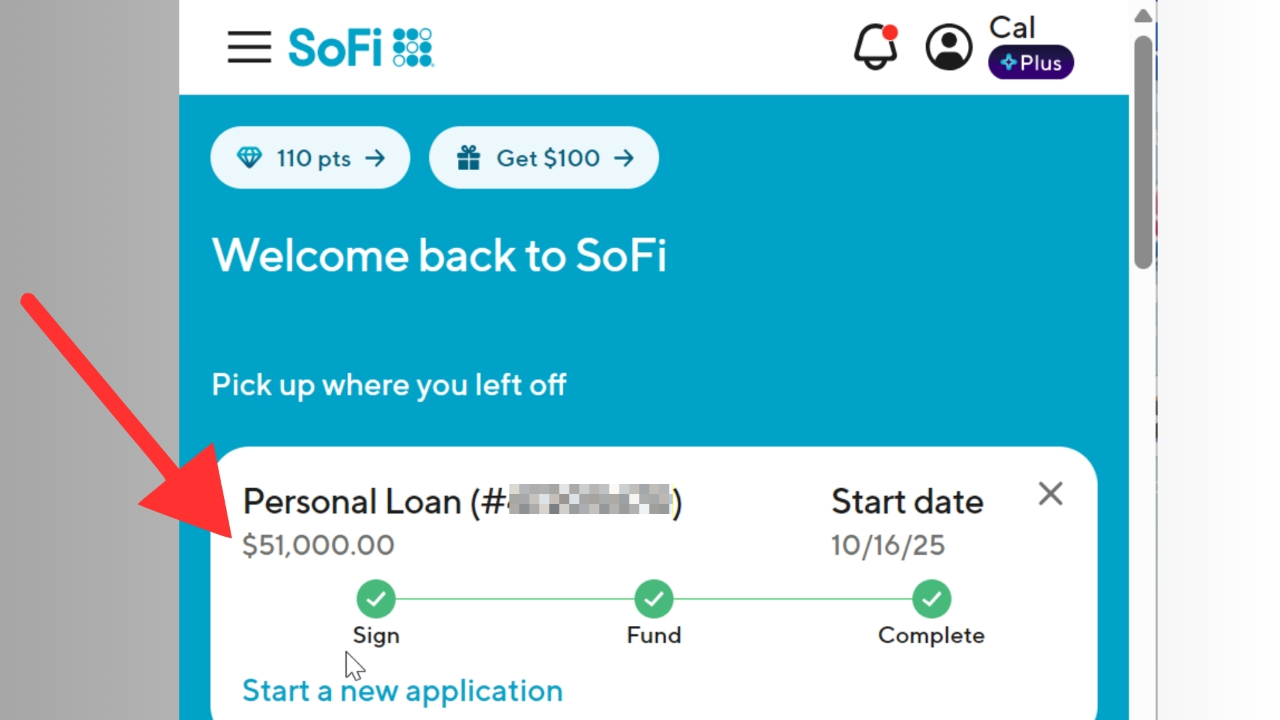

My SoFi Pre-Approval

When I first checked my SoFi pre-approval, it was almost too easy.

I logged in.

Answered a few short questions.

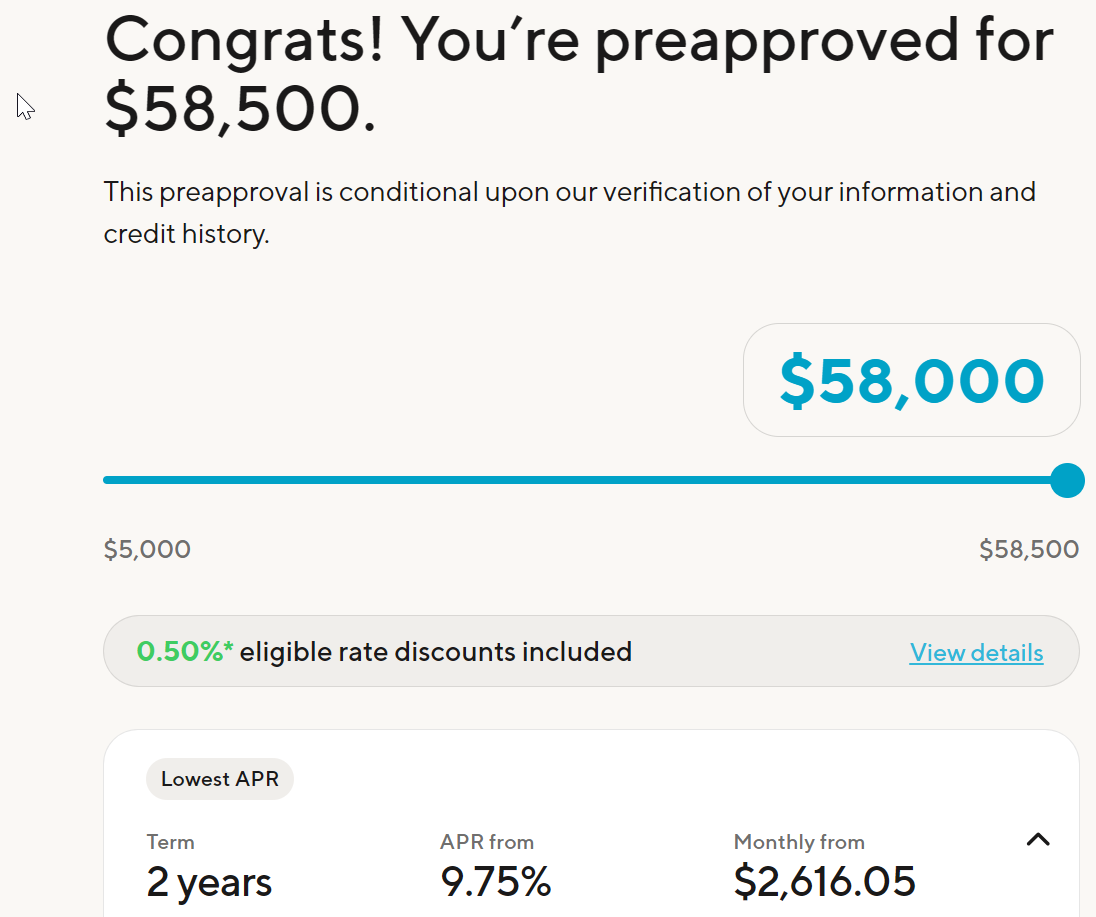

And within about 30 to 40 seconds, SoFi showed that I was pre-approved for up to $58,500.

That number got my attention.

I was not asking for almost $60,000.

But seeing that type of offer on the screen made the whole thing feel real.

It is one thing to think you are fundable.

It is another thing to see a lender show you a number that large.

Still, I did not immediately move forward.

I waited two days.

I wanted to think through the amount, the term, the payment, and whether it actually made sense.

That part matters.

Just because a lender offers you more money does not mean you should take the maximum.

Why I Chose $51,000 Instead of $58,500

SoFi pre-approved me for up to $58,500.

But I chose $51,000.

Why?

Because that was the amount I actually needed.

I did not want to borrow extra money just because it was available.

That is where a lot of people get in trouble with personal loans.

They start with a debt consolidation goal, then decide to take extra cash because the lender offered it.

That can turn a smart move into a bad one.

For me, the purpose was simple:

I wanted to pay off the balances from my 0% APR promo cards before they rolled into high interest.

So I took the amount that fit the plan.

Not the maximum.

The Application Process

Two days after seeing the pre-approval, I logged back in around 9 a.m.

I increased the loan request to $51,000.

I selected debt consolidation as the purpose.

Then I submitted the application.

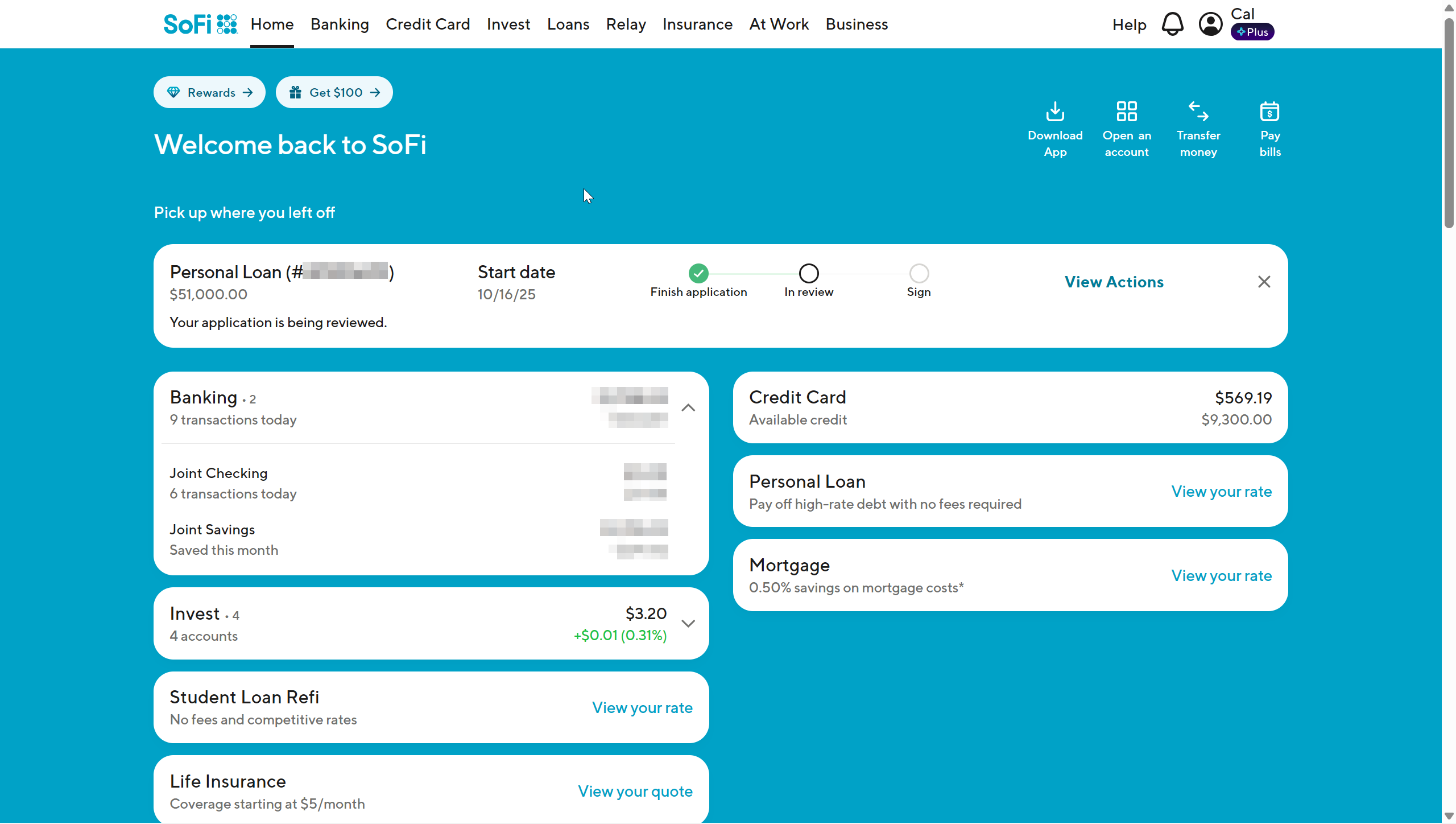

Right away, it went to “under review.”

That part can make you nervous.

But I did not have to wait long.

The final decision came back in less than 20 minutes.

No document request.

No verification email.

No manual upload portal.

No “we need 2 to 3 business days.”

Just an approval.

Then by around 3 to 4 p.m. that same day, the funds were in my SoFi checking account.

That means the full process took roughly five hours from application to funding.

Helpful resource: If you want to check your own SoFi personal loan offer, you can view your rate with a soft pull through my SoFi Personal Loans link: https://calbarton.link/SoFi-Loan

My SoFi Personal Loan Data Points

Here are the exact data points from my approval.

Personal credit profile:

-

Experian FICO 8: Around 765

-

Utilization: About 12%

-

Average age of accounts: 5 years, 1 month

-

Inquiries in the past year: 1

-

Credit mix: 26 bank-issued credit cards and 10 installment loans or mortgages

Loan details:

-

Loan purpose: Debt consolidation

-

Requested loan amount: $51,000

-

Pre-approved amount: Up to $58,500

-

Term selected: 6 years

-

APR: Around 13%

-

Funding speed: Same day, roughly 5 hours

-

Documents required: None

-

Bureau pulled: Experian only in my case

-

Employment setup: W-2 employee through my business payroll

That is a strong profile.

It is not perfect.

But it is clean enough to show what a fundable borrower can look like.

Why I Think SoFi Approved Me With No Docs

The biggest reason I think this approval went so smoothly is my long-term SoFi relationship.

I had been with SoFi for about five or six years.

I had checking and savings with them.

I had their credit card for about four years.

They could already see a lot of my financial behavior.

That matters.

A lender that has no relationship with you may need to ask for proof.

They may need pay stubs.

They may need tax returns.

They may need bank statements.

But if you already bank with the lender, they may have enough internal data to feel comfortable.

SoFi could see my deposits, spending behavior, account history, repayment patterns, and overall relationship.

That does not guarantee no-doc approval.

But in my case, I believe the relationship helped.

Why Debt Consolidation Made Sense

The loan purpose was debt consolidation.

That was not random.

I actually had credit card balances I wanted to consolidate before the 0% APR periods expired.

That is the cleanest use case for a personal loan like this.

Instead of letting multiple credit cards roll into 20% to 30% interest, I moved the debt into one fixed-rate installment loan.

That gave me:

-

One fixed monthly payment

-

A clear payoff schedule

-

Lower stress from fewer due dates

-

Lower revolving utilization

-

Less risk of high-interest rollover

Debt consolidation is not magic.

It only works if you do not run the credit cards back up afterward.

But when used correctly, it can be a powerful reset.

Why You Should Be Honest About Loan Purpose

I want to be clear about this part.

Do not lie about your loan purpose.

If you are using the loan for debt consolidation, then choosing debt consolidation makes sense.

If you are using it for something else, choose the accurate purpose.

Lenders ask the loan purpose because it helps them understand risk.

Debt consolidation can look responsible because you are using the money to simplify or pay down existing debt.

But that does not mean you should select it if that is not what you are doing.

The better move is to match the loan purpose to the actual use.

That keeps the application clean.

Why My Credit Score Could Improve

One reason personal loans can help credit scores is utilization.

Credit card balances affect revolving utilization.

Installment loans are treated differently.

So when you use a personal loan to pay down credit cards, your revolving utilization may drop.

That can help your score.

In my case, the loan allowed me to bring those credit card balances down to zero.

That could potentially push my score higher once the updated balances report.

But results vary.

If your utilization is already low, your score may not move much.

If your utilization is high, the impact can be bigger.

The key is that the credit cards need to actually report lower balances.

And you need to avoid running them back up again.

The Main Benefit: One Payment Instead of Five

Before the loan, I was juggling several credit card balances.

Different due dates.

Different statement dates.

Different promo expiration dates.

Different payments to track.

That gets annoying fast.

The SoFi personal loan simplified everything.

Instead of managing 4 to 5 separate credit card payments, I now had one fixed monthly payment.

That alone has value.

Sometimes the best financial move is not just about the interest rate.

It is about reducing the number of things you have to manage.

One payment is easier to track than five.

Why I Picked a Six-Year Term

SoFi offered me a lower rate on a shorter term.

The lower-rate option was around 9.75%, but it was tied to a two-year term and required linking credit cards for direct payoff during the application.

I chose the six-year term at around 13% instead.

Why?

Flexibility.

The shorter term had a lower rate, but it also came with a higher required monthly payment.

The six-year term gave me more breathing room.

I can still pay the loan off early and reduce the total interest cost.

But I did not want to lock myself into a tight payment schedule just to get the lower rate.

That is a trade-off every borrower needs to think through.

Lowest rate is not always the best option if the payment creates stress.

What SoFi Looked At

SoFi looked at more than just my credit score.

That is how most personal loan underwriting works.

Lenders usually care about:

-

Credit score

-

Income

-

Debt-to-income ratio

-

Existing debt

-

Credit history

-

Recent inquiries

-

Employment stability

-

Banking behavior

-

Relationship history

-

Requested loan amount

-

Loan purpose

My 765 FICO helped.

My low inquiry count helped.

My credit mix helped.

My SoFi banking relationship likely helped.

And the debt consolidation purpose made sense for the situation.

All of that worked together.

The Income Strategy That Actually Matters

When applying for a personal loan, income matters.

But that does not mean you should inflate it.

Report real income.

If household income is allowed and your spouse or partner contributes to household expenses, include it only if the application allows that and it is accurate.

The goal is not to make up a number.

The goal is to report your income correctly so the lender can understand your ability to repay.

If something looks off, the lender may ask for documents.

And if you cannot verify what you reported, that can become a problem.

So be strategic, but stay honest.

Why Being a W-2 Employee Helped

Even though I own my business, I pay myself through payroll.

That means I show up as a W-2 employee through my business.

That can make underwriting cleaner.

Self-employed borrowers can sometimes face extra document requests because lenders may want tax returns, business income verification, profit and loss statements, or bank statements.

Being on payroll can make the income look more consistent.

That does not mean every business owner needs to run payroll just for a loan.

But in my case, I think the W-2 structure helped make the application cleaner.

What I Would Do Before Applying for SoFi

Before applying for a SoFi personal loan, I would check a few things.

First, check your credit score.

Second, check your utilization.

Third, check your recent inquiries.

Fourth, make sure your income is accurate.

Fifth, decide the actual loan purpose.

Sixth, compare the payment across different terms.

Seventh, make sure you can repay the loan without running the credit cards back up.

That last part is critical.

A debt consolidation loan can help.

But if you pay off cards and then charge them up again, you now have the loan and the card debt.

That is how consolidation backfires.

Who a SoFi Personal Loan May Make Sense For

A SoFi personal loan may make sense if:

-

You have good credit

-

You want to consolidate higher-interest credit card debt

-

You want one fixed monthly payment

-

You want to check your rate with a soft pull

-

You need a large loan amount

-

You want to avoid origination or prepayment fees

-

You have a clear payoff plan

This is not for everybody.

But for the right profile, SoFi can be a strong personal loan option.

Who Should Be Careful

Be careful with a personal loan if:

-

Your income is unstable

-

Your credit card balances are still growing

-

You do not have a real payoff plan

-

You are borrowing extra money just because it is offered

-

The monthly payment is too tight

-

You may run the paid-off cards back up again

A personal loan should solve a problem.

It should not create a bigger one.

Frequently Asked Questions

Does SoFi offer personal loan pre-approval?

Yes. SoFi lets you check your rate before submitting a full application. Checking your rate should not affect your credit score, but moving forward with a final application can involve a hard credit pull.

How fast does SoFi fund personal loans?

SoFi says funds may be available as soon as the same day you sign. In my case, I applied in the morning and the funds landed in my SoFi checking account by mid-afternoon.

What credit bureau did SoFi pull for my personal loan?

SoFi pulled Experian only in my case. Your result may vary based on your profile, location, and SoFi’s current underwriting process.

Did SoFi ask me for income documents?

No. I was approved for $51,000 with no W-2s, pay stubs, tax returns, or bank statements required. That does not mean everyone will avoid documents.

Is debt consolidation the best reason for a SoFi loan?

Debt consolidation can be a strong reason if you are actually using the loan to pay down or simplify existing debt. You should choose the loan purpose that honestly matches how you plan to use the funds.

Can a personal loan raise your credit score?

It can help if the loan is used to pay down credit card balances and lower revolving utilization. But results vary, and taking on new debt can also affect your credit profile.

Final Thoughts

SoFi approving me for a $51,000 personal loan with no documents and same-day funding was one of the cleanest personal loan experiences I have tested.

The pre-approval showed up fast.

The final approval came back in under 20 minutes.

The funds landed the same day.

And SoFi did not ask me for W-2s, pay stubs, tax returns, or bank statements.

But I do not think this happened by accident.

My credit profile was strong.

My Experian FICO was around 765.

My inquiries were low.

My relationship with SoFi was several years old.

I had checking, savings, and their credit card.

And the loan purpose matched the actual use case.

That is the real lesson.

Funding is not just about clicking apply.

It is about building the profile before you need the money.

When the relationship, credit profile, income, and loan purpose all line up, approvals can move a lot faster than most people expect.