SoFi Essential Card After Bankruptcy: Can You Get Approved Early?

Jun 26, 2026

One person reportedly got approved for the SoFi Essential Credit Card just four months after bankruptcy discharge.

Their FICO score was still in the 600s.

And they were approved for a $2,000 credit limit.

That is the kind of data point that catches my attention because a lot of people think bankruptcy means they are locked out of credit cards for years.

Not months.

Years.

But this is why rebuilding after bankruptcy is more nuanced than people think.

Some major banks may not want anything to do with you for a while.

But fintech cards, store cards, secured cards, and certain targeted offers may still give you a path back into credit much sooner than expected.

The SoFi Essential Card is one of the more interesting options showing up in that rebuild lane.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Some bankruptcy rebuilders have reported getting approved for the SoFi Essential Credit Card within months of a Chapter 7 discharge, including approvals with FICO scores still in the 600s. The card appears to be targeted through Credit Karma in some cases, and users may need to see the offer before applying. Approval is not guaranteed, but the data points suggest SoFi may be more bankruptcy-friendly than some traditional banks for the right profile.

Two SoFi Essential Approval Data Points After Bankruptcy

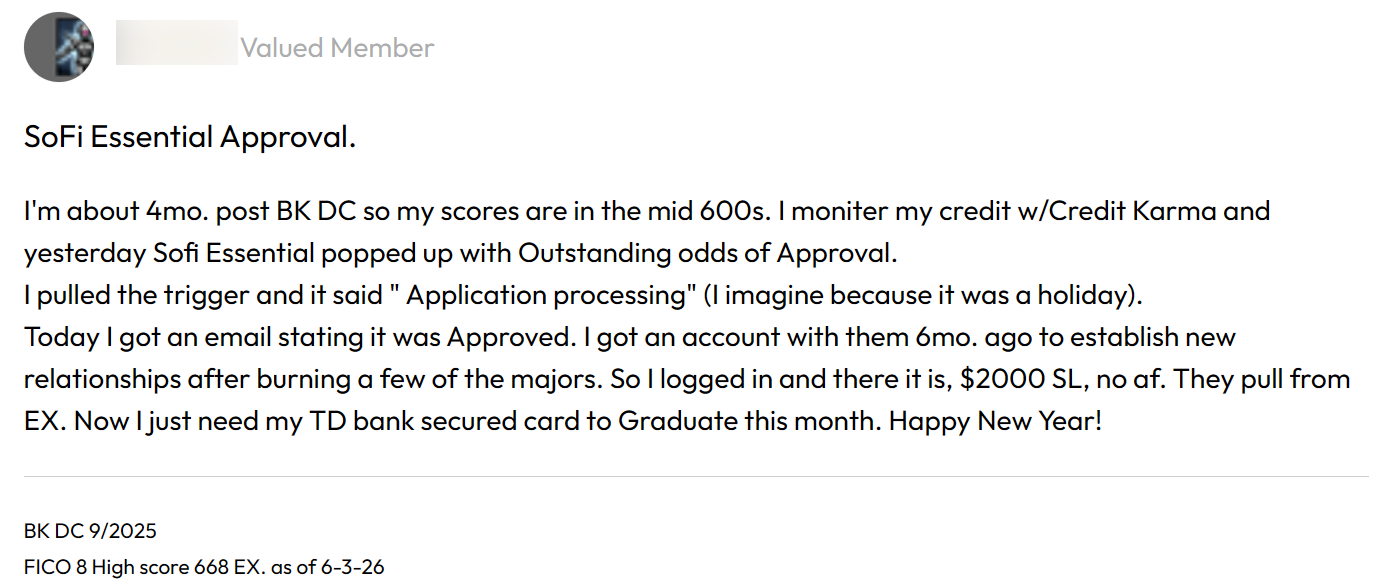

The first data point involved someone about four months post-bankruptcy discharge.

Their scores were reportedly in the mid-600s.

Credit Karma showed them an “Outstanding Odds” offer for the SoFi Essential Card.

They applied and were approved for a $2,000 limit.

The second data point was also a Chapter 7 bankruptcy rebuild.

This person had a thin credit file after bankruptcy with only a couple of cards open.

They kept seeing the SoFi Essential offer in Credit Karma.

Eventually, they applied and were approved for $3,000.

Both were early in their rebuild.

Both were in the 600-score range.

Both had Chapter 7 bankruptcies.

And both got approved.

That does not mean everyone will get the same result.

But it does show that rebuilding after bankruptcy does not always have to wait five to seven years.

What Makes the SoFi Essential Card Interesting?

The SoFi Essential Card is not built like a premium rewards card.

This is not a luxury travel card.

This is not a high-end points card.

This is not a card you get because you want big bonus categories everywhere.

This card is mainly built for people who are trying to build or improve their credit.

The card offers:

-

No annual fee

-

No over-limit fees

-

No returned payment fees

-

No foreign transaction fees

-

3% cash back on SoFi Travel purchases

-

No rewards outside SoFi Travel

-

No required secured-card deposit

-

Credit reporting to the major credit bureaus

That makes it more of a rebuilding tool than a rewards machine.

And that is exactly how I would look at it.

The goal is not to squeeze every possible reward out of the card.

The goal is to rebuild trust with lenders.

This Is a Credit Rebuilding Tool

After bankruptcy, your job is simple.

Show lenders that the old credit problems are behind you.

That means you need clean payment history.

Low utilization.

Time.

And accounts reporting positive activity.

The SoFi Essential Card can help with that if you use it correctly.

You do not need to put huge spending on it.

You do not need to carry a balance.

You do not need to chase rewards.

You just need to use it responsibly.

That may mean putting a small recurring bill on it, paying it in full every month, and letting the positive reporting build over time.

That is boring.

But boring works.

The Big Catch: You May Need a Targeted Offer

One important thing to understand is that the SoFi Essential Card may not be available the same way for everyone.

Based on the data points, some people are seeing the offer inside Credit Karma.

That means this may be a targeted or prequalified-style offer.

In other words, you may not be able to simply search the public internet, land on a normal application page, and apply whenever you want.

You may need to see the offer first.

That is similar to how some other targeted cards show up inside Credit Karma or other credit monitoring platforms.

So if you do not see the SoFi Essential Card offer yet, that does not automatically mean you are denied.

It may just mean the offer has not been targeted to your profile.

Helpful resource: If you are comparing cards while rebuilding, my Free Credit Card & Loan Pre-Approval Master List can help you find options that may let you check your odds before applying: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

SoFi May Pull Experian

Based on the data points being discussed, SoFi may pull Experian as part of the process after you accept the offer.

That matters because after bankruptcy, every hard inquiry counts.

You do not want to apply blindly.

You want to know which bureau may be pulled, what your current report looks like, and whether you are actually seeing a targeted offer before you move forward.

If your Experian report is your weakest report, that could matter.

If your Experian report is cleaner than the others, that could also matter.

Either way, do not ignore the bureau pull.

It is part of the strategy.

The Bigger Lesson: Bankruptcy Does Not End Your Credit Life

A lot of people think bankruptcy means nobody will approve them for years.

That is not always true.

Bankruptcy can absolutely make approvals harder.

Some banks may blacklist you if you included them in the bankruptcy.

Some issuers may require a long waiting period.

Some may not approve you again until the bankruptcy ages.

But other lenders may look at your file differently.

That is where fintech cards, secured cards, and certain co-branded cards can become useful.

They may be more willing to look at your current behavior instead of only focusing on the past.

One Rebuild Sequence That Stood Out

One of the SoFi approval examples was not the person’s first card after bankruptcy.

They had already picked up several cards before the SoFi Essential approval.

The sequence looked like this:

-

Ally Everyday Cash Back: $4,000

-

Bread Cashback: $6,100

-

Credit One Omni Rewards Amex: $10,000

-

Macy’s Amex: $2,000

-

Discover Secured: $200

-

SoFi Essential: $3,000

That is the part that stood out.

This person reportedly burned more than 10 major banks in their bankruptcy, including names like Amex and Bank of America.

But they still rebuilt into multiple approvals.

And the total available credit was over $25,000 in under a year and a half.

That is a completely different picture from the idea that bankruptcy means you are stuck for five to seven years with no real options.

Why This Sequence Worked

The sequence worked because they were not only chasing major legacy banks right away.

They used a mix of cards that can be more flexible for rebuilders.

That included:

-

Fintech-issued cards

-

Co-branded store cards

-

Credit builder or rebuild-friendly cards

-

A secured card that can potentially graduate

-

Targeted offers showing through Credit Karma

That is usually a smarter rebuild path.

Because if you burned major banks in bankruptcy, going right back to those same banks may not work immediately.

But other issuers may still be willing to give you a shot.

Then, once you build positive history again, bigger doors can start opening later.

Why Fintech and Co-Branded Cards Can Be More Flexible

A big reason these cards can work after bankruptcy is that fintechs and co-branded cards may not always underwrite the same way traditional banks do.

Some lenders may care more about:

-

Current income

-

Current payment behavior

-

Current credit activity

-

Bank account patterns

-

Thin-file risk

-

Education level

-

Recent rebuild progress

That does not mean they ignore bankruptcy.

But they may not treat it the same way a major bank does.

That difference matters.

If one bank is focused heavily on the bankruptcy itself, another lender may be more interested in what your credit behavior looks like after discharge.

That is why rebuild strategy matters.

Do Not Confuse Approval With a Spending Invitation

Getting approved after bankruptcy is exciting.

But it can also be dangerous if you treat the approval like permission to spend.

That is not the goal.

The goal is to rebuild.

So if you get a $2,000 or $3,000 limit, I would not run it up.

I would not carry a balance.

I would not use the card to create another debt problem.

I would use it carefully.

Put a small bill on it.

Pay it in full.

Keep utilization low.

Let it report.

Repeat.

That is how you turn the card into a rebuild tool instead of a new problem.

How to Use the SoFi Essential Card After Bankruptcy

If you get approved for the SoFi Essential Card after bankruptcy, I would keep the strategy simple.

Use the card for one or two boring expenses.

For example:

-

Gas

-

Groceries

-

A small utility bill

-

A streaming subscription

-

A phone bill

Then pay the balance in full every month.

The key is to keep utilization low.

Ideally, under 10% if possible.

So if the limit is $2,000, try not to let more than around $200 report.

If the limit is $3,000, try not to let more than around $300 report.

That does not mean you can never spend more.

But for credit rebuilding, low reported utilization can help your profile look cleaner.

What to Do Before Applying

Before applying for the SoFi Essential Card or any card after bankruptcy, I would do a few things first.

Check your credit reports.

Make sure your bankruptcy discharge is reporting correctly.

Make sure included accounts show properly.

Make sure there are no incorrect balances reporting on discharged debts.

Then check your current scores.

Look for prequalified offers.

And be honest about whether you are ready for new credit.

If you are still missing payments or struggling with cash flow, the priority may not be another credit card yet.

The priority may be stabilizing your finances first.

A Smarter Rebuild Path After Bankruptcy

If you are rebuilding after bankruptcy, I would think in stages.

Stage one is stability.

Make sure your reports are accurate.

Make sure your budget works.

Make sure you are not behind on anything current.

Stage two is your first rebuild accounts.

That might include:

-

A secured card

-

A credit builder account

-

A fintech card

-

A targeted prequalified offer

-

A store or co-branded card

Stage three is responsible usage.

Pay on time.

Keep utilization low.

Avoid applying too much.

Let accounts age.

Stage four is moving back toward better cards.

That might take time.

But the timeline can be faster than people think when the rebuild is done properly.

Helpful resource: If you are trying to rebuild credit after bankruptcy or past credit problems, Kovo may be worth researching as a credit-building option: https://offers.calbartoncashback.com/Kovo

How Fast Can You Rebuild After Bankruptcy?

Every profile is different.

But I have seen people make serious progress within 18 to 24 months when they rebuild correctly.

That does not mean bankruptcy disappears.

Chapter 7 bankruptcy can stay on your credit report for years.

But your score can still improve before the bankruptcy falls off.

That is because credit scoring also looks at your current behavior.

If you stack positive payment history, keep utilization low, avoid new missed payments, and stop applying randomly, you can start rebuilding the file.

The bankruptcy is still there.

But it does not have to define every future approval.

What You Can Do Next

If you are trying to rebuild after bankruptcy, here is the simple version.

First, check your Credit Karma dashboard regularly.

If the SoFi Essential Card shows up as a targeted offer, read the terms carefully before applying.

Second, start with easier prequalified options.

Do not jump straight into cards that are known to be unfriendly after bankruptcy.

Third, use any new card lightly.

One or two small bills is enough.

Fourth, pay in full every month.

Do not rebuild your way back into debt.

Fifth, keep utilization low.

Under 10% is a good goal when possible.

Finally, give the process time.

A lot can change in 18 to 24 months if you keep your reports clean and use credit responsibly.

Frequently Asked Questions

Can you get the SoFi Essential Card after bankruptcy?

Some users have reported getting approved for the SoFi Essential Card after Chapter 7 bankruptcy, including approvals within months of discharge. Approval is not guaranteed, but the card appears to be showing up for some bankruptcy rebuilders through targeted offers.

Is the SoFi Essential Card secured?

The SoFi Essential Card is not positioned like a traditional secured card that requires a deposit to set your credit limit. That makes it different from cards where you must put down $200 or more just to open the account.

Does the SoFi Essential Card have an annual fee?

No. The SoFi Essential Card has no annual fee, which can be helpful for rebuilders who want to keep an account open long term without paying to maintain it.

Does the SoFi Essential Card earn rewards?

The card earns 3% cash back on SoFi Travel purchases. Outside of SoFi Travel, it is not really a rewards card. It is better viewed as a credit-building tool.

Where do you apply for the SoFi Essential Card?

Some data points show the SoFi Essential Card appearing as a targeted offer inside Credit Karma. If you do not see it, you may not currently be targeted for the card.

What should I do after getting approved after bankruptcy?

Use the card lightly, pay it in full every month, keep utilization low, avoid random applications, and let positive payment history build. The goal is rebuilding trust, not chasing spending power too fast.

Final Thoughts

The SoFi Essential Card is not exciting in the traditional rewards-card sense.

But for someone rebuilding after bankruptcy, it may be interesting for a completely different reason.

It gives some people a shot earlier than expected.

A $2,000 or $3,000 credit limit a few months after Chapter 7 discharge is not something to ignore.

That can be a real tool if you use it correctly.

But the strategy matters.

Do not treat an approval like permission to spend.

Treat it like a chance to rebuild.

Keep the balance low.

Pay on time.

Let the account age.

And use the card to prove that your credit behavior after bankruptcy is different from what happened before.

Because rebuilding after bankruptcy is not about getting every bank to forgive you immediately.

It is about finding the lenders that will give you a chance, using those accounts responsibly, and slowly earning your way back into stronger approvals.