Revenued Review: EIN-Only No PG Business Funding With No Hard Pull

Jun 26, 2026

If you are building your business on top of your personal credit right now, there is a good chance one bad month could cause your business problems to spill directly onto your personal credit report.

Every time the business needs money, your utilization spikes.

Your score drops.

Your debt-to-income climbs.

And eventually, it starts feeling like your business life and personal life are financially glued together.

That is why more business owners are starting to pay attention to EIN-only business funding.

No personal guarantee.

No hard pull.

And business credit reporting tied to the EIN instead of your personal credit profile.

One product in that space that stands out is Revenued.

Revenued is an EIN-only no-PG business card and flex line that is based mainly on business revenue and banking activity, not your personal FICO score.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links. This article is sponsored by Revenued, but the goal is to give you the full picture, including what I like, what I do not like, and who I think should avoid it.

Quick Answer

Revenued is an EIN-only business card and flex line that may offer business funding with no personal guarantee and no hard inquiry on your personal credit. It is mainly based on business revenue, deposits, and banking activity instead of your personal FICO score. This can be useful for business owners trying to separate business funding from personal credit, but the repayment structure can be expensive and may not fit businesses with tight or unpredictable cash flow.

What Is Revenued?

Revenued is not a traditional business credit card.

It is better understood as an EIN-only business card and flex line that mainly looks at business revenue and banking activity.

That means the approval process is not built around your personal credit score the same way a traditional business credit card might be.

Revenued may offer:

-

No personal guarantee

-

No hard inquiry on your personal credit

-

Approval based mostly on business deposits and banking activity

-

Access to funds through a Visa business card

-

Access to direct cash draws

-

Business credit reporting to Dun & Bradstreet

That is why the EIN-only angle gets people excited.

Because most business funding eventually circles back to your personal credit somehow.

Your SSN.

Your utilization.

Your personal score.

Your personal risk.

So when business owners hear “no PG,” “no hard pull,” “EIN-only approval,” and “business credit reporting,” it immediately grabs attention.

Especially if they already have elevated utilization, multiple inquiries, or too many business expenses sitting on personal credit cards.

Helpful resource: If Revenued sounds like it may fit your business, you can check your eligibility and learn more here without a hard pull on your personal credit: https://offers.calbartoncashback.com/Revenued

The Big Tradeoff: This Is Usually Not Cheap Money

This is the part you cannot ignore.

Revenued can be useful in the right situation, but this usually is not cheap money.

Depending on your approval terms, repayments may come out:

-

Daily

-

Weekly

-

Monthly

That changes the entire conversation.

Because now you are not just asking:

“How much funding can I get?”

You are asking:

“How does this affect my cash flow every single week?”

That is the real question.

A funding product can look attractive at first because there is no hard pull, no personal guarantee, and no personal credit balance reporting.

But if the repayment structure drains your cash flow, that creates a different problem.

This works best when the business already has real revenue, predictable deposits, and a clear plan for using the money.

It does not work well when the business is already financially cornered.

Who Revenued Is Actually Best For

Revenued is not really designed for brand-new businesses with no activity.

Generally speaking, this is a better fit for businesses that:

-

Have been operating for at least one year

-

Have real business revenue

-

Use an active business bank account

-

Have consistent deposits

-

Have around $20,000 or more in monthly business deposits

-

Keep business and personal finances separate

That separate business bank account piece matters.

This is not ideal for someone mixing personal and business expenses in the same account.

From what I understand, Revenued is generally built more for:

-

LLCs

-

Corporations

-

Partnerships

It may not be the best fit for sole proprietors.

The business owner who is most likely to benefit from something like this is someone who already has revenue coming in, needs faster working capital, and wants to avoid hammering their personal credit profile every time the business needs money.

My Personal Revenued Approval Experience

Here is how my own Revenued approval worked.

Once my business revenue and deposits increased, I decided to apply.

The application was straightforward.

I connected my business bank account through Plaid.

After underwriting reviewed the account, I got a conditional approval in around 20 minutes.

And honestly, that is the part that stood out to me.

The decision was tied mainly to business activity.

Not my personal FICO score.

I can confirm there was no hard inquiry on my personal credit.

I can also confirm there was no new balance reporting to my personal credit afterward.

That is a very different experience compared to traditional business funding.

After the conditional approval, Revenued requested:

-

My driver’s license

-

A bank verification letter from Bluevine

I submitted both documents and then scheduled a call with Sam, my account manager at the time.

He walked me through how the flex line worked and explained that accounts are reviewed every four to six weeks for possible limit increases.

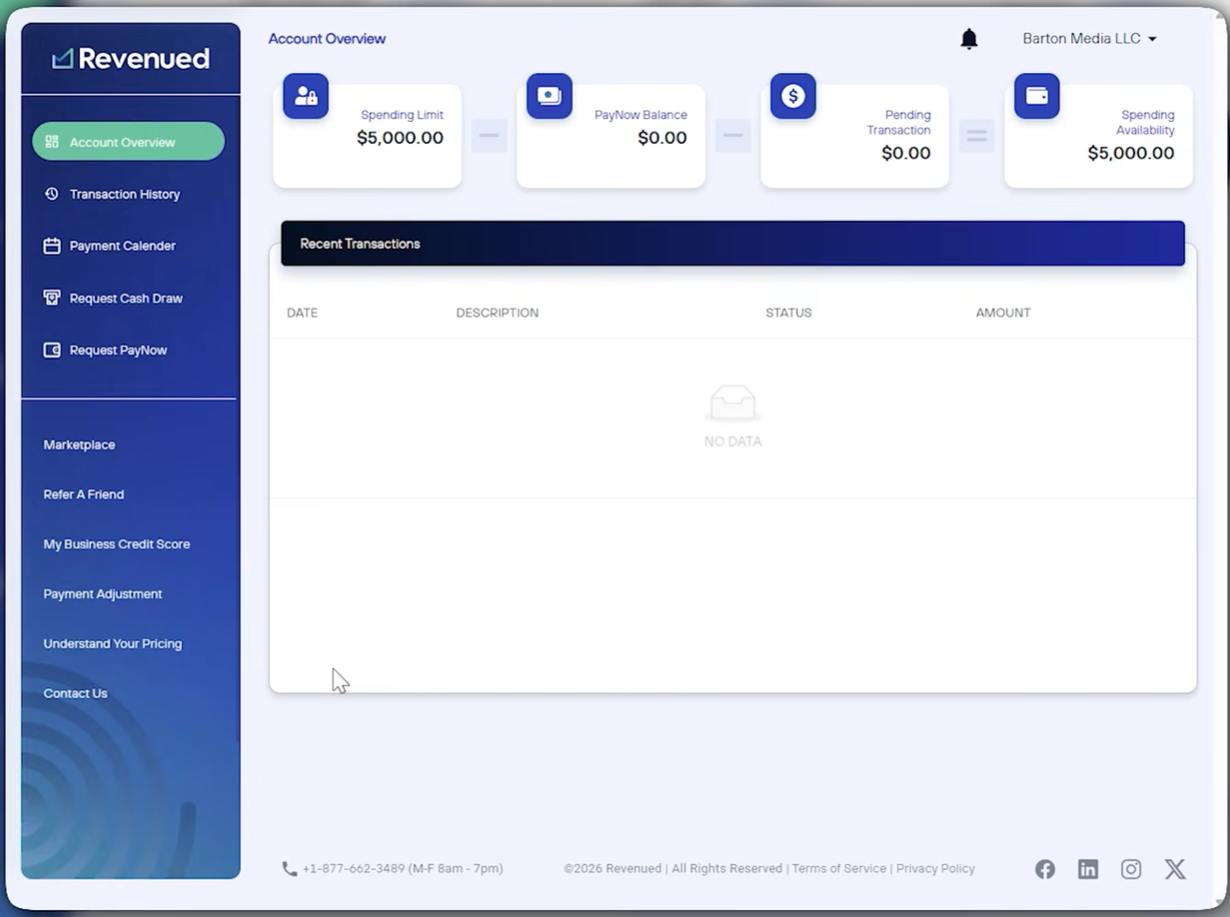

My starting limit ended up being $5,000.

That is not massive.

But Revenued uses more of a growth-based model.

You may start smaller, then scale based on usage, repayment history, and overall business performance over time.

According to Revenued, some businesses can eventually scale anywhere from around $150,000 to as high as $750,000 depending on cash flow and repayment history.

After I signed the agreement, I received the “Welcome to Revenued” email less than 24 hours later.

Inside the account, I had:

-

Immediate online access

-

A virtual card instantly available

-

Physical card shipping later

-

Direct cash draw access to my business bank account

The biggest thing for me was simple:

My personal credit profile was still untouched afterward.

What I Like About Revenued

The biggest thing I like about Revenued is the EIN-only and no-PG structure.

That is still uncommon.

Especially for businesses trying to avoid loading more debt onto personal credit cards.

Other things I liked:

-

Fast decisions once accounts are connected properly

-

No hard inquiry on personal credit

-

No personal credit balance reporting

-

Ability to draw cash directly

-

Visa business card access

-

Dedicated U.S.-based reps

-

Business credit reporting to Dun & Bradstreet

For a business owner trying to separate business funding from personal credit, those features matter.

Because one of the biggest traps in business funding is relying on personal credit forever.

Eventually, that can create problems.

Your business expenses start affecting your personal score.

Your personal utilization gets too high.

Your debt-to-income looks worse.

Your personal credit becomes the funding engine for everything.

Revenued can help some business owners start moving away from that.

What I Do Not Like About Revenued

Now let’s talk about the part I do not like as much.

The repayment structure.

Depending on your offer, some business owners may get daily repayments.

And for some people, that can start feeling more like MCA-style financing.

For example, one of my community members named Charles was approved for around $40,000.

But he told me:

-

The repayments were daily

-

The factor rate was around 1.44

-

He personally did not love the structure

This is where a lot of business owners misunderstand products like this.

Some people hear “1.44 factor rate” and think:

“Okay, so the cost is 44%.”

But when repayments are coming out daily, the effective cost of the money can become dramatically higher than it first sounds.

Why?

Because you are constantly paying principal back almost immediately.

That means you need to understand the true cash-flow impact.

Not just the approved amount.

Not just the factor rate.

Not just the fact that there is no hard pull.

You have to ask:

“How expensive is this money really once repayments start hitting my account every day?”

That is how business funding should be evaluated.

Run the numbers.

Understand the repayment schedule.

Then decide whether the money actually helps your business.

Why Cash Flow Matters So Much

Revenued may make sense when the money is being used intentionally.

It may not make sense when the business is already under financial pressure and just trying to survive another week.

That is a huge difference.

If your business has strong deposits, consistent revenue, and a clear use for the funds, this type of product may help bridge temporary gaps.

But if your margins are thin and daily repayments would make it hard to operate, you need to be careful.

Funding is not just about getting approved.

It is about whether the repayment structure fits your business.

A $40,000 approval can sound great.

But if the daily repayment crushes your operating cash flow, it may not be a good deal.

A Real Business Example: Sawyer Services

One real business example is Sawyer Services.

They are an HVAC and handyman company operating across parts of the Carolinas and Georgia.

A couple years ago, it was basically the owner and one technician.

Together, they generated around $670,000 in revenue.

Eventually, the owner’s wife joined the business full-time too.

Now they have real payroll, real expenses, and real pressure.

About a year ago, they joined Revenued.

And according to them, it became a lifesaver during cash-flow crunches.

They used it for:

-

Payroll

-

Operating expenses

-

Home Depot purchases

-

Keeping money moving while waiting on slow-paying customers

At one point, they had a customer delay payment for almost 140 days on a $60,000 invoice.

Think about that.

Payroll still has to go out.

Materials still need to be purchased.

Rent, supplies, insurance, and operating expenses still exist.

The business still has to function.

That is where a product like Revenued can make sense.

Not as random debt.

But as a bridge when the business has real revenue, real receivables, and a temporary cash-flow gap.

When Revenued Can Make Sense

Revenued may make sense if:

-

Your business has consistent monthly deposits

-

You already have real revenue

-

You need fast working capital

-

You understand the repayment structure

-

Your margins can support the payments

-

You want to avoid using more personal credit

-

You need access to both card spending and cash draws

-

You are trying to build business credit reporting through the EIN

This is not about getting money just because it is available.

That is how people get hurt.

This is about using the money with a plan.

For example, it may make sense for bridging a temporary cash-flow gap, covering payroll while waiting on invoices, buying materials for a job, or handling short-term operating expenses tied to revenue.

When Revenued May Not Make Sense

Revenued may not be a good fit if:

-

Your business has unstable deposits

-

You do not have predictable cash flow

-

You are already behind on obligations

-

You do not know what the money will be used for

-

Daily repayments would strain the business

-

You are using it to cover a deeper profitability problem

-

You are not separating business and personal finances

-

You are a brand-new business with little or no revenue

This is where I want business owners to be honest.

No-PG funding sounds attractive.

No hard pull sounds attractive.

EIN-only approval sounds attractive.

But none of that matters if the repayment structure does not fit your business.

The wrong funding at the wrong time can make things worse.

Before You Apply, Ask Yourself These Questions

Before applying for something like Revenued, I would ask:

-

Am I doing real, consistent business deposits?

-

Is my business bank account active and clean?

-

Do I understand exactly how repayments work?

-

Can my margins realistically support this?

-

Do I know what the money will be used for before I apply?

-

Am I using this to move toward business-based funding?

-

Am I trying to avoid stacking more personal debt?

-

Would daily or weekly repayments create cash-flow pressure?

-

Do I have a plan to repay this without hurting operations?

That checklist matters.

Because the goal is not just to get approved.

The goal is to use funding in a way that actually helps the business.

Frequently Asked Questions

Is Revenued a traditional business credit card?

No. Revenued is not a traditional business credit card. It is more like an EIN-only business card and flex line based mainly on business revenue, deposits, and banking activity.

Does Revenued require a personal guarantee?

Revenued is positioned as a no-PG business funding option. That means it may not require a personal guarantee, but you should always review your specific agreement before accepting any offer.

Does Revenued do a hard pull?

In my experience, Revenued did not do a hard inquiry on my personal credit. The decision was mainly tied to business deposits and banking activity.

Does Revenued report to business credit?

Revenued reports to Dun & Bradstreet, which may matter for business owners trying to build more funding activity around the EIN instead of relying only on personal credit.

What kind of business is Revenued best for?

Revenued is generally better for businesses with at least one year in operation, active business banking, consistent revenue, and around $20,000 or more in monthly business deposits.

Is Revenued expensive?

It can be. The cost depends on your specific terms, repayment schedule, and factor rate. Daily repayments can make the effective cost feel much higher than it first appears, so you need to run the numbers before accepting an offer.

Final Thoughts

Revenued is one of the more interesting EIN-only no-PG business funding options right now.

The biggest benefit is obvious:

It can help some business owners access funding without a hard pull, without a personal guarantee, and without adding a new balance to personal credit.

That matters.

Especially if you are trying to stop using personal credit cards as your business funding engine.

But this is not free money.

And it is not cheap money for everyone.

The repayment structure can be aggressive, especially if your offer includes daily payments.

So before applying, be honest about your revenue, deposits, margins, and cash flow.

For the right business, Revenued can be a useful bridge.

For the wrong business, it can become expensive fast.

That is the full picture.

If your business has real revenue, consistent deposits, and you want to explore business-based funding without a hard pull on your personal credit, Revenued may be worth checking out.