How I Removed 4 Experian Hard Inquiries in Under 20 Minutes

Jun 27, 2026

I removed four Experian hard inquiries from my personal credit report in under 20 minutes.

And my FICO score jumped 8 points almost instantly.

If you are trying to clean up your credit before applying for credit cards, personal loans, or business funding, hard inquiries matter more than people think.

Yes, inquiries are only one part of your score.

But lenders do not only look at your score.

Some banks have strict rules around how many recent inquiries they will allow, even if your score is strong.

That is why keeping inquiries low can matter, especially if you are preparing for multiple rounds of funding.

But before you start disputing everything, I need to be very clear.

You should not dispute legitimate inquiries you knowingly authorized.

And you definitely should not say an inquiry was unauthorized if you know you applied.

That can create bigger problems than the inquiry itself.

This process is for inquiries that are inaccurate, unauthorized, not attached to an active account, or tied to a business account that does not report to your personal credit file.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I removed four Experian hard inquiries by reviewing my Experian report, identifying inquiries that were not tied to active personal accounts, calling Experian, and asking to speak with the department that handles unauthorized inquiries and fraud-related disputes. The representative told me it could take 24 to 72 hours, but in my case the inquiries were marked under dispute within minutes and removed in under 20 minutes. Your results can vary, and you should only dispute inquiries that are inaccurate or unauthorized.

Why Hard Inquiries Matter

Hard inquiries are part of the “new credit” category in FICO scoring.

That category is smaller than payment history or utilization, but it still matters.

A single inquiry usually is not the end of the world.

But several recent inquiries can start creating problems.

Not just for your score.

For underwriting.

A lender may see multiple recent inquiries and think:

“This person is looking for too much credit too quickly.”

That can hurt you even if your score looks good.

This is especially important if you are trying to get business credit cards, 0% APR cards, personal loans, or credit union approvals.

Some banks are sensitive to recent inquiries.

Some lenders are sensitive to inquiries on specific bureaus.

And if you are building a funding sequence, inquiry management becomes part of the strategy.

Do Not Dispute the Wrong Inquiries

This is the most important warning in the entire article.

Do not dispute hard inquiries that are tied to open personal credit accounts you actually applied for.

That can backfire.

For example, imagine you dispute an inquiry connected to a credit card you still use.

If the lender receives a fraud-related dispute or sees that you are challenging the inquiry, it could trigger a review.

In a worst-case scenario, that could lead to account restrictions, account closure, or additional verification.

That would be a terrible trade.

Removing one inquiry is not worth losing a valuable credit card or loan account.

Before disputing anything, slow down and match each inquiry to the account behind it.

You want to know exactly what you are challenging before you call or submit a dispute.

Which Inquiries May Be Worth Reviewing?

The inquiries that may be worth reviewing are usually ones that fall into one of these categories:

-

You do not recognize the company

-

You did not apply for credit with that company

-

The inquiry is not connected to any active personal account

-

The inquiry came from a business credit application that does not report to personal credit

-

The inquiry appears duplicated or inaccurate

-

You believe the inquiry was made without proper authorization

That does not automatically mean it will be removed.

But those are the types of inquiries that may be worth questioning.

The goal is not to remove accurate information just because you do not like it.

The goal is to correct information that does not belong on your report.

Start by Reviewing Your Credit Report

Before calling anyone, review your credit report carefully.

Do not rely only on memory.

Pull up your report and look at the inquiry section.

Write down:

-

The inquiry name

-

The inquiry date

-

Whether it is a hard inquiry

-

Whether it connects to an open account

-

Whether you recognize the lender

-

Whether it may be tied to a business credit application

This part matters because when you speak with a representative, you need to be specific.

Do not just say:

“I want all my inquiries removed.”

That sounds messy.

Instead, you want to say:

“I want to dispute this specific inquiry because I do not recognize it, and it is not tied to any account I opened.”

The more precise you are, the better.

Where to Check Your Experian Report

For Experian specifically, the easiest place to start is Experian.com or the Experian app.

That gives you a direct look at what Experian is reporting.

In my case, Experian.com was useful because I could see updates quickly.

I could monitor when the inquiries moved into dispute status.

Then I could see when they disappeared.

Just remember, Experian only shows you the Experian side.

If you want to review all three bureaus, you should also check Equifax and TransUnion.

Use AnnualCreditReport.com for All Three Reports

Another free option is AnnualCreditReport.com.

That is the official website for free credit reports from Experian, Equifax, and TransUnion.

It is not the fanciest tool in the world, but it gives you a full view of your credit reports.

That matters because an inquiry may appear on one bureau and not the others.

If you are preparing for credit card approvals or business funding, you need to know what is sitting on each report.

Experian may look clean.

TransUnion may not.

Equifax may have something different.

Do not assume all three reports match.

Use Ctrl + F to Find Inquiries Faster

Once you have your report open, use Ctrl + F on your computer.

Search for terms like:

-

“Inquiry”

-

“Inquiries”

-

The lender name

-

The bank name

-

The creditor name

This can help you move through the report faster instead of scrolling endlessly.

Then write down the exact inquiry name and date exactly as it appears.

You will need that information later if you call or dispute online.

How I Contacted Experian

After reviewing my report, I called Experian.

The number I used was:

714-830-7000

From there, I worked through the automated system and tried to reach a live representative.

When prompted, I selected the business option.

Then once I reached someone, I asked to speak with the department that handles special services or unauthorized inquiry disputes.

Different reps may use different names for the department.

Some may describe it as special services.

Some may route it through fraud-related support.

The main thing is that you want the department that can handle unauthorized or inaccurate inquiries.

Fraud Alerts Are Optional

During the process, you may be asked about adding a fraud alert.

A fraud alert can be useful if you are actually worried about identity theft.

But it can also add extra verification steps when you apply for credit.

So do not add one casually just because you are trying to remove an inquiry.

If you believe you are dealing with real identity theft, a fraud alert may make sense.

If you are only disputing an inaccurate inquiry and you do not believe your identity is being misused, think carefully before adding one.

The goal is to protect your credit without creating unnecessary friction for future applications.

What to Say When You Reach the Right Department

When you reach the right department, stay calm and direct.

You can say something like:

“I’m reviewing my Experian credit report and I see hard inquiries that I do not recognize and that are not tied to any active personal accounts I opened. I’d like to dispute these as unauthorized or inaccurate inquiries.”

Then provide the inquiry names and dates one by one.

Do not exaggerate.

Do not claim identity theft unless you genuinely believe identity theft occurred.

Do not say you filed complaints with the CFPB, FTC, or Experian by mail unless you actually did.

Just explain the facts clearly.

That is enough.

What If the Rep Pushes Back?

If the representative pushes back, do not get emotional.

Stay polite.

You can repeat:

“I understand. I’m not asking to remove legitimate inquiries tied to accounts I opened. I’m only disputing these specific inquiries because I do not recognize them and they are not connected to any active personal account I authorized.”

If needed, ask:

“Can you please note the reason for the dispute as unauthorized or inaccurate inquiry and submit it for review?”

You may need to repeat yourself.

That is normal.

The goal is to stay consistent, calm, and specific.

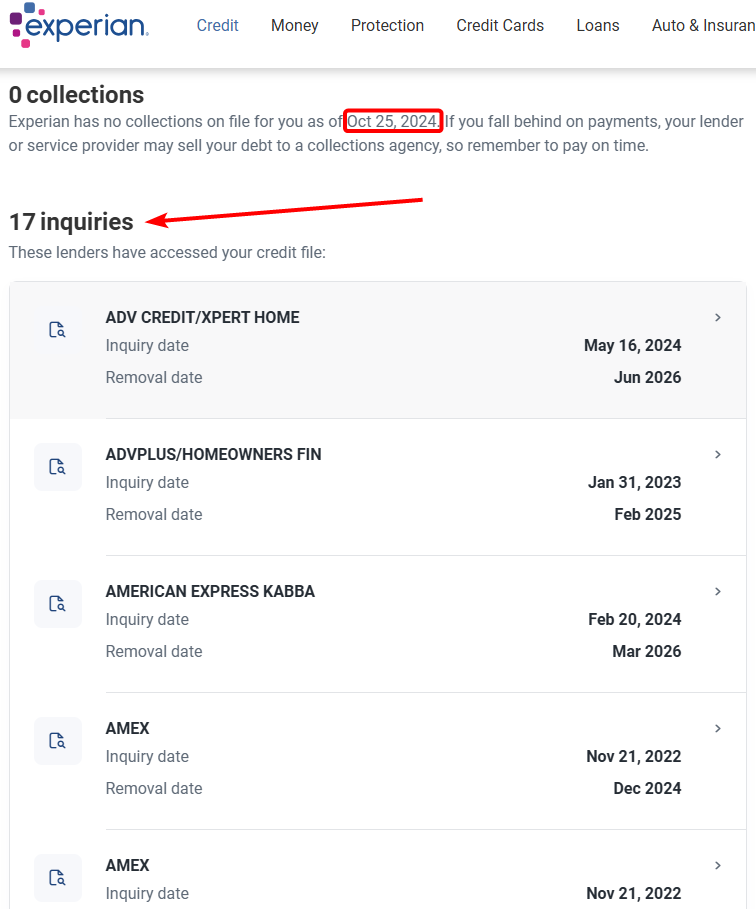

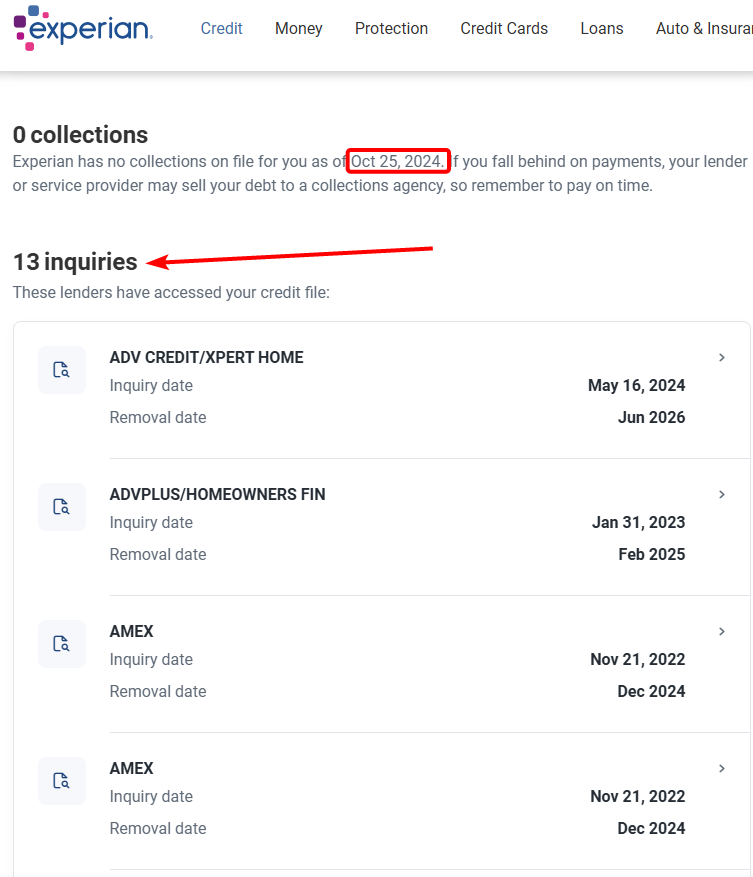

What Happened in My Case

In my case, the representative told me the process could take 24 to 72 hours.

But the actual update happened much faster.

Within about 5 minutes after the call, the inquiries were marked as under dispute.

Within about 20 minutes, all four inquiries were deleted from my Experian report.

Then my FICO score jumped 8 points.

That was a strong result.

But I would not promise everyone the same timeline.

Some people may see results quickly.

Others may wait days.

Others may have inquiries verified and left on the report.

That is why you should treat this as one data point, not a guaranteed outcome.

Why My Score Jumped 8 Points

My score increase made sense because the removed inquiries pushed me below a recent-inquiry threshold.

Before the removal, I had more recent inquiries showing.

After the removal, I had fewer than three inquiries in the past six months.

That can matter.

Credit scoring models do not treat every file exactly the same.

One person may lose only a few points from inquiries.

Another person may see a bigger change if the inquiries are recent, clustered, or pushing them over certain thresholds.

In my case, four removed inquiries produced an 8-point increase.

Your result could be smaller, larger, or no change at all.

Why This Matters for Business Funding

If you are trying to get business funding, Experian inquiries can matter a lot.

Many business credit card issuers pull Experian.

If your Experian report is crowded with recent inquiries, it can hurt your approval odds.

It can also make lenders more cautious about your starting limit.

That is why cleaning up inaccurate inquiries before applying can help.

But again, only dispute what is inaccurate or unauthorized.

Do not try to remove legitimate inquiries connected to accounts you opened just to make your report look cleaner.

That is not the right move.

A Smarter Way to Avoid Future Inquiries

Removing inaccurate inquiries is one thing.

Avoiding unnecessary inquiries in the first place is even better.

Before applying for credit, look for:

-

Soft-pull preapprovals

-

Cards that show your offer before a hard pull

-

Banks that reveal your starting limit before approval

-

Data points about which bureau the bank pulls

-

Clear application rules before submitting

That can save you from wasting hard pulls on denials or tiny limits.

Helpful resource: If you want to avoid applying blindly, my Free Credit Card & Loan Pre-Approval Master List can help you find cards and lenders that may let you check your odds before risking a hard pull: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Using Bureau Pull Data for Business Credit

Once your inquiries are cleaned up, you can plan your next applications more strategically.

The problem is most banks do not clearly advertise which credit bureau they pull.

That makes business funding harder to plan.

If you are trying to build a 0% APR business credit card strategy, bureau pull data matters.

For example, if you just cleaned up Experian, you may want to know which banks are most likely to pull Experian.

If TransUnion is cleaner, you may want to target banks that pull TransUnion.

If Equifax has fewer inquiries, that changes the strategy too.

Helpful resource: My 0% APR Business Credit Card Database includes hundreds of banks and credit unions offering 0% APR business credit cards, including bureau pull data to help you plan applications more strategically: https://courses.calbartoncashback.com/0-apr-business-cards-1

Frequently Asked Questions

Can you remove hard inquiries from Experian?

You can dispute hard inquiries that are inaccurate, unauthorized, duplicated, or not tied to any account you authorized. Legitimate hard inquiries from applications you knowingly submitted generally should not be removed just because you want them gone.

How long do hard inquiries stay on your credit report?

Hard inquiries can stay on your credit report for up to two years. FICO scoring usually focuses more on recent inquiries, but lenders may still look at inquiry history during underwriting.

Will removing hard inquiries increase my credit score?

It can, but it depends on your profile. In my case, removing four Experian inquiries resulted in an 8-point FICO increase. Your score may increase less, more, or not at all.

Should I dispute inquiries tied to open credit cards?

Be very careful. If the inquiry is connected to an active account you opened, disputing it could create problems with that lender. Do not dispute legitimate inquiries tied to accounts you knowingly applied for.

Is a fraud alert a good idea?

A fraud alert can be useful if you believe you are a victim of identity theft. But it can also create extra verification steps for future credit applications, so do not add one casually if identity theft is not actually the issue.

What is the best way to avoid hard inquiries?

The best way is to use soft-pull preapproval tools, research bureau pull data, and avoid applying blindly. Preapproval is not a guarantee, but it gives you more information before risking a hard inquiry.

Final Thoughts

Removing four Experian hard inquiries in under 20 minutes was one of the fastest credit report changes I have seen personally.

My inquiries moved into dispute status within minutes.

Then they disappeared.

And my FICO score jumped 8 points.

That was a great result.

But the bigger lesson is not just how fast it happened.

The bigger lesson is that you need to manage inquiries carefully.

Do not dispute legitimate inquiries just because you regret applying.

Do not claim fraud if you know you authorized the application.

Do not risk active accounts just to remove one inquiry.

Instead, review your report, identify anything inaccurate or unauthorized, and dispute those items properly.

Then, going forward, apply smarter.

Use preapproval tools.

Understand bureau pulls.

Avoid random applications.

And protect your clean reports before you start chasing credit cards, business funding, or 0% APR offers.