PNC Business Credit: How People Are Getting $50K+ in Business Funding

Jun 30, 2026

You can potentially get serious business credit from PNC Bank.

And in some data points, business owners have reported getting approved without uploading proof of income.

That is what makes PNC interesting.

We are talking about business credit cards, business lines of credit, and strategies where one banking relationship can turn into multiple funding options.

But let’s be clear from the start.

PNC is not easy.

They are not the “throw in a sloppy application and hope for the best” kind of bank.

They want clean credit.

They want low utilization.

They want low inquiries.

They want a real business profile.

And if you are trying to get the bigger approvals, relationship banking matters.

Quick Answer

PNC may approve business owners for business credit cards and unsecured business lines of credit, with public line-of-credit amounts listed from $10,000 to $100,000. Data points show some applicants getting approved for large PNC business credit lines without uploading income documents, but that usually comes with strong personal credit, low utilization, an established business, revenue, and a banking relationship. Your result may vary based on credit score, inquiries, business revenue, business age, relationship history, product, state, and underwriting.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you are comparing business credit cards with 0% APR offers, my 0% APR Business Credit Card Database can help you research banks, offers, bureau pulls, and approval data points before applying.

Why PNC Business Credit Is Worth Watching

PNC is not always the loudest bank in the business credit space.

But that is exactly why I pay attention to it.

A lot of business owners keep chasing the same banks:

Chase.

Amex.

U.S. Bank.

Bank of America.

Capital One.

Meanwhile, regional and relationship-based banks like PNC can quietly offer strong business credit opportunities if your profile is clean enough.

PNC currently offers business credit cards and unsecured small business lines of credit. Its public unsecured business line of credit page lists line amounts from $10,000 to $100,000 with no collateral required.

That is the kind of funding that can help with:

-

Inventory

-

Cash flow

-

Equipment

-

Payroll timing

-

Marketing

-

Expansion

-

Project expenses

-

Working capital

But the bigger the request, the cleaner the profile needs to be.

PNC Is Not Beginner-Friendly for Everyone

I want to be honest.

PNC can be tough.

This is not the bank I would target if your profile is messy.

If your utilization is high, inquiries are stacked up, recent late payments are showing, or your business financials are weak, PNC may not be the easiest approval.

The data points suggest PNC likes low-risk borrowers.

That means they may care about:

-

Personal credit score

-

Personal credit history

-

Recent inquiries

-

Utilization

-

Business revenue

-

Business age

-

Existing business debt

-

Banking relationship

-

Business checking activity

-

Business credit profile

-

Overall stability

This is not just about having a business.

It is about looking fundable.

PNC Credit Score Expectations

The script data point says PNC looks at Experian FICO 9 for some business credit decisions.

That is interesting because many lenders still use FICO 8 in a lot of consumer-credit contexts.

FICO 9 can treat certain items differently, including medical debt and paid collections.

That can help or hurt depending on your file.

The data point also says PNC generally wants to see a score around 700 to 720 or higher.

I would treat that as a working target, not a guaranteed rule.

For larger approvals, I would want to be stronger than the minimum.

If I were targeting PNC, I would want:

-

720+ if possible

-

Clean recent history

-

Low utilization

-

Few recent inquiries

-

No fresh negatives

-

No messy banking behavior

PNC does not seem like the place to test a borderline profile.

PNC Wants a Clean Recent Credit Profile

PNC appears to be sensitive to recent credit problems.

That means you want the last two years to look clean.

Ideally, no:

-

Late payments

-

Collections

-

Charge-offs

-

Recent bankruptcies

-

Returned payments

-

Maxed-out cards

-

Excessive inquiries

-

Heavy new account activity

This matters because business credit is still risk underwriting.

Even if the product is for your business, the bank may still care heavily about your personal credit behavior.

If your recent history looks unstable, the bank may not want to extend a large business limit.

Utilization Matters a Lot

The script data point says PNC wants to see utilization below 5%, and may prefer something closer to 1%.

That is aggressive.

But it makes sense for a conservative bank.

Low utilization tells the bank:

You are not desperate.

You are not relying heavily on revolving debt.

You are managing credit well.

You have breathing room.

A lot of people think “under 30%” is good enough.

For high-limit business credit, I do not love that mindset.

Under 30% is not the goal.

For stronger approvals, I would rather see utilization under 10%.

For PNC, based on these data points, under 5% may be even better.

PNC May Be Inquiry-Sensitive

The script says PNC can be sensitive to recent inquiries, especially if you have more than two inquiries in the last 90 days.

That matters.

Recent inquiries can make a bank think you are shopping for credit aggressively.

That can look like risk.

If you want to apply with PNC, I would stop applying elsewhere for a while first.

Let the file cool down.

Do not walk into PNC right after an application spree and expect them to love it.

If you want the best shot, make PNC part of the plan before you start applying everywhere else.

Start With a PNC Business Checking Relationship

One of the smartest ways to approach PNC is to build the relationship first.

That means opening a PNC business checking account before asking for credit.

The good news is you may be able to start with a small opening deposit.

Third-party banking reviews currently list PNC Business Checking with a $100 opening deposit.

That makes the first step accessible for a lot of business owners.

You do not need to start with $25,000.

You do not need to walk in like a Fortune 500 company.

But you do need to look serious.

What You May Need to Open PNC Business Checking

Before opening a business checking account, have your documents ready.

Depending on your business structure, you may need:

-

EIN letter from the IRS

-

Articles of Organization or Incorporation

-

Operating Agreement

-

Business address

-

Ownership information

-

Personal ID

-

Social Security number

-

Business license, if applicable

-

Beneficial ownership information

Having these ready makes you look organized.

And with relationship banks, looking organized matters.

You do not want to be fumbling around for basic business documents while asking for serious business credit.

How to Build the Relationship Before Applying

Opening the account is step one.

Using the account is step two.

If you want PNC to view you as a real business relationship, do not leave the account sitting dead.

Use it.

Move money through it.

Pay bills from it.

Run subscriptions through it.

Deposit revenue into it.

You do not need chaotic activity.

You want steady, normal, boring business activity.

That can include:

-

Monthly deposits

-

Vendor payments

-

Software subscriptions

-

Insurance payments

-

Utility payments

-

Business credit card payments

-

Payroll or contractor payments

Boring activity is good.

Boring looks real.

The 90-Day Relationship Strategy

If you want to improve your chances, consider giving the account time.

The script suggests depositing $2,000 to $5,000 and letting it sit for at least 90 days.

That kind of balance seasoning can help show stability.

It may not be required.

It may not guarantee anything.

But it can help your profile look more serious.

A business checking account with a little money and consistent activity looks better than an account opened yesterday with $0 and no transactions.

If you are targeting higher limits, relationship seasoning can matter.

My PNC Relationship Strategy

The script mentioned a simple strategy:

Move at least $1,000 per month into the PNC business checking account.

Shift regular business subscriptions to the account.

Create consistent account activity.

Then apply for PNC business credit later after the relationship has been built.

That is the right idea.

Not rushed.

Not random.

Not “open account today, ask for $100,000 tomorrow.”

Build first.

Apply later.

PNC Business Credit Cards

PNC offers multiple business credit card options.

The script focused on two:

-

PNC Visa Business Credit Card

-

PNC Cash Rewards Visa Signature Business Credit Card

The PNC Visa Business Credit Card was described as having a 0% intro APR for the first 13 billing cycles on purchases and balance transfers, with no annual fee.

The PNC Cash Rewards Visa Signature Business Credit Card was described as offering 1.5% cash back, no annual fee, and a $600 cash bonus.

These exact offers need verification before publishing because card terms change.

But the larger strategy still matters:

PNC has business cards that can fit different goals.

One may be better for low interest or intro APR.

Another may be better for cash back.

Applying for Two PNC Business Cards With One Pull

One of the most interesting PNC strategies is applying for two business cards on the same day.

The script says many people have had success applying for both cards with only one hard pull.

That is powerful if true.

Because if you can get multiple approvals with one inquiry, that can create more available business credit without taking multiple hits.

One data point said:

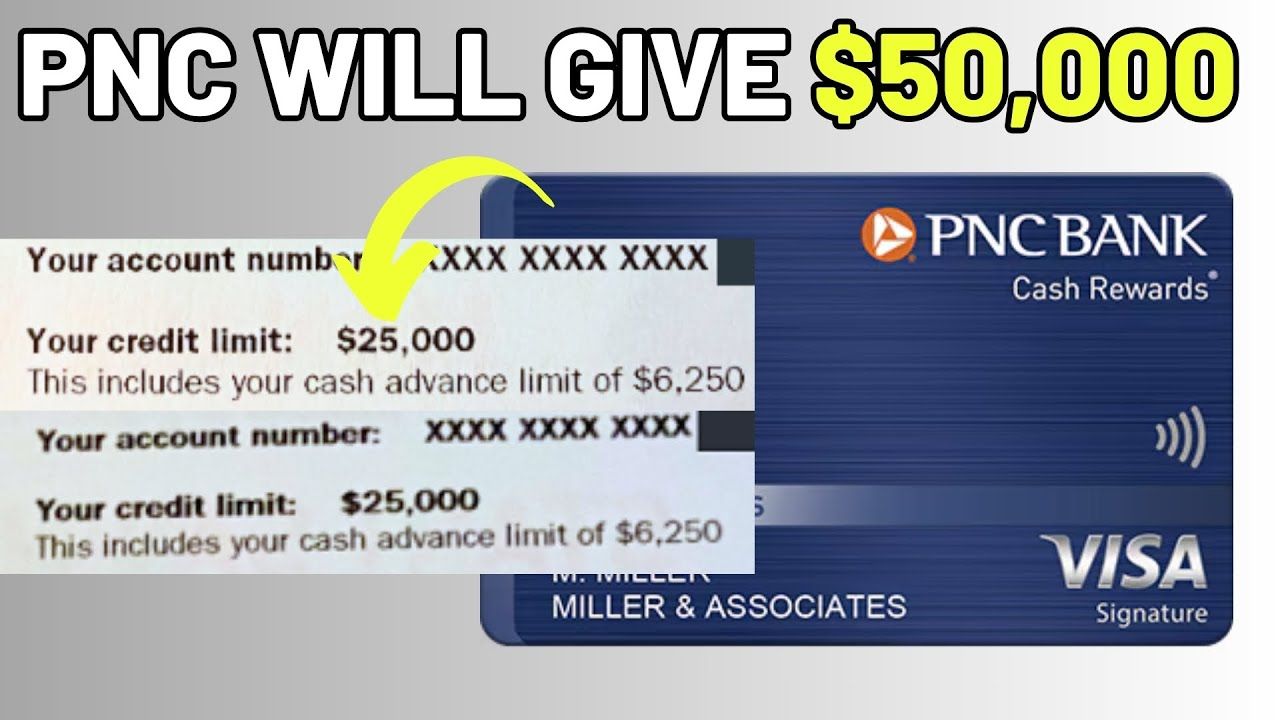

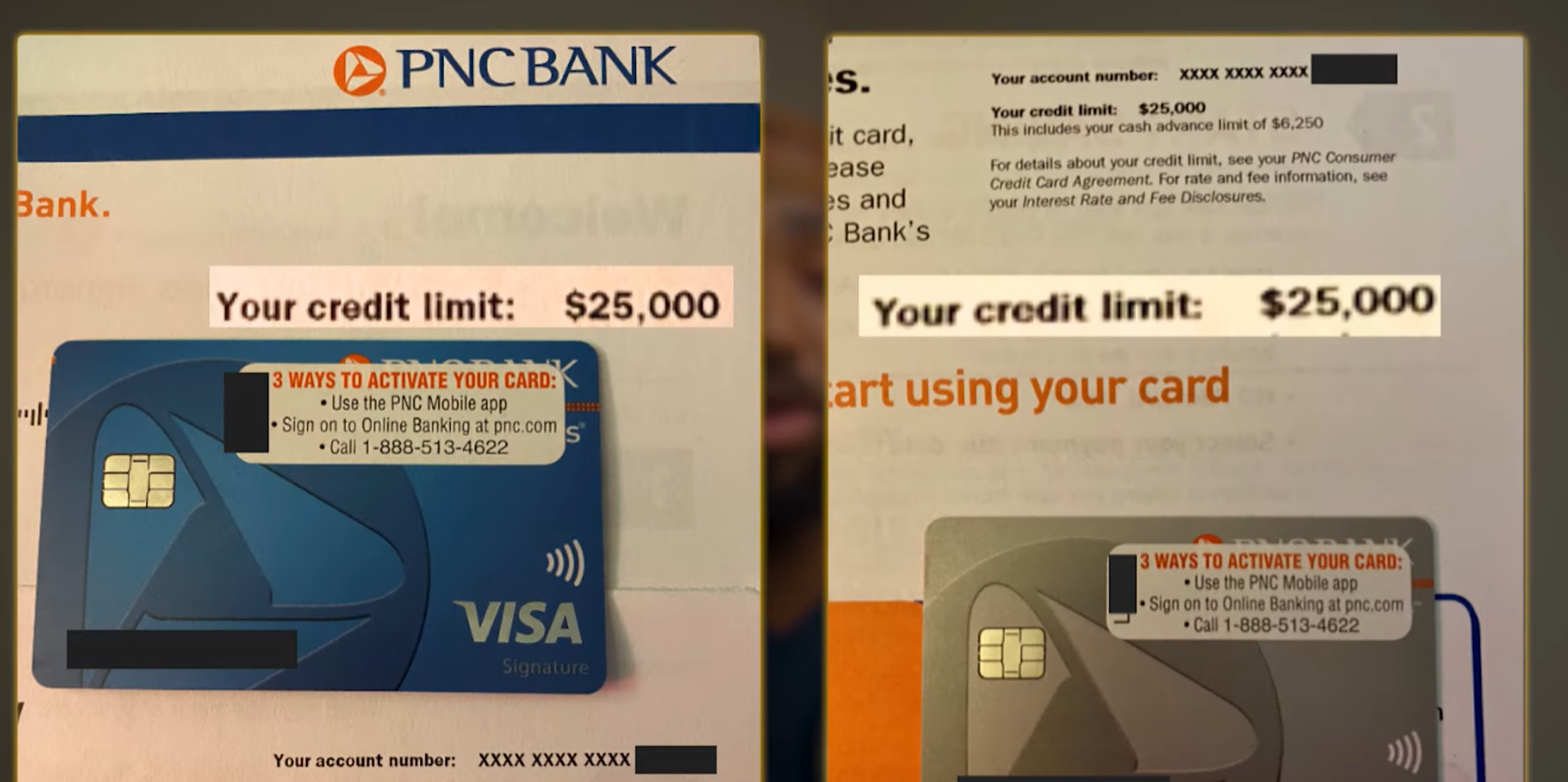

The applicant was approved for two PNC business cards totaling $50,000.

One card was instant.

The other went pending and approved two days later.

Both cards came with identical $25,000 limits.

That is the kind of data point business credit people love.

But do not treat this as guaranteed.

Same-day applications do not always combine pulls.

Banks can change systems.

Manual review can change outcomes.

Always be ready for the possibility of more than one inquiry.

PNC Business Line of Credit

The bigger opportunity may be PNC’s unsecured business line of credit.

PNC’s public page lists unsecured business line amounts from $10,000 to $100,000 with no collateral required.

A business line of credit can be useful because it is flexible.

You can draw when needed, repay, and reuse the available credit.

That can help with:

-

Seasonal cash flow

-

Inventory

-

Short-term projects

-

Payroll timing

-

Equipment needs

-

Vendor payments

-

Emergency working capital

A business credit card is useful.

A business line of credit can be even more flexible.

But it is also harder to qualify for.

Why You May Want Cards First, Line of Credit Second

The script recommends applying for business credit cards before trying for the business line of credit.

I agree with that logic for a lot of profiles.

Business lines of credit are usually harder.

They may require stronger revenue, stronger business history, and cleaner financials.

Business credit cards may be easier to start with.

So a smarter sequence may be:

First, build the PNC checking relationship.

Second, apply for business cards if your profile is ready.

Third, consider the business line of credit once the relationship and revenue support it.

Do not start with the hardest product unless your file is strong enough.

How Much Should You Request?

PNC’s unsecured business line of credit publicly lists amounts up to $100,000.

The script says PNC may counter with a line equal to 10% to 20% of stated business revenue.

That means if you want a larger line, the business revenue needs to support it.

For example:

A business doing $200,000 in revenue may not look the same as a business doing $1 million.

If you request the maximum, be ready for PNC to ask questions.

And if you are aiming for the upper end, be ready for documents.

No-doc approvals may happen in some data points.

But the bigger the request, the more likely a bank may want proof.

No-Doc Does Not Mean No Underwriting

Some PNC data points mention no document uploads.

That is not the same as no underwriting.

PNC can still review:

-

Personal credit

-

Business credit

-

Revenue

-

Business age

-

Existing relationship

-

Account activity

-

Existing debt

-

Prior PNC history

-

Banking behavior

No-doc simply means the applicant was not asked to upload tax returns, bank statements, or financial statements for that approval.

That can happen.

But it is never guaranteed.

If PNC asks for documents, you need to be ready.

Data Point #1: $100K PNC Business Line of Credit and $19K Card

One customer reportedly applied online for a PNC business line of credit.

By Monday, the company was approved for the full $100,000.

They reported:

-

No hard pull on personal credit

-

Nothing reported to personal credit

-

Smooth approval process

-

No documentation required

Then the banker suggested applying for the PNC Cash Rewards Visa Signature business card.

They were also approved for $19,000.

That is a strong combined result.

Why Data Point #1 Worked

This was not a beginner file.

The applicant reportedly had:

-

Personal FICO over 800

-

Business founded in 2013

-

Existing PNC relationship

-

Two existing lines of credit with PNC for different businesses

-

Willingness to open business checking when asked

That explains the approval.

The business had history.

The borrower had excellent credit.

PNC already knew them.

That is a very different situation from a brand-new business walking in cold.

This is why relationship matters.

Data Point #2: $75K PNC Business Line of Credit

Another customer reportedly applied Wednesday evening.

By Friday morning, they had an email and a call from a banker.

They were approved for the exact amount requested:

$75,000.

They reported:

-

No hard inquiry on personal credit

-

A few e-signatures

-

PNC checking relationship

-

Debt-free business aside from one vehicle loan

-

Personal credit score around 828

-

Business score around 97

-

Business revenue around $1.25 million

That is an extremely strong profile.

And the approval makes sense.

High credit scores.

Strong business revenue.

Low debt.

Existing checking relationship.

That is exactly the kind of borrower banks like.

Why Data Point #2 Worked

This approval was not random.

The applicant had four major strengths.

First, they had excellent personal credit.

A score around 828 makes the file look low risk.

Second, they had strong business revenue.

A business doing around $1.25 million annually can support a larger line.

Third, they already had a PNC checking account.

That relationship gave PNC more context.

Fourth, the business had low debt.

Aside from a 2019 Ford Extended Transit Van, they were reportedly debt-free.

That matters.

Low debt means more cash flow available to handle new credit.

What These PNC Data Points Teach Us

These stories are exciting.

But they also show a pattern.

The approvals were not built on luck.

They were built on:

-

Strong personal credit

-

Low debt

-

Established businesses

-

Existing PNC relationships

-

Clean profiles

-

Real revenue

-

Willingness to bank with PNC

-

Organized documentation

-

Conservative underwriting comfort

That is the lesson.

PNC may offer strong funding.

But PNC wants the business to look like a safe bet.

Four Things That Can Help You Get PNC Business Credit

If you want a better shot with PNC, focus on these four things.

1. Lower Personal Utilization

Get your reported utilization down.

For PNC, I would aim under 5% if possible.

Under 10% is good.

Under 5% is better.

2. Let Inquiries Cool Off

Do not apply everywhere right before PNC.

If the data point about two inquiries in 90 days is accurate, PNC may not like recent credit shopping.

Give your profile time to breathe.

3. Build the Banking Relationship

Open business checking.

Use it.

Move money through it.

Let it season.

Do not treat the account like a prop.

Treat it like a real business account.

4. Keep Business Documents Ready

Have your documents organized before applying.

That includes:

-

EIN letter

-

Articles of Organization or Incorporation

-

Operating Agreement

-

Business tax documents, if available

-

Bank statements, if requested

-

Revenue records

-

Business debt details

Even if the approval ends up being no-doc, you still want to be ready.

Who PNC May Be Best For

PNC may be a good fit if you have:

-

Strong personal credit

-

Low utilization

-

Low inquiries

-

Established business revenue

-

A clean business profile

-

A PNC branch or online access path

-

Willingness to build a banking relationship

-

Interest in 0% APR business cards

-

Interest in a business line of credit

PNC is probably not the best first stop for everyone.

But for the right profile, it can be powerful.

Who Should Wait Before Applying

You may want to wait if:

-

Your utilization is high

-

Your personal credit score is below target

-

You have several recent inquiries

-

You have recent negatives

-

Your business revenue is not ready

-

You have no banking relationship

-

Your documents are messy

-

You are applying out of desperation

-

You cannot handle the debt responsibly

The worst time to apply is when your profile is not ready.

Fix the weak spots first.

Then apply.

Frequently Asked Questions

Does PNC offer business credit cards?

Yes. PNC offers business credit cards, including cards focused on low interest, cash back, rewards, and travel. Terms and offers can change, so verify the current card details before applying.

Does PNC offer a business line of credit?

Yes. PNC offers unsecured small business lines of credit, and its public page lists amounts from $10,000 to $100,000 with no collateral required.

Can you get PNC business credit without proof of income?

Some data points show PNC approvals without document uploads or proof of income. But that is not guaranteed. PNC can request financial documents, bank statements, tax returns, or other verification depending on the application.

What credit score do you need for PNC business credit?

The script data point says PNC generally looks for around 700 to 720 or higher, and some successful applicants had scores over 800. For stronger approvals, cleaner credit and lower utilization usually help.

Does PNC pull Experian FICO 9?

The script data point says PNC may pull Experian FICO 9. This needs verification because bureau and score model usage can vary by product, state, and underwriting.

Can you apply for two PNC business cards with one hard pull?

Some data points suggest applicants have received two PNC business card approvals from same-day applications with one hard pull. This is not guaranteed, and applicants should be prepared for the possibility of more than one inquiry.

Conclusion

PNC is not the easiest business credit lender.

But that is exactly why the approvals can be worth paying attention to.

If your profile is clean, your utilization is low, your inquiries are controlled, and your business looks stable, PNC may offer serious business credit opportunities.

The business credit cards can help with 0% APR and rewards.

The unsecured business line of credit can provide flexible working capital.

And the relationship strategy can help you look like more than a random applicant.

But do not rush it.

Open the business checking account.

Use it.

Season the relationship.

Clean up your personal credit.

Organize your documents.

Apply when the file makes sense.

Because with PNC, the goal is not just getting approved.

The goal is walking in like a business owner the bank can actually trust.