Pelican Credit Union $10K Approval: No Income Docs, Real Human Review

Jun 29, 2026

A recent $10,000 Pelican Credit Union credit card approval caught my attention because it looked very different from the way a lot of major banks treat applications right now.

No instant denial.

No long document upload marathon.

No automated “we’ll get back to you” black hole.

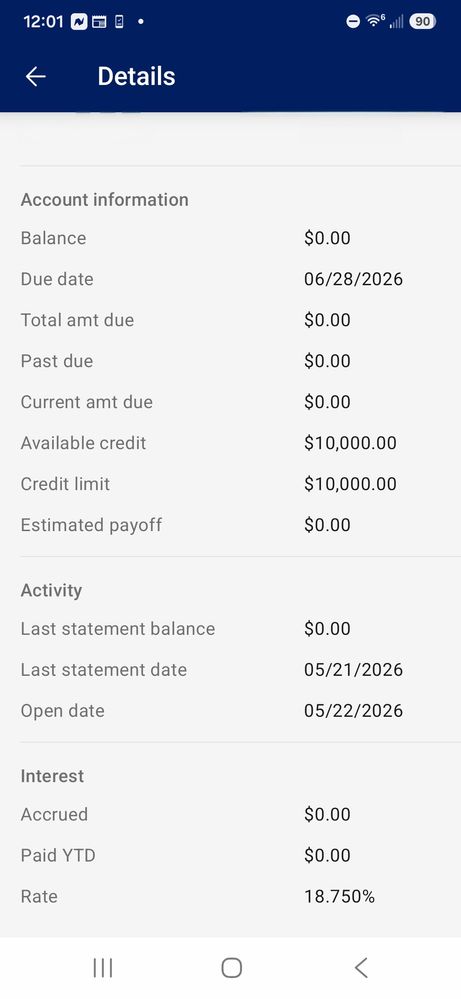

According to the approval data point, the applicant applied for the Pelican Premier Visa early in the morning, received a personal call from a loan officer a couple of hours later, answered a few basic verification questions, and had the new $10,000 credit card showing inside their online account later that same day.

That is exactly why credit unions are still worth studying.

Because while a lot of people keep obsessing over Chase, Amex, Capital One, and Citi, some smaller credit unions are still using a more human underwriting process.

And Pelican Credit Union is one of the names starting to get attention.

Quick Answer

Pelican Credit Union is getting attention because recent forum data points show some applicants getting approved for credit cards with a more personal underwriting process than many major banks. The Pelican Premier Visa Signature card currently advertises travel rewards, Walmart+ reimbursement, TSA PreCheck or Global Entry reimbursement, and limits up to $50,000.

Some users have reported Equifax pulls, out-of-state membership through partner associations, and no ChexSystems pull for membership. But these are user-reported data points, not guaranteed rules, and your result can vary based on your credit profile, state, product, income, and relationship with the credit union.

Why This Pelican Credit Union Approval Stood Out

The approval that caught my attention was for the Pelican Premier Visa.

According to the forum post, the person applied early in the morning. They did not receive an instant approval, but about two hours later, a loan officer personally called them.

That part matters.

Because with many large banks, you usually get one of three things:

-

Instant approval

-

Instant denial

-

A generic pending message

But here, an actual person reached out.

The applicant said the call took less than five minutes. The loan officer only confirmed a few basic items, including:

-

Last four digits of SSN

-

Birthday

-

Address

-

Rent payment

That was basically it.

No massive document request.

No proof of income upload.

No long explanation of recent accounts.

Then by noon, the card was reportedly already showing inside the applicant’s online account.

That is the kind of approval story that makes credit people stop scrolling.

The Credit Profile Was Not Perfect Either

The most interesting part was not just the approval.

It was the profile behind the approval.

According to the data point, the person had around 12 inquiries and had gone on an application spree about two months earlier.

That is not usually what you want to see before applying for another credit card.

A lot of banks are very sensitive to recent credit-seeking behavior. One extra inquiry, one newly opened account, or one recent balance spike can sometimes be enough to push an approval into a denial.

But in this case, the applicant said Pelican did not ask about the recent accounts and did not seem overly inquiry-sensitive.

That does not mean Pelican ignores inquiries.

It does not mean you should go apply with 12 inquiries and expect the same result.

But it does show why credit union data points are worth watching. Some credit unions may look at the full picture differently than the big national banks.

The $5 Membership Workaround

The first question most people will ask is simple:

Can I even join Pelican Credit Union?

That is where this gets more interesting.

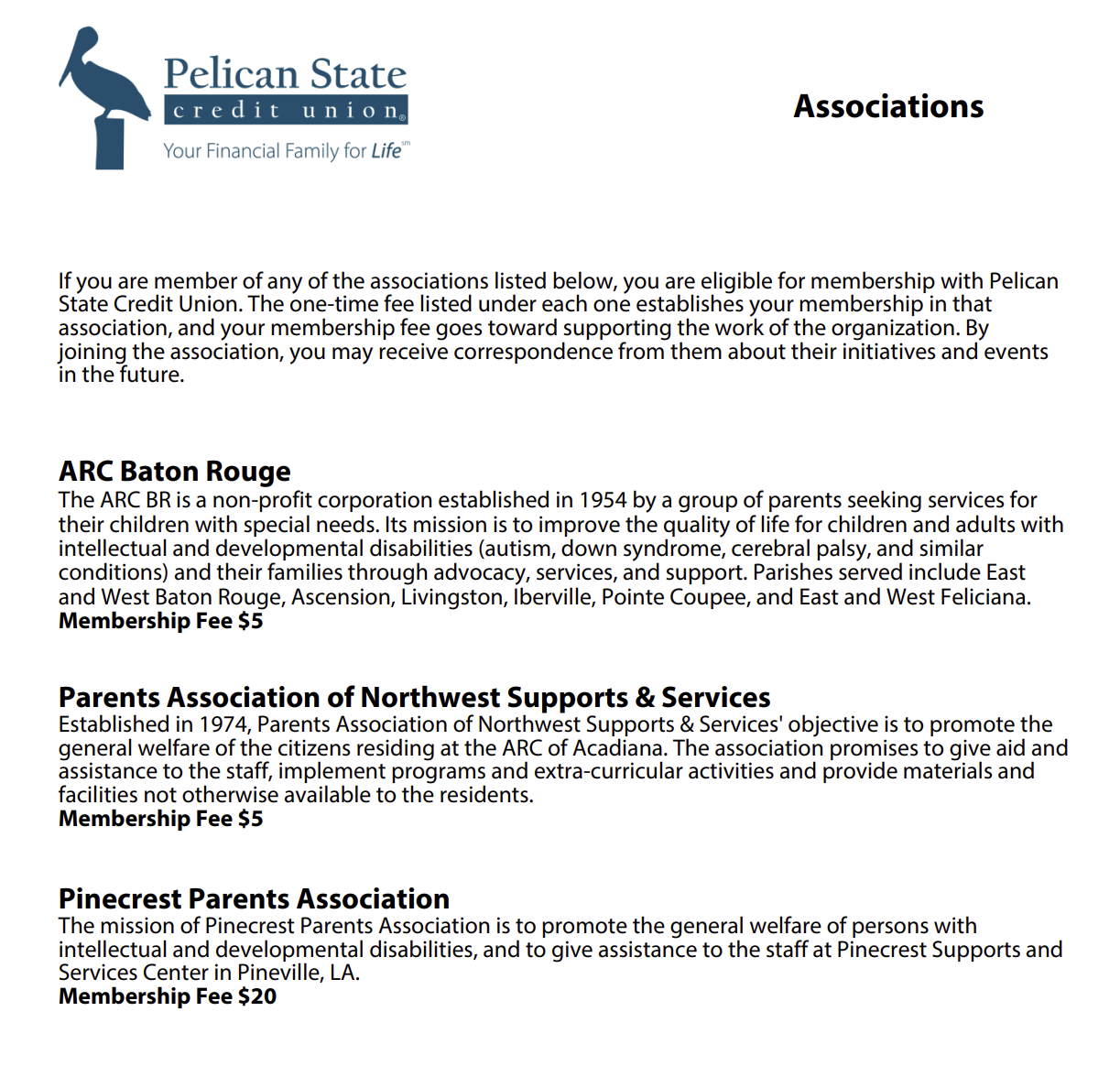

Pelican has partner associations that can help people qualify for membership. One of the listed associations has a one-time membership fee of $5.

That means this is not only for people who live near a branch or work for a specific employer.

Pelican also lists other membership paths, including living in certain Louisiana parishes, working for certain partner employers, being a Pelican employee, or having an immediate family member who qualifies.

But the partner association option is the piece that makes Pelican more interesting for people outside Louisiana.

Helpful resource: If you like finding smaller credit unions that may be open to people outside their local area, my 150+ Credit Unions Anyone Can Join Database can help you research more options like this: https://courses.calbartoncashback.com/CreditUnions

What Credit Bureau Does Pelican Credit Union Pull?

Multiple user reports say Pelican pulls Equifax for credit card applications.

That is important because some people have cleaner credit files on one bureau than another. Your Equifax report may look different from your Experian or TransUnion report, especially if inquiries, balances, or accounts are not reporting the same way across all three.

But do not treat this as a permanent rule.

Credit bureau pulls can vary by state, product, timing, and internal credit union policy. So if Equifax is a major reason you are interested, verify current data points before applying.

Does Pelican Credit Union Pull ChexSystems?

Several users have claimed Pelican does not pull ChexSystems for membership.

That will get attention because ChexSystems can be a problem for people who have had banking issues in the past.

But this is another area where you should be careful.

A user-reported “no ChexSystems” data point is useful, but it is not the same thing as an official written policy. Credit unions can change account-opening procedures, identity verification rules, fraud screening tools, and membership requirements at any time.

So I would treat this as a promising data point, not a guarantee.

Why In-House Credit Union Underwriting Matters

One reason Pelican is interesting is that it does not feel like one of those generic outsourced credit union card programs.

You have probably seen those before.

A credit union promotes a card, but the actual underwriting or servicing is tied to a larger third-party issuer or card program. Those cards can feel more standardized and more algorithm-driven.

Pelican’s data points feel different.

When a loan officer calls an applicant directly, asks a few questions, and makes a same-day decision, that feels more like relationship banking.

And that is one of the biggest reasons I still pay attention to smaller credit unions.

Sometimes the answer is not just “credit score too low” or “too many inquiries.”

Sometimes a human underwriter can look at the full profile and make a decision that a giant bank’s automated system might not make.

Pelican’s Credit Card Lineup Is Surprisingly Competitive

Pelican’s credit card lineup is also stronger than most people would expect from a smaller regional credit union.

The Pelican Premier Visa Signature currently advertises:

-

Limits up to $50,000

-

3x points on travel

-

2x points on dining

-

1 point on other purchases

-

30,000-point welcome bonus after meeting the spending requirement

-

Walmart+ reimbursement

-

TSA PreCheck or Global Entry reimbursement

-

Visa Signature benefits

-

$95 annual fee

Pelican also lists no-annual-fee credit cards with limits up to $50,000, including the Pelican Points Visa and Pelican Prime Visa.

That is not what most people picture when they think about a small Louisiana credit union.

And that is the whole point.

Sometimes the most interesting credit card opportunities are not coming from the banks everyone talks about every single day.

The Bankruptcy Approval Data Point

Another Pelican data point that stood out involved a person who said they were approved only about six months after a Chapter 7 bankruptcy discharge.

The bankruptcy was still reporting.

They were still approved.

Now, this does not mean Pelican is an automatic approval after bankruptcy. It also does not mean you should apply right after a discharge and expect the same result.

In fact, another important detail is that this bankruptcy-related data point did involve proof of income being requested.

So the lesson is not “Pelican never asks for income documents.”

The lesson is that some smaller credit unions may still be willing to look at a rebuilding profile instead of treating a past bankruptcy like a permanent rejection stamp.

That matters.

Because a lot of people rebuilding credit after bankruptcy feel like every decent card is off-limits for years.

But credit unions can sometimes be more flexible when the rest of the profile makes sense.

Do Not Rush Into an Application Just Because of One Data Point

I want to be clear.

I am not saying you should go apply for Pelican tomorrow morning.

That is not the takeaway.

The takeaway is that smaller credit unions can have very different underwriting behavior than the major banks.

Before applying anywhere, you should look at:

-

Which bureau they usually pull

-

Whether they are inquiry-sensitive

-

Whether they ask for proof of income

-

Whether membership is open to you

-

Whether they are sensitive to new accounts

-

Whether the card fits your actual goals

-

Whether you can handle another hard inquiry

One good data point is not a strategy.

But a pattern of good data points can help you find banks and credit unions that may fit your profile better.

Helpful resource: Before applying for a new credit card, it may also be worth checking soft-pull options first. My free Credit Card & Loan Pre-Approval Master List can help you find lenders that let you check offers before risking a hard pull when available: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

The Bigger Lesson: Stop Only Looking at Giant Banks

Most people keep applying with the same giant banks over and over again.

Chase.

Amex.

Capital One.

Citi.

Bank of America.

And those banks can be great when your profile fits what they want.

But if your profile does not fit their current underwriting box, it can feel like you are getting rejected by a machine.

That is why I like studying smaller banks and credit unions.

There are hundreds of them across the country. Many have their own membership rules, bureau preferences, risk tolerance, manual review process, and internal underwriting style.

Some will be strict.

Some will be conservative.

Some will ask for every document under the sun.

But others may look at your full credit profile in a way the biggest banks will not.

That is why Pelican is worth paying attention to.

Not because everyone should apply.

But because it is another reminder that the credit world is much bigger than the same five banks everyone talks about online.

Frequently Asked Questions

Does Pelican Credit Union offer high-limit credit cards?

Yes, Pelican currently advertises credit card limits up to $50,000 on several cards, including the Premier Visa Signature, Points Visa, and Prime Visa. Approval and actual credit limit depend on creditworthiness and other underwriting factors.

What credit score do you need for the Pelican Premier Visa?

Pelican’s Premier page says a minimum credit score of 680 is required to be considered for the Premier card. That does not guarantee approval. It only means that 680 is the stated minimum to be considered.

What credit bureau does Pelican Credit Union pull?

User reports commonly mention Equifax for Pelican credit card applications. However, credit bureau pulls can vary, so verify recent data points before applying.

Can you join Pelican Credit Union from out of state?

Pelican lists partner associations as one way to qualify for membership. One listed partner association has a $5 membership fee. That may create a path for people outside Pelican’s local branch footprint, but you should confirm eligibility directly before applying.

Does Pelican Credit Union check ChexSystems?

Some users have reported that Pelican did not pull ChexSystems for membership. That is useful information, but it should not be treated as a guaranteed policy. Account-opening procedures can change.

Does Pelican Credit Union verify income for credit cards?

It depends. One recent approval data point reported no proof of income request, but another bankruptcy-related approval data point did involve proof of income. So you should be prepared for the possibility of income verification.

Conclusion

The Pelican Credit Union approval data point stood out because it showed something many people feel is disappearing from credit card underwriting:

Human judgment.

A loan officer called.

The questions were simple.

The decision was fast.

And the approval happened despite a profile that many larger banks might have picked apart.

That does not make Pelican an automatic approval. It does not mean inquiries do not matter. It does not mean income documents will never be requested.

But it does show why smaller credit unions are worth studying.

Because sometimes the best credit card opportunities are not hiding inside the biggest banks.

Sometimes they are sitting inside a regional credit union most people have never even searched for.