Novo Funding Approval: How I Got $3,300 in Business Funding With No Hard Pull

Jun 29, 2026

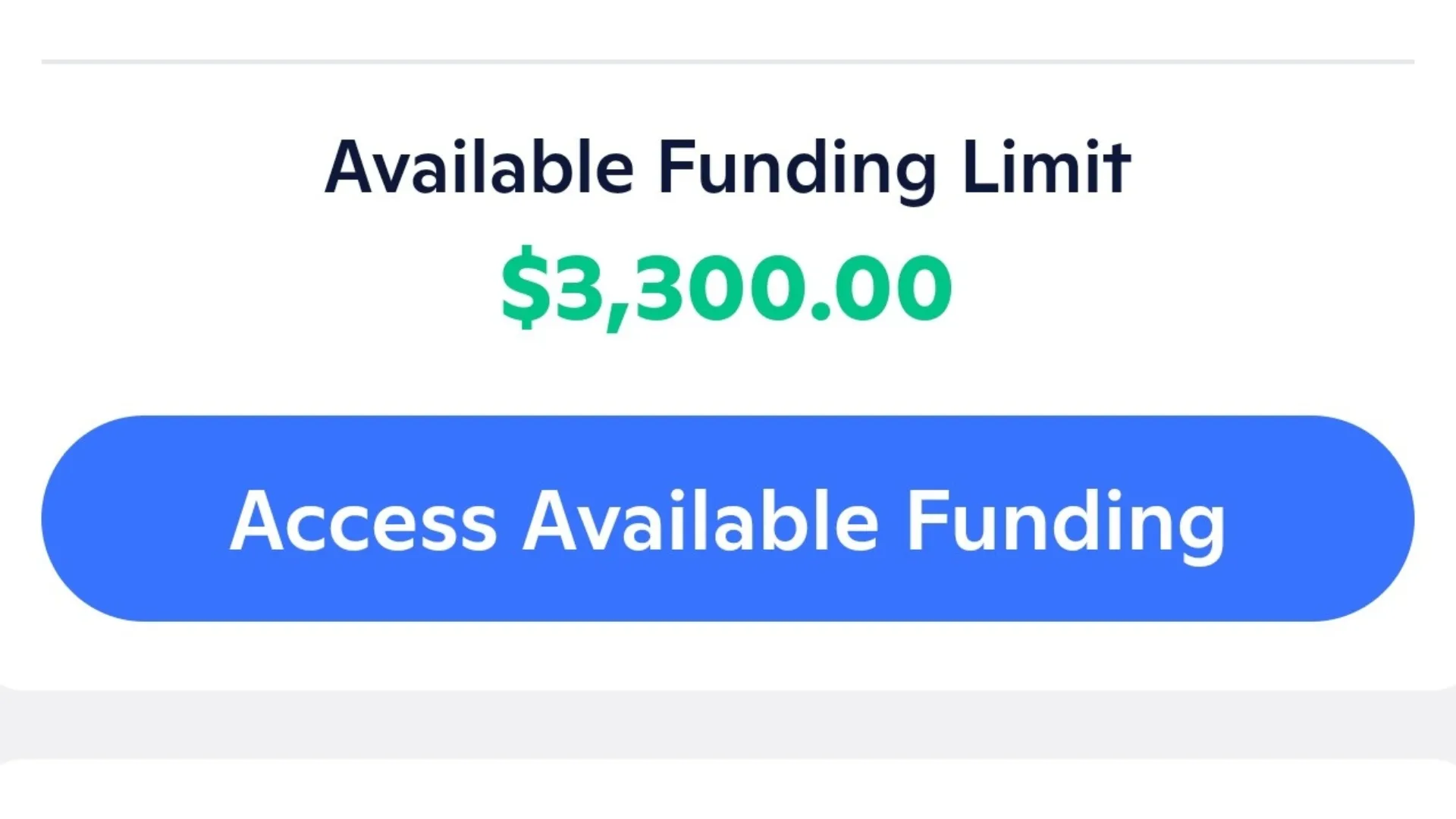

I just got approved for $3,300 in Novo Funding for my business.

No hard credit pull.

No long application.

No tax returns.

No W-2s.

And the money was available as cash that could be used for normal business expenses.

That matters because getting business funding with a newer small business is usually painful. Banks want more time in business, higher revenue, tax returns, stronger business credit, and a clean personal profile. If your business is new or your monthly revenue is still low, most lenders do not exactly roll out the red carpet.

Novo Funding is different.

It is not technically a business line of credit. Novo calls it a merchant cash advance, or MCA. But the way it works feels a lot like a line-of-credit-style funding option because you can access funds, repay over time, and potentially use available funding again.

That does not mean it is perfect. There are some serious details you need to understand before using it.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I was approved for $3,300 in Novo Funding after making three deposits of at least $2,000 into my Novo business checking account over about four months. Novo Funding uses a soft credit check, so my personal credit score was not hit with a hard inquiry. Novo says Funding is a merchant cash advance repaid over six months with a flat Monthly Rate, not a traditional loan or credit card interest rate. Terms, eligibility, rates, limits, personal guarantee language, and approval timing can vary by business profile. (novo.zendesk.com)

What Is Novo Funding?

Novo Funding is a working capital product available through Novo.

Technically, it is a merchant cash advance. That means Novo is not calling it a normal business loan or traditional business line of credit.

Novo says Funding provides merchant cash advances that give businesses fast, flexible working capital without taking on debt or giving up equity. Once approved, you get a lump sum based on projected business sales and repay it monthly over six months with a flat Monthly Rate.

That is the official definition.

But from a user standpoint, it feels closer to a flexible funding line because you can access cash, repay it, and potentially use available funding again later. Novo also says Funding is designed so business owners can draw what they need from their limit, and Available Funding can replenish after repayment.

That is why I call it “business line-of-credit-style funding.”

Just remember the important part:

It is still an MCA.

And MCA pricing does not work the same way as a normal credit card APR or bank loan APR.

Novo Funding Minimum Requirements

The original data point I reviewed listed these as the rough minimum requirements:

-

600 FICO score

-

Up to six months of banking history with Novo

-

$500 to $2,000 per month in business revenue

That is very low compared with most business funding options.

But here is where I need to be careful.

Novo’s current public pages do not clearly confirm all of those exact minimums in one place. Novo’s current Funding page says you may be eligible if you are the primary user of your Novo account and stay active for at least six months. Novo’s FAQ also says Funding is currently invite-only and that you are eligible to get started if you receive a pre-approval.

So I would treat the 600 FICO and $500 to $2,000 revenue figures as data points that need verification before publishing as hard rules.

The safer takeaway is this:

Novo Funding looks like it may be more accessible than many traditional business loans, especially for small businesses already using Novo. But you still need to be pre-approved, and Novo makes the final decision.

How Novo Decides Your Limit and Rate

Novo looks at more than one thing.

According to Novo’s FAQ, your Total Funding Limit and Monthly Rate can be based on your credit, revenue, business type, and other factors powered by Novo’s internal algorithms. Novo also says your Available Funding Limit and Monthly Rate can change over time based on economic shifts, credit history, or account activity. (novo.zendesk.com)

That means this is not just about your personal FICO score.

Novo is also looking at the business.

That includes the money coming in, the way your account is used, your business type, and probably whether your cash flow looks stable enough to support repayment.

Novo also encourages linking external business accounts. Their FAQ says connected accounts help them maintain a full picture of your business finances, and linking external accounts often leads to higher funding limits and lower Monthly Rates.

That part is important.

If you barely use Novo and your outside revenue is sitting in another business account, Novo may not see the full picture unless you link those accounts or move deposits into Novo.

How I Got Approved for $3,300

Here is what happened with my approval.

I opened a free Novo business checking account over a year ago under Barton Media LLC.

My business had originally been established in December 2022, but I had to dissolve and reform it in October 2023 after moving from New York to North Carolina. That hurt me from a business funding standpoint because “time in business” is a major factor for many lenders.

Then in January 2024, I decided to test Novo Funding.

The issue was that I had barely used the Novo account.

Even though the account had been open for over a year, it was not my primary business checking account. For months, it sat with a zero-dollar balance. I had almost no real relationship with Novo besides opening the account and initially putting in $100.

Every time I logged in, the Funding button was grayed out.

That meant I was not eligible.

So I started testing deposits.

In January, I deposited $5,000 from another business account.

Nothing happened.

I checked weekly for about two months, and Novo still showed me as ineligible for Funding.

Then I skipped February.

In March, I deposited another $2,000.

Still nothing.

Then in April, I made a third deposit for $3,000.

That is when everything changed.

A few days after that third deposit, I checked the Novo app, and suddenly I was eligible for Funding.

That surprised me because Novo publicly says you need to stay active for at least six months, but my funding eligibility showed up much faster once account activity picked up. (Novo)

My Personal Credit Profile at Approval

Novo told me they would soft-pull my personal credit to finish the application.

That matched Novo’s public FAQ, which says Novo does not check your credit history when you apply for a Novo checking account, but if you apply for Novo Funding, they run a soft credit check that does not impact your credit score.

I use Aura to monitor my credit, and I never received a hard inquiry alert.

My Equifax FICO profile at the time looked like this:

-

FICO score: 796

-

Utilization: 2%

-

Average age of accounts: 6 years, 8 months

-

Revolving accounts: 31

-

Late payments: 0

-

Age of newest account: 2 months

After I accepted the soft-pull step, Novo showed me an approval for $3,300 at a 2.25% Monthly Rate over six months.

I did not need to enter a bunch of new information. I went through the terms, confirmed the details, and the offer was there.

Helpful Resource: Before applying for business funding, it helps to understand whether your business looks fundable from a lender’s perspective. My Business Credit Buildout System is designed to help business owners build their profile and prepare for funding.

Why the Deposit Pattern Mattered

The biggest lesson from my Novo approval is simple:

Novo wanted to see activity.

The account being open for a long time did not seem to be enough.

I had the account for over a year, but the Funding option stayed unavailable while the account was basically dead.

Once I started moving money through the account, the situation changed.

In total, it took:

-

One $5,000 deposit in January

-

One $2,000 deposit in March

-

One $3,000 deposit in April

-

About four months from starting the test

-

Three deposits of at least $2,000

Then I became eligible.

That does not mean everyone can copy this exact pattern and get approved.

Do not take it that far.

But it does show that relationship activity matters. A business checking account with real deposits, active usage, and visible cash flow can look very different from an account that sits empty for months.

Novo Funding Is Not a Normal Business Credit Card

This is where Novo Funding gets interesting.

With a business credit card, you get a credit limit and use the card for purchases.

With Novo Funding, approved funds can land as cash in your business account.

That is a very different tool.

Cash can be used for things a credit card does not always handle cleanly, like:

-

Payroll

-

Contractors

-

Rent

-

Office leases

-

Equipment deposits

-

Vendor payments

-

Inventory

-

Vehicle down payments

-

Emergency cash flow gaps

Yes, you can sometimes use a business credit card to pay vendors through services that charge a processing fee.

But that adds cost.

Novo Funding gives you actual business cash.

That is the main advantage.

The Rate Needs to Be Read Carefully

My offer showed a 2.25% Monthly Rate over six months.

Novo says the Monthly Rate is your fee, it varies by customer, and some rates start as low as 1.5%. Novo also says each advance is settled over six months, with monthly transfers made up of 1/6 of the principal plus the Monthly Rate.

That is not the same as a credit card APR.

This is important because people love comparing funding products like they are all priced the same way.

They are not.

A credit card APR, a business loan interest rate, a factor rate, and a merchant cash advance Monthly Rate can all calculate cost differently.

So before drawing funds, you need to look at the actual repayment schedule.

Do not just look at the percentage and say, “That sounds cheap” or “That sounds expensive.”

Look at:

-

The amount you are drawing

-

The total amount due

-

The monthly transfer amount

-

The fee

-

Whether paying early reduces the cost

-

Whether the cash solves a real business problem

Novo says there is no penalty for early transfers and that you can settle the amount due any time.

That is useful.

But you still need to understand the cost before using the money.

Novo Funding vs. Business Credit Cards

Novo Funding has a few advantages over many business credit cards.

The first one is the soft pull.

Hard inquiries are annoying because you can get denied and still take the credit hit. Novo says Funding uses a soft credit check that does not affect your credit score.

The second advantage is cash access.

A business credit card is great for swiping. Novo Funding can be better when you need money sitting in the account.

The third advantage is that Novo’s underwriting appears to focus heavily on business activity and projected sales, not just personal credit. Novo says your limit and Monthly Rate are based on credit, revenue, business type, and other algorithm-driven factors.

The fourth advantage is that Novo does not currently report Funding activity to Dun & Bradstreet, according to its FAQ. That can be good if you do not want the activity showing up somewhere, but it also means this is not currently a tool for building D&B business credit history.

So this cuts both ways.

Novo Funding may help you access cash.

But it may not help build business credit reporting the way some business credit cards, vendor accounts, or trade lines can.

Helpful Resource: If you are comparing business credit cards instead of cash advances, my 0% APR Business Credit Card Database can help you find cards that may give your business interest-free runway without using MCA-style funding.

The Personal Guarantee Warning

The original approval data point was exciting because no personal guarantee was needed in that situation.

But I do not want you walking away thinking Novo Funding never has personal guarantee language.

Novo’s own FAQ says personal guarantees can apply in some cases. Specifically, Novo says that if the business does not fulfill its obligation after defaulting, the business owner may be held personally liable for the amount due, plus legal or collection costs.

That is a big difference.

So the right way to say this is:

My data point showed a Novo Funding approval where no personal guarantee was needed based on the offer reviewed. But Novo’s current FAQ says personal guarantees can apply in some cases, so every business owner needs to read their own agreement before accepting funds.

Do not skip the agreement.

Do not assume the terms are the same for everyone.

Do not rely on someone else’s approval screenshot as your legal protection.

Helpful resource: If you are comparing business credit options that may not require a personal guarantee, my No PG Business Credit Card Master List can help you research options before applying.

What Happens If You Do Not Have Enough Money in Novo?

This is another detail you need to understand before drawing funds.

Novo says if your Novo checking account does not have enough money to cover your Monthly Minimum Amount Due, the monthly transfer is marked incomplete. Where allowed, Novo may automatically try to transfer the remaining amount from your connected external business accounts, starting with the account that has the highest balance. (novo.zendesk.com)

That matters because connecting accounts is not just about getting a higher limit.

Those accounts may also be used to help collect payments if your Novo account is short, depending on your state and terms.

Novo also says if you are late on a monthly transfer, the remaining amount becomes past due, the account is considered delinquent, you may be charged a late fee, and you cannot access your Available Funding Limit until the past-due amount is reconciled. (novo.zendesk.com)

So yes, this can be flexible.

But it is not free money.

You still need to manage cash flow carefully.

Six Ways Novo Funding Can Beat a Business Credit Card

Novo Funding is not always better than a business credit card.

But in the right situation, it has real advantages.

1. You Get Cash in the Bank

This is the biggest one.

A business credit card gives you purchasing power.

Novo Funding gives you working capital in your account.

That can help when the expense does not accept credit cards or when card payment fees make no sense.

2. It Uses a Soft Credit Check

Novo says Funding uses a soft credit check, so it does not impact your credit score. That is a big deal if you are trying to protect your personal credit before a mortgage, auto loan, business funding round, or credit card strategy. (novo.zendesk.com)

3. It Can Work for Smaller Businesses

Traditional business loans can be brutal for newer businesses.

Novo Funding is built for small businesses already using Novo, and approval is tied to factors like credit, revenue, business type, account activity, and Novo’s algorithms. (novo.zendesk.com)

That does not mean approval is easy.

But it may be more realistic than walking into a traditional bank asking for a business line of credit with a newer LLC and low revenue.

4. You Can Use It for Almost Any Business Purpose

Novo says Funding can be used at the business owner’s discretion for business priorities, including things like equipment, marketing, and delayed payments. (Novo)

That flexibility is helpful.

Credit cards can be limited by where they are accepted.

Cash is cleaner.

5. Early Repayment Can Help

Novo says you can settle your amount due early without a penalty. (novo.zendesk.com)

That gives you more control if cash flow improves.

With any funding product, the faster you can safely clear the obligation, the less stress you put on the business.

6. It Does Not Currently Report to D&B

Novo says it does not report Novo Funding activity to Dun & Bradstreet as of today. (novo.zendesk.com)

That can be good or bad.

Good if you do not want the funding activity visible on business credit reports.

Bad if your goal is to build business credit history.

So do not use Novo Funding thinking it is automatically building your business credit file.

Use it for working capital.

Use other tools for business credit building.

Who Novo Funding Makes Sense For

Novo Funding may make sense if:

-

You already use Novo

-

You have steady business deposits

-

You need short-term working capital

-

You want to avoid a hard credit pull

-

You want cash instead of card purchasing power

-

You can repay over six months

-

You understand the Monthly Rate

-

You read the agreement before accepting

This is especially interesting for newer small businesses that may not qualify for traditional bank lines of credit yet.

But it should still be used carefully.

Short-term working capital can help a business move faster.

It can also create pressure if cash flow is not consistent.

Who Should Skip Novo Funding

Novo Funding may not be the right move if:

-

You do not have steady business revenue

-

You cannot handle six-month repayment

-

You do not understand the Monthly Rate

-

You need long-term financing

-

You want business credit reporting

-

You are already behind on obligations

-

You would use the money to cover a business that is not producing cash

That last one is important.

Funding should solve a business problem.

It should not hide a broken business model.

If you use short-term funding to cover expenses without a plan to generate revenue, you are just buying time.

And time gets expensive.

How I Would Try to Qualify Again

Based on my experience, I would not just open a Novo account and let it sit empty.

That did not work.

If I were trying to qualify again, I would focus on three things.

First, I would keep the account active.

Second, I would move real business deposits through the account.

Third, I would connect external business accounts if they show strong revenue or cash flow.

Novo wants to understand your business.

An empty account does not tell them much.

A business account with deposits, activity, and clean cash flow tells a stronger story.

That does not guarantee approval.

But it gives Novo more data to work with.

Frequently Asked Questions

Is Novo Funding a business line of credit?

Technically, no. Novo calls Funding a merchant cash advance. But it can feel similar to line-of-credit-style funding because you can access working capital, repay it, and potentially use available funding again later.

Does Novo Funding do a hard pull?

Novo says applying for Novo Funding involves a soft credit check that does not impact your credit score. Novo also says it does not check credit history when you apply for the Novo checking account itself.

Does Novo Funding require a personal guarantee?

It can in some cases. Novo’s FAQ says that if the business does not fulfill its obligation after defaulting, the owner may be held personally liable for the amount due, plus legal or collection costs. Always read your own agreement before accepting funds.

Does Novo Funding report to business credit bureaus?

Novo says it does not report Novo Funding activity to Dun & Bradstreet as of today. That means it should not be treated as a business credit-building tradeline unless Novo changes its reporting policy.

How long does Novo Funding take to repay?

Novo says each merchant cash advance is settled over six months. Monthly transfers include 1/6 of the principal plus the Monthly Rate.

Can paying early reduce the cost?

Novo says there is no penalty for early transfers and that you can settle the amount due any time. Before drawing funds, review your repayment schedule so you understand exactly how early repayment affects your cost. (novo.zendesk.com)

Conclusion

Novo Funding is one of the more interesting small business funding options I have tested.

I was approved for $3,300 after moving real deposits through my Novo account, and the application used a soft credit check instead of a hard pull.

That is a big deal.

But you still need to understand what this is.

Novo Funding is a merchant cash advance, not a traditional business line of credit. The Monthly Rate is not the same thing as a credit card APR. Novo does not currently report Funding to Dun & Bradstreet. And while my data point did not require a personal guarantee, Novo’s own FAQ says personal guarantees can apply in some cases.

So use this the right way.

If you already bank with Novo, have clean business deposits, and need short-term working capital, Novo Funding may be worth watching.

But do not draw money just because it is available.

Read the terms. Know the repayment schedule. Understand the cost. And make sure the funding helps your business make more money, not just delay a cash flow problem.