Navy Federal Approved Me for $25,000 After 6 Weeks

Jun 27, 2026

Navy Federal just approved me for a $25,000 credit limit on the More Rewards American Express card.

And I had only been a member for about six weeks.

If you have ever chased high credit limits, you know how rare that can be right out of the gate.

For many people, getting limits like that takes years.

Multiple cards.

Multiple credit line increase requests.

A long history with the bank.

Slowly inching your way up.

But with Navy Federal, the approval came fast.

And it reminded me why so many people in the credit world call Navy Federal the “House of High Limits.”

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I was approved for a $25,000 Navy Federal More Rewards American Express card about six weeks after joining Navy Federal. Before applying, I opened checking and savings accounts, deposited $1,000, added a small recurring direct deposit, and let the relationship sit for a few weeks. Navy Federal pulled TransUnion, the approval was instant, and my credit profile was around a 780 FICO with 3% utilization.

Why Navy Federal Is Called the “House of High Limits”

If you have been around the credit card world long enough, you have probably heard people call Navy Federal the “House of High Limits.”

That nickname exists for a reason.

For years, people have reported getting approved for high starting limits with Navy Federal.

Not just $2,000 or $5,000.

I am talking about reported approvals like:

-

$25,000

-

$30,000

-

$40,000

-

Even higher limits in some cases

That is very different from what many people see with large national banks.

With big banks, you may get approved, but the starting limit can be underwhelming.

A lot of people start with $2,000, $5,000, or maybe $10,000 if the bank really likes the profile.

Then they spend years asking for increases.

Navy Federal can work differently.

Credit unions often care about relationships.

And when the relationship signals line up with a strong credit profile, the results can be impressive.

Why I Decided to Test Navy Federal Myself

I had heard the Navy Federal high-limit stories for years.

But eventually, I wanted to test it myself.

My father served in the military years ago, which made me eligible for membership.

So I joined Navy Federal and started building the relationship before applying for a credit card.

That part matters.

I did not join and instantly fire off a card application the same day.

I wanted to send a few signals first.

Nothing complicated.

Nothing magical.

Just simple relationship-building steps.

How I Joined Navy Federal

The membership process was smoother than I expected.

I was expecting the typical clunky credit union experience.

Old software.

Slow onboarding.

Confusing navigation.

But honestly, Navy Federal felt more polished than I expected.

The account opening process was easy.

The app and online experience felt closer to a big bank than an old-school credit union.

Once I was in, I opened both a checking account and a savings account.

Then I made an initial $1,000 deposit.

Nothing crazy.

I just wanted money sitting there so the account did not look empty or dormant.

The Relationship Setup Before Applying

After opening the accounts, I added Navy Federal as another direct deposit destination from my business.

I only set it up for $100 per month.

That is not a huge amount.

But it showed activity.

It showed that I was not just opening an account to immediately grab a credit card and disappear.

I also made a few extra deposits of a couple hundred dollars here and there.

Again, nothing extreme.

Just enough to show that this was a real banking relationship.

That is the point.

You do not always need to move your entire financial life to a credit union.

But giving the relationship some activity can matter.

Six Weeks Later, I Applied

About six weeks after opening the Navy Federal accounts, I decided to apply.

There was no preapproval offer sitting in my dashboard.

No special invitation.

No message saying I was already approved.

Just curiosity.

So I pulled up the application on my computer and went through the process.

The application itself was straightforward.

I submitted it.

And the decision came back instantly.

No review message.

No “we need more time.”

No waiting days for underwriting.

Just an approval screen.

The Moment I Saw the Limit

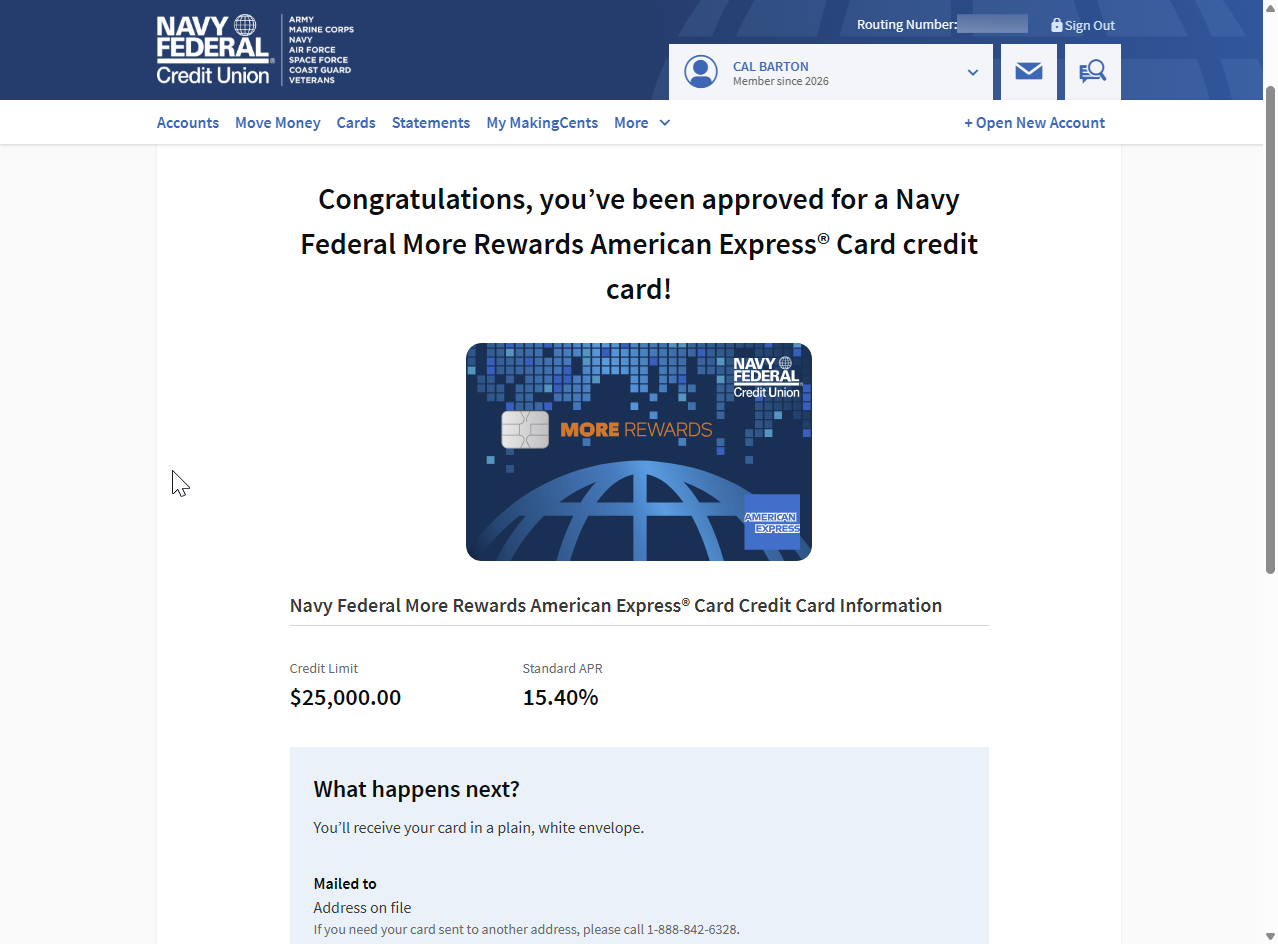

Right there on the screen, I saw it:

$25,000 credit limit.

I leaned back in my chair for a second and just stared at the number.

Then I pumped my fist.

Not going to lie.

That was one of the largest starting credit limits I had ever received.

For a first Navy Federal credit card, after only six weeks of membership, that limit was strong.

Naturally, I took a screenshot.

Then I posted it to my YouTube community page.

The response was wild.

People were excited, and honestly, I was too.

My Navy Federal Approval Data Points

Here is what my profile looked like when I applied:

-

Card: Navy Federal More Rewards American Express

-

Approval: Instant

-

Starting limit: $25,000

-

Bureau pulled: TransUnion

-

TransUnion FICO: Around 780

-

Utilization: Around 3%

-

Recent inquiries: 1 in the last 6 months

-

Average age of accounts: 4 years, 5 months

-

Oldest account: 17 years

-

Total available credit before approval: Around $215,000

-

APR: Around 15%

-

Welcome bonus: $200 value after meeting the spending requirement

That is a strong profile.

So I do not want to pretend the relationship setup did all the work.

My credit profile helped.

A lot.

But I also do not think the relationship signals hurt.

Why I Think the Approval Worked

Looking back, I think a few things probably helped.

First, the relationship signals.

I opened checking and savings.

I deposited $1,000.

I set up a recurring $100 monthly direct deposit.

I made a few extra deposits.

I let the account sit for several weeks before applying.

Those steps told Navy Federal I was not just there for a one-time credit application.

I was becoming a real customer.

Second, the credit profile was clean.

A FICO score around 780, 3% utilization, and a long credit history are exactly the kind of things lenders like to see.

Third, Navy Federal is a credit union.

Credit unions often look at relationships differently than big banks.

They still care about your credit.

They still underwrite.

They still deny people.

But they may weigh relationship factors more heavily than some national banks that feel completely algorithm-driven.

The Auto Refinance Interaction May Have Helped Too

Before applying for the More Rewards card, I briefly applied for an auto refinance through Navy Federal.

The rate did not beat my current loan, so I did not move forward.

But it still created another interaction with Navy Federal’s system.

I was not just opening accounts.

I was exploring more of their products.

Did that directly cause the $25,000 approval?

I cannot prove that.

But I do think it added to the overall relationship picture.

Banks and credit unions pay attention to behavior.

They want to know whether you are a real customer or just chasing one product.

Why the More Rewards Card Made Sense

The Navy Federal More Rewards American Express card is a strong everyday rewards card.

It earns bonus points in categories many people actually use, including:

-

Restaurants

-

Food delivery

-

Supermarkets

-

Gas

-

Transit

That makes it more useful than a card that only works well in rare categories.

It also has no annual fee.

And at the time of my approval, the card came with a $200 value bonus after meeting the spending requirement.

So for me, this was not just about the limit.

The card itself made sense.

A high limit is nice.

But I still want the card to fit my actual spending.

Why Credit Unions Can Be Powerful for High Limits

This approval is a good reminder that credit unions can be powerful if you are chasing higher limits.

Big banks can give high limits too.

But many credit unions are known for being more relationship-focused.

That can work in your favor if you prepare properly.

The mistake people make is applying randomly.

They open an account.

Immediately apply.

Get denied or get a small limit.

Then assume the credit union is overrated.

Sometimes the better move is to slow down.

Open the account.

Fund it.

Use it.

Show activity.

Let the relationship breathe.

Then apply.

That does not guarantee approval.

But it gives you a cleaner setup.

Helpful resource: If you are interested in credit unions beyond Navy Federal, my 150+ Credit Unions Anyone Can Join Database can help you find credit unions that may be open to people outside a narrow local area: https://courses.calbartoncashback.com/CreditUnions

What I Would Do Before Applying to Navy Federal

If you are thinking about applying for a Navy Federal credit card, I would not rush.

Here is the simple setup I would consider:

-

Make sure you are legitimately eligible for membership

-

Open checking and savings

-

Deposit real money into the account

-

Set up some type of recurring deposit if possible

-

Use the account lightly

-

Let the relationship age for a few weeks or longer

-

Lower credit card utilization before applying

-

Check your credit reports

-

Avoid stacking recent inquiries

-

Apply when your profile looks clean

This does not guarantee a $25,000 approval.

But it puts you in a better position.

Do You Need Direct Deposit?

I do not think direct deposit is always required.

But I do think it can help.

Even a small recurring deposit can signal activity.

In my case, I used $100 per month.

That was enough to show Navy Federal the account was alive.

Again, this is not magic.

It is just relationship-building.

If you already plan to use Navy Federal, sending some money there regularly can make sense.

Does Navy Federal Pull TransUnion?

In my case, Navy Federal pulled TransUnion for the More Rewards application.

That matters because bureau pulls can affect your strategy.

If your TransUnion file is cleaner than Experian or Equifax, that could be helpful.

If your TransUnion has recent inquiries or high utilization, you may want to clean it up first.

That said, bureau pulls can vary.

Do not assume every applicant in every state will get the exact same pull.

But for my approval, it was TransUnion.

Why Utilization Probably Mattered

My utilization was around 3% when I applied.

That is important.

Low utilization makes your profile look cleaner.

It tells lenders you are not already maxed out.

It suggests you have credit available and are managing it well.

If your utilization is 30%, 50%, or 70%, you may still get approved somewhere.

But your odds of a high starting limit may be lower.

If you are trying to get a large limit, I would try to get utilization as low as possible before applying.

For many people, under 10% is a strong target.

What I’m Doing Next With Navy Federal

I am not done with Navy Federal.

My plan is to let the card age.

Use it lightly.

Pay it on time.

Keep the balance low.

Then, after about six months, I will likely request a credit limit increase.

After that, I may apply for the Navy Federal Flagship Rewards card.

That card is interesting because it has travel benefits and can reimburse an annual Amazon Prime membership when the terms are met.

So the plan is simple:

Build the relationship.

Use the first card responsibly.

Ask for an increase later.

Then consider the next Navy Federal card when the timing makes sense.

Do Not Apply Just Because I Got Approved

This is important.

My $25,000 approval does not mean everyone will get $25,000.

Your result can vary based on:

-

Credit score

-

Income

-

Debt-to-income ratio

-

Utilization

-

Credit history

-

Recent inquiries

-

Navy Federal relationship

-

Membership profile

-

Internal underwriting

-

Timing

Do not look at one approval and assume the same thing will happen for you.

Use it as a data point.

Not a guarantee.

That is how you avoid getting caught up in approval hype.

Frequently Asked Questions

Is Navy Federal really good for high credit limits?

Navy Federal has a strong reputation for high-limit approvals, which is why many people call it the “House of High Limits.” That does not mean every applicant will get a high limit, but many strong data points exist.

How long should I wait before applying for a Navy Federal credit card?

I waited about six weeks after joining before applying. Some people apply sooner, while others wait longer. If you want to build relationship signals first, giving the account some activity before applying can make sense.

What bureau did Navy Federal pull for your More Rewards approval?

Navy Federal pulled TransUnion for my More Rewards American Express application. Bureau pulls can vary, so check current data points before applying.

What credit score did you have when you got approved?

My TransUnion FICO score was around 780 when I applied.

Did you have a Navy Federal preapproval?

No. I did not have a preapproval offer showing in my dashboard. I applied directly and received an instant approval.

Does opening checking and savings help with Navy Federal approvals?

It may help build the relationship, but it does not guarantee approval. In my case, I opened checking and savings, deposited $1,000, set up a small recurring direct deposit, and let the relationship sit for about six weeks before applying.

Final Thoughts

Navy Federal approved me for a $25,000 More Rewards card after about six weeks of membership.

That is a strong result.

And for me, it confirmed why Navy Federal has the “House of High Limits” reputation.

But I do not think the approval came from one magic trick.

It was the combination of a strong credit profile and basic relationship-building.

Checking and savings.

A $1,000 deposit.

A small recurring direct deposit.

A few extra deposits.

A clean TransUnion report.

Low utilization.

A long credit history.

All of that likely helped.

If you are eligible for Navy Federal and you want to pursue high-limit credit cards, I think it is worth building the relationship intentionally.

Do not just rush in.

Set up the account correctly.

Use it.

Let it breathe.

Then apply when your credit profile is ready.

That is the smarter way to approach credit union approvals.