Klutch Visa Soft Pull Pre-Approval: My $10,000 Offer

Jun 28, 2026

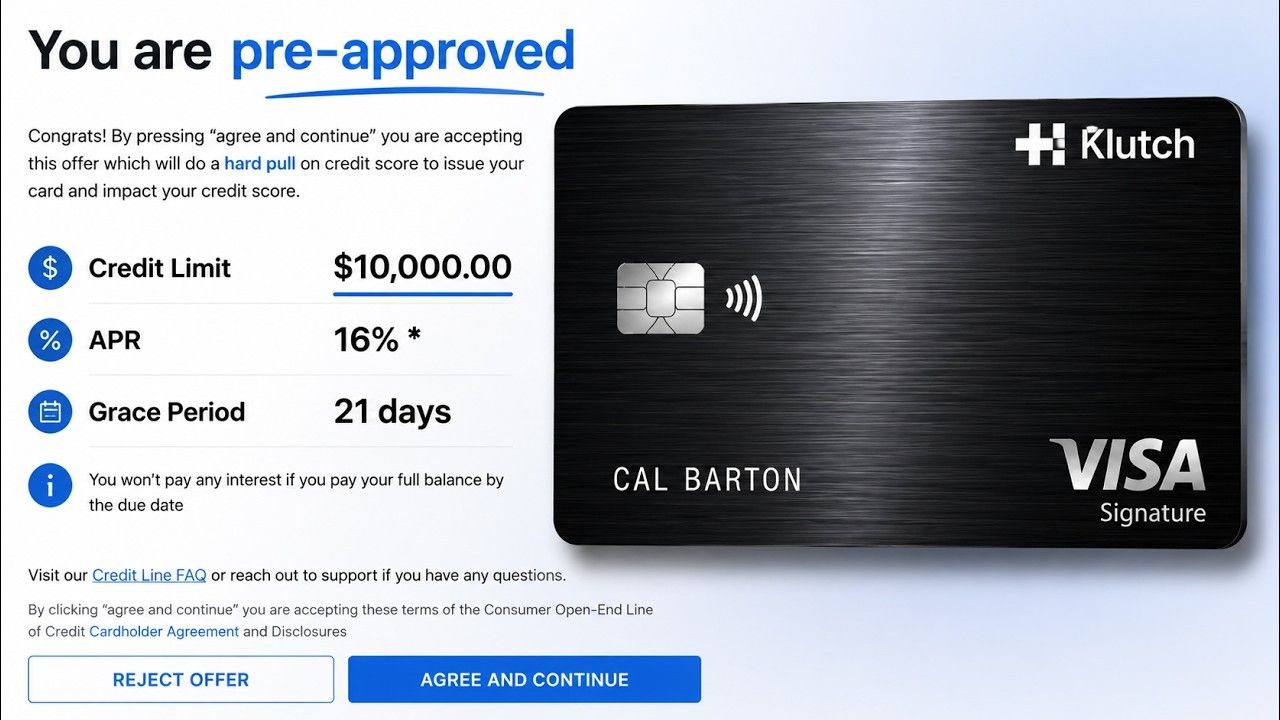

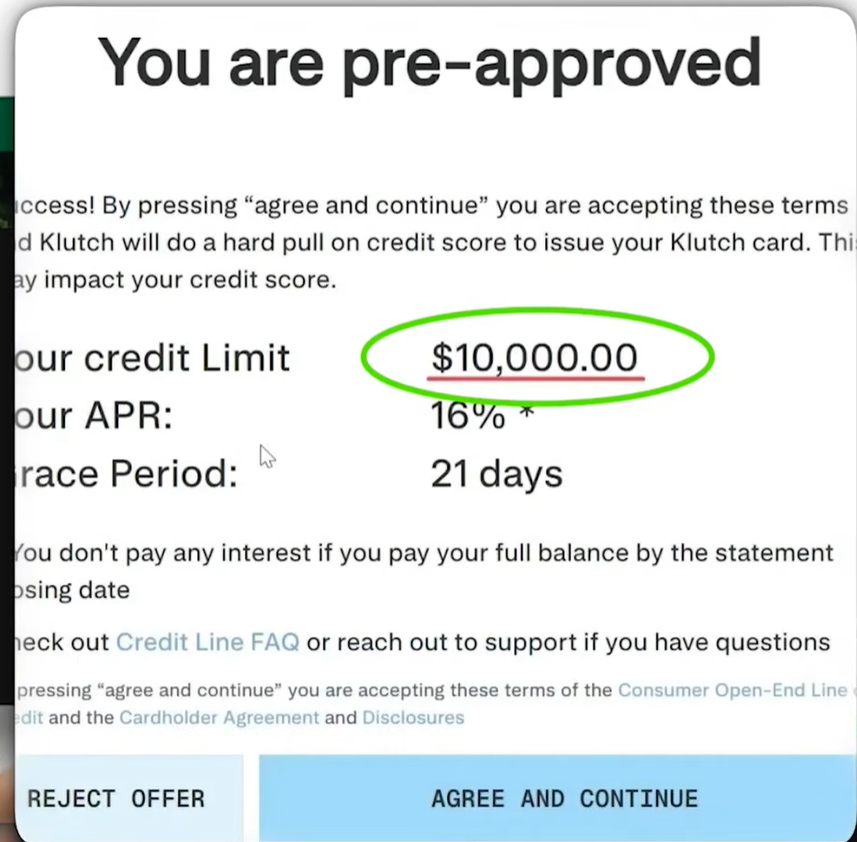

I got pre-approved for a $10,000 Klutch Visa credit card offer with no hard pull upfront.

That is what makes this card interesting.

Not the rewards.

Not the mini-apps.

Not the automation.

The biggest feature is simple: you may be able to see a real credit limit offer before deciding whether to fully move forward.

That matters because most credit card applications feel like a gamble.

You apply.

You take the hard pull.

Then you wait to see whether the bank gives you a strong limit, a tiny limit, or a denial.

Klutch works differently, at least based on my experience. I went through the pre-approval process, verified my identity, waited a couple of hours, and then saw a $10,000 offer sitting inside the app.

Two people from my community have also been approved, including one person who reported a $2,000 starting limit.

So this is definitely one I wanted to break down.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I was pre-approved for a $10,000 Klutch Visa credit card offer with no hard inquiry upfront. The process included identity verification with my driver’s license and a quick face scan, then the offer appeared a couple of hours later inside the Klutch app. Your result may vary, and you should confirm whether accepting the final offer triggers a hard pull before moving forward.

Helpful resource: If you are tired of taking hard pulls just to guess your approval odds, my free Credit Card & Loan Pre-Approval Master List includes cards that may show offers upfront before you fully apply: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

My Klutch Pre-Approval Experience

I applied directly from my phone.

There was no paperwork.

No long document upload process.

No income verification request during the pre-approval process.

Klutch had me verify my identity using my driver’s license and a quick face scan.

That part only took about a minute or two.

After that, my application moved into a pending or under review status.

So this was not an instant approval.

About two hours later, I received a text message saying:

“Congratulations! You're pre-approved for the Klutch Card! Open the Klutch app to get your card today.”

I logged back in.

And there it was.

A $10,000 credit limit offer sitting in my account.

That is the part that stood out.

I was not just seeing vague language like “you may qualify” or “you are invited to apply.”

I was seeing a specific limit offer upfront.

Why Seeing the Limit Upfront Matters

A lot of credit cards make you apply blind.

You might have great credit and still end up with a disappointing starting limit.

Or worse, you take a hard inquiry and get denied.

That is why upfront limit visibility is so valuable.

With Klutch, the main appeal is that you can potentially see what you are being offered before fully committing.

That can help if you are trying to:

-

Build more available credit

-

Lower utilization

-

Add another tradeline

-

Avoid unnecessary hard pulls when possible

-

Compare offers before choosing where to apply

This does not mean everyone will get $10,000.

My offer was $10,000.

One community member reported a $2,000 starting limit.

Your offer could be higher, lower, or you may not be pre-approved at all.

But being able to see the offer upfront gives you more information than a traditional blind application.

Is Klutch a Credit Card or a Charge Card?

This part can get confusing.

Klutch sometimes uses language that feels similar to a charge card.

But Klutch Credit is still revolving credit.

That means:

-

You can receive a stated credit limit

-

You may be able to carry a balance

-

Interest can apply if you do not pay in full

-

Minimum payments can exist

-

Your account behavior matters

My offer showed a $10,000 limit and a 16% rate.

So I would not treat this like a prepaid card or a simple spending app.

It is credit.

If you pay your statement balance in full by the due date, you can avoid interest.

If you carry a balance, it can work more like a normal credit card.

What “Dynamic Spending” Means

Klutch also has something called dynamic spending.

The way I understand it, this means your spending power is not necessarily frozen forever.

Your available spending can be influenced by your account behavior.

That may include things like:

-

How you use the card

-

Whether you pay in full

-

Whether you make payments on time

-

How often you carry balances

-

Your overall account activity

So while my offer showed $10,000, Klutch may continue evaluating the account in the background.

That is not necessarily bad.

It just means you should treat the card carefully.

Paying on time and managing the account well can help you build trust.

Carrying balances, missing payments, or showing risky behavior could cause the system to tighten up.

Klutch Plans: Free, Rewards, and Metal

Klutch has three plan options:

-

Essentials: Free

-

Rewards: $10 per month

-

Metal: $20 per month

You do not need to start with a paid plan just to test the card.

That is important.

For most people, I would start with the free Essentials plan first.

Use the card.

Learn the app.

See whether you actually like the controls, virtual cards, and spending tools.

Then decide later if the rewards or extra features justify paying monthly.

I personally would not rush into paying for rewards unless the math clearly works for your spending.

There are already strong flat-rate cashback cards on the market that do not require a monthly fee.

So for me, the Klutch rewards are secondary.

The main feature is the pre-approval and upfront limit visibility.

Virtual Cards and Spending Controls

Klutch also gives you access to virtual cards.

That means you can create different card numbers for different uses.

For example, you could create separate virtual cards for:

-

Subscriptions

-

Online shopping

-

One-time purchases

-

Specific merchants

-

Specific projects

-

Personal vs. business expenses

That can make spending easier to organize.

It can also help protect your main card number.

If you use one card number for a free trial, another for subscriptions, and another for online purchases, you have more control than you would with one main card number being used everywhere.

This is one of the more practical parts of Klutch.

Even if you do not care about mini-apps, virtual cards can be useful.

What Klutch Mini-Apps Are

Klutch is not just trying to be a basic credit card.

It is trying to be more like a programmable finance platform.

That is where Mini-Apps come in.

Mini-Apps are tools inside the Klutch app that can change how your card behaves.

Instead of only tracking spending after the fact, you can set rules before spending happens.

That can include things like:

-

Blocking certain transactions

-

Setting merchant controls

-

Creating spending limits

-

Managing subscriptions

-

Creating single-use card behavior

-

Automating actions after purchases

-

Organizing spending by category or purpose

This is where Klutch feels different from a normal credit card.

A normal card lets you spend first and review later.

Klutch is trying to let you build rules around the spending before it happens.

Examples of How Mini-Apps Could Help

Here are a few real-world ways someone might use Klutch’s tools.

If you forget to cancel free trials, you could use a card setup that helps control or block future subscription charges.

If you overspend, you could create spending limits that help stop you before you go past your budget.

If you are worried about card fraud, you could use single-use or merchant-specific cards for online purchases.

If you mix business and personal expenses, you could separate spending with different card numbers.

That is the idea.

You are not just relying on memory.

You are setting rules.

For some people, that is powerful.

For others, it may feel like overkill.

How I Would Actually Use Klutch

I want to be honest.

I do not think most people will get this card because of the mini-apps.

I do not think most people will use every automation feature.

I also would not get this card mainly for rewards.

The real reason to look at Klutch is much simpler:

You may be able to see a real limit offer before taking the next step.

That is the feature.

If you are trying to build more available credit, this is useful.

If you are trying to lower utilization, this is useful.

If you want to avoid wasting hard pulls on blind applications, this is useful.

If you want to add another tradeline and see the offer first, this is useful.

The rest is optional.

Who Klutch May Make Sense For

Klutch may make sense if you want a credit card that gives you more visibility before moving forward.

It may also fit if you like virtual cards, spending rules, automation, and app-based controls.

This could be especially interesting for:

-

People who want to see a limit before fully applying

-

People focused on utilization

-

People who like virtual cards

-

People who use subscriptions often

-

People who want more control over online purchases

-

People who enjoy automation and custom rules

-

People who want another revolving tradeline

If you are technical, organized, or someone who likes building workflows, you may actually enjoy the Klutch setup.

Who Should Probably Skip It

Klutch may not be the best fit if you only care about simple rewards.

If all you want is a basic cashback card, there are plenty of simple 2% cards that do not require monthly fees.

You may also want to skip it if you hate app-based banking, do not care about virtual cards, or do not want to think about spending rules.

Some people just want a card they can swipe and forget about.

That is fine.

Klutch is more interesting for people who want control, visibility, and customization.

The Pre-Approval Angle Is the Real Play

The reason Klutch caught my attention is the pre-approval structure.

I am always looking for cards that let people see more information before risking a hard inquiry.

Most credit card applications are still too vague.

You do not know the limit.

You do not know the odds.

You do not know whether the application is worth it.

Klutch gave me a $10,000 offer upfront.

That is why it belongs in the same conversation as other cards that reveal more before approval.

Helpful resource: If you specifically want cards that may reveal your starting limit before you apply, my 9 Credit Cards That Reveal Your Starting Limit Before Approval list is a good place to start: https://offers.calbartoncashback.com/Links

What I Would Check Before Accepting the Offer

Before accepting any Klutch offer, I would check a few things.

First, confirm whether accepting the offer triggers a hard pull.

Second, check the APR.

Third, review the monthly plan options.

Fourth, confirm which features are free and which require a paid plan.

Fifth, understand how the virtual cards work.

Sixth, make sure you know whether the card reports to the credit bureaus.

Seventh, read the terms before using the card heavily.

Do not just focus on the limit.

A $10,000 offer is nice, but the full terms still matter.

Frequently Asked Questions

Does Klutch offer soft-pull pre-approval?

Based on my experience, Klutch showed me a $10,000 pre-approved offer with no hard inquiry upfront. Before accepting the final offer, confirm whether moving forward triggers a hard pull.

Does Klutch show your credit limit before approval?

In my case, yes. I saw a $10,000 credit limit offer inside the Klutch app after the pre-approval process. Other people may see different limits or may not qualify.

Is Klutch a real credit card?

Yes. Klutch Credit is a Visa credit card backed by a revolving line of credit. That means it can work like a normal credit card, including interest if you carry a balance.

What credit limit did I get with Klutch?

My pre-approved Klutch Visa offer showed a $10,000 credit limit. One community member also reported a $2,000 starting limit.

Does Klutch have a free plan?

Yes. Klutch has a free Essentials plan. They also offer paid Rewards and Metal plans.

Should you get Klutch for rewards?

I would not make rewards the main reason to get Klutch. The rewards can be useful for some people, but the stronger reason to look at the card is the soft-pull pre-approval experience and upfront limit visibility.

Final Thoughts

Klutch is one of the more interesting soft-pull pre-approval cards I have tested because it showed me a real $10,000 limit offer before moving forward.

That is the headline.

The mini-apps are interesting.

The virtual cards are useful.

The automation tools could be powerful for the right person.

But for most people, the real value is simple:

You can potentially see what Klutch is willing to offer before fully committing.

That gives you more control.

It reduces guesswork.

And it helps you avoid applying blind.

I would start with the free plan, review the terms, confirm whether accepting the final offer triggers a hard pull, and treat the card like any other revolving credit account.

Use it carefully.

Pay on time.

Avoid carrying unnecessary balances.

And if the upfront offer makes sense for your profile, Klutch may be worth testing.