KeyBank Business Credit Approval: How TJ Got $60K With No Hard Pull

Jun 29, 2026

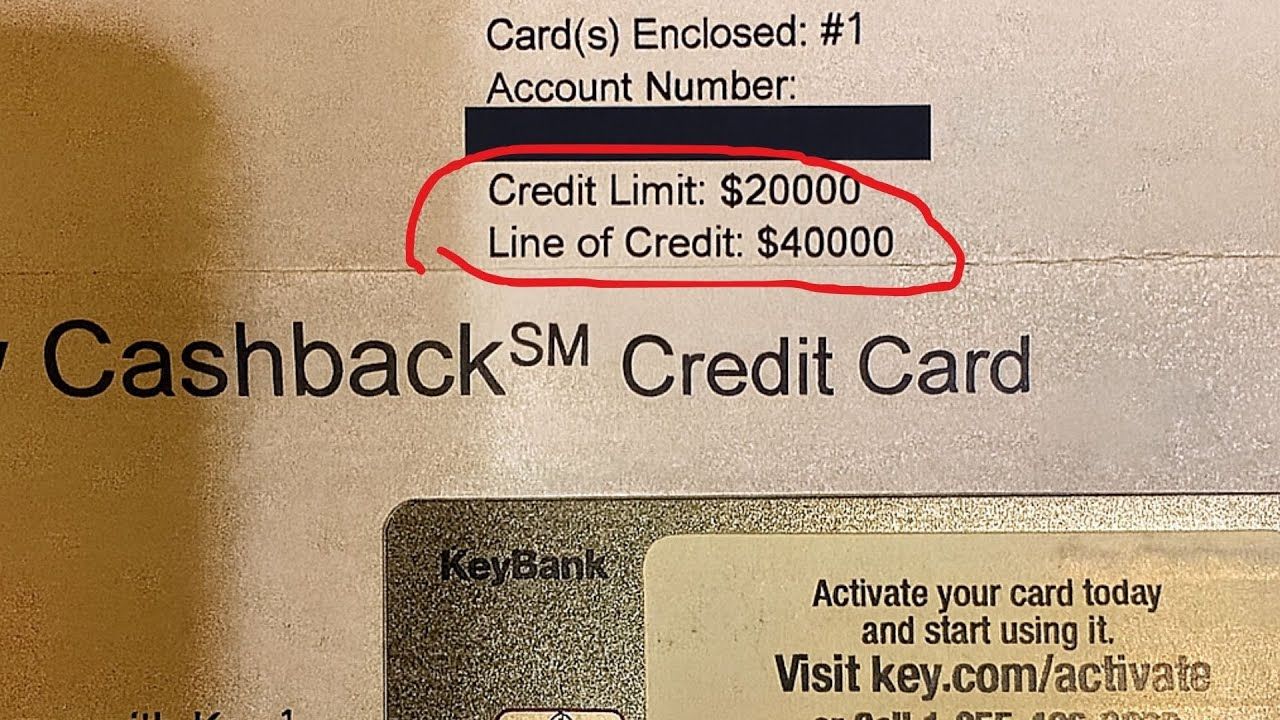

TJ got approved for $60,000 in business credit with KeyBank.

The approval broke down into a $20,000 business credit card and a $40,000 business line of credit.

And according to TJ’s data point, KeyBank did it without a single hard credit pull.

That is the kind of approval that changes how a business owner moves. When a client pays late, a project needs money up front, or you need extra working capital, you are not stuck throwing everything on your personal credit cards.

But this approval did not happen by accident.

TJ walked in with a plan. He had strong personal credit, a business banking relationship, a clean presentation, and a business entity that looked more seasoned than a brand-new LLC.

That combination made a major difference.

Quick Answer

TJ got approved for $60,000 in KeyBank business credit: a $20,000 business credit card and a $40,000 business line of credit. His reported profile included a 780 FICO score, strong personal credit card limits, a recently opened KeyBank checking account, and a two-year-old shelf corporation.

The biggest lesson: KeyBank can be relationship-driven, and business age may matter a lot. But this is one data point, not a guaranteed KeyBank rule. Hard pulls, approvals, documentation requests, credit limits, and personal guarantee requirements can vary by applicant, branch, product, and underwriting.

The KeyBank Approval Data Point

Here is the basic setup from TJ’s approval:

-

Bank: KeyBank

-

State: Ohio

-

Personal credit score: 780 FICO

-

Existing personal card limits: A couple of $20,000+ cards

-

Business setup: Two-year-old shelf corporation

-

Banking relationship: KeyBank checking account opened about one week before applying

-

Deposit amount: $50 minimum deposit

-

Application method: In branch

-

Approval: $20,000 business credit card and $40,000 business line of credit

-

Reported credit impact: No hard pull

KeyBank does offer small-business lines of credit. KeyBank’s current small-business line of credit page lists lines from $10,000 to $500,000, renewable every 12 months, with secured and unsecured options. (Key.com)

KeyBank also offers business credit cards. Its business credit card page says the KeyBank Business Card is designed to help manage cash flow and business expenses, has a $0 annual fee, and uses Mastercard acceptance. (Key.com)

That makes TJ’s approval structure believable: one business credit card plus one business line of credit.

The unusual part is the reported no hard pull.

That is valuable, but do not treat it like a guaranteed rule. KeyBank does not publicly advertise a blanket “no hard pull” approval policy for every business credit card or line of credit applicant.

Why TJ Wanted Business Credit Instead of Personal Credit

TJ needed capital to keep his business running and growing.

A big part of his business involves helping other entrepreneurs with credit repair and adding tradelines to strengthen their profiles. That type of business can require money up front before the revenue comes back in.

And this is where a lot of business owners mess up.

They start putting business expenses on personal credit cards because it feels easy.

At first, it works.

Then one big project hits.

One client pays late.

One invoice gets delayed.

Now your personal utilization jumps, your credit score drops, and your “backup plan” starts turning into a problem.

That is the trap TJ wanted to avoid.

He wanted business-side funding that gave him breathing room without putting extra pressure on his personal credit reports.

That matters because KeyBank’s own business credit card FAQ says KeyBank does not report KeyBank business credit card accounts to personal credit bureaus. (Key.com)

That does not automatically mean there is no personal guarantee. Reporting and personal guarantee are two different things.

But keeping business card activity off your personal credit report can still be a major advantage when you are trying to protect your utilization and personal score.

Why Wells Fargo and U.S. Bank Did Not Give Him What He Wanted

On paper, TJ looked strong.

He had a 780 FICO score.

He had no negatives.

He had strong existing personal credit limits.

He knew credit.

But that did not mean every bank treated him like a premium borrower.

At Wells Fargo, he expected at least a $20,000 line.

They came back with $12,000.

That is not terrible for a lot of people, but based on his profile, it felt low.

Then U.S. Bank was even tighter.

They approved him for only $3,000.

Three thousand dollars.

For a real business owner trying to manage expenses, clients, projects, and growth, that barely moves the needle.

This is why bank selection matters.

A good credit score does not force every bank to give you a high limit. Each bank has its own risk model, relationship rules, internal exposure limits, and underwriting style.

Sometimes the same borrower can look average at one bank and strong at another.

Why the KeyBank Relationship Mattered

Before applying, TJ opened a KeyBank checking account.

He only put in the minimum $50.

That sounds small, but the amount was not the whole point.

The point was relationship.

He was no longer walking in as a total stranger asking for money. He was walking in as a new KeyBank business banking customer.

That does not guarantee approval.

But it can change the conversation.

KeyBank’s lending page says its business wellness advisors work with business owners to help determine the right lending solutions for their needs. (Key.com)

That type of setup is very different from a fast online application where you submit a form and hope the algorithm likes you.

In branch, you can explain the business.

You can answer questions.

You can build trust.

You can come across like a business owner who knows what they are doing.

That is exactly what TJ did.

The Shelf Corporation Move

The move that made this approval more interesting was the entity he used.

TJ did not apply with a brand-new LLC.

He used a two-year-old shelf corporation.

A shelf corporation is a business entity that was formed earlier and has been sitting unused or lightly used. Some business owners buy them because they want the entity to look older on paper.

That can matter because business age is one of the things lenders may pay attention to.

A two-year-old business looks more seasoned than a three-month-old LLC.

That does not mean it automatically gets approved.

It does not mean the bank will ignore revenue, documentation, credit, industry, or risk.

But it can make the application look stronger.

Here is the part people need to hear:

A shelf corporation is not a magic wand.

If the business has no bank history, no activity, no clean records, no tax returns, and no real operations, the bank may still treat it like a risky or unproven business.

And if anything about the entity is messy, it can backfire.

Before using a shelf corporation, you need to check for:

-

Old debts

-

Prior owners

-

Secretary of State records

-

Address mismatches

-

Business name inconsistencies

-

Tax issues

-

Missing ownership documents

-

No operating history

-

No bank activity

-

Any signs the entity was abused before you bought it

The goal is not to fake a business.

The goal is to present a clean, legitimate, fundable business profile.

There is a big difference.

How TJ Presented Himself in the Branch

TJ did not walk into KeyBank winging it.

He practiced.

He knew what he was going to say.

He had his numbers ready.

He had his NAICS code ready.

And he understood that the banker was not just looking at his credit score.

They were looking at him.

That matters.

When you sit across from a banker, your confidence matters. Your answers matter. Your paperwork matters. Your tone matters.

You do not want to sound desperate.

You do not want to over-explain.

You do not want to give numbers that sound made up.

You want to sound like someone who understands their business and can repay what they borrow.

TJ reportedly listed:

-

Personal income: $14,000 per month, or about $168,000 per year

-

Business revenue: $650,000

-

Approximate profit margin: 26%

Those numbers helped paint the picture of a business owner with enough income and revenue to support the requested credit.

But here is the warning:

Do not make up numbers.

Do not inflate revenue.

Do not guess your way through a bank application.

If a lender asks for documents, tax returns, bank statements, or proof of income, your story needs to match the paperwork.

The Approval: $20K Card and $40K Line of Credit

After the in-branch meeting, TJ got the call.

Approved.

The final result was:

$20,000 KeyBank business credit card

$40,000 KeyBank business line of credit

Total approval:

$60,000 in business credit

And according to TJ, there was no hard pull on his credit.

That is the part that makes this data point stand out.

KeyBank’s official line of credit page says its lines of credit are built for things like seasonal cash flow, inventory, and short-term working capital. (Key.com)

That is exactly why a business owner would want this type of funding.

The credit card can help with everyday business expenses.

The line of credit can sit there as a cushion.

You do not have to use it all.

You do not have to max it out.

You just know it is there.

For a business owner, that changes how you sleep at night.

What the Funding Unlocked for His Business

The $20,000 business credit card gave TJ immediate spending power.

He could use it for business bills, client costs, projects, and operating expenses.

The $40,000 line of credit gave him something even more important:

A safety net.

That is the real value of a business line of credit.

It is not just about spending money.

It is about knowing you have access to capital if something goes wrong or an opportunity pops up.

Slow-paying client?

You have options.

Big project requires money up front?

You have options.

Business expenses hit before revenue comes in?

You have options.

That is what business funding is supposed to do.

It gives you flexibility.

The Second Test: Same Person, Different Setup

A few months later, TJ tried the play again.

Same person.

Strong credit.

Same general knowledge.

But this time, he skipped two major steps.

First, he did not open a KeyBank checking account first.

Second, he applied with a brand-new LLC that was only about three to four months old.

The result was completely different.

Instead of a smooth approval, KeyBank started asking for more documents.

Tax returns.

Bank statements from another institution.

A voided check.

Extra proof.

At that point, TJ withdrew the line of credit application and only moved forward with the business credit card.

The approval dropped from a $20,000 card and $40,000 line of credit to just a $5,000 business credit card.

Same person.

Different business setup.

Different result.

That is the lesson.

Business age and banking relationship can change the whole application.

How to Follow the Same Playbook

This does not mean everyone can copy TJ and walk out with $60,000.

That is not how underwriting works.

But there are some clear lessons here.

Step 1: Build the banking relationship first

Do not wait until you need money to introduce yourself to the bank.

Open the business checking account.

Use it.

Let money flow through it.

Keep the account clean.

Even a small account can help start the relationship, but a stronger banking history is better than a $50 deposit and a dream.

TJ’s first application had a KeyBank checking relationship in place.

His second application did not.

The results were not even close.

Step 2: Bring a strong personal credit profile

Even with business credit, your personal credit can still matter.

TJ had a 780 FICO score and strong existing card limits.

That matters because banks like to see that you have already managed credit responsibly.

Before applying, I would want:

-

Low personal utilization

-

No recent late payments

-

No unpaid collections

-

No messy recent credit behavior

-

Existing credit limits that show you can manage larger lines

-

A clean explanation for your business revenue and income

You do not need a perfect profile.

But you do need a profile that makes sense for the amount you are asking for.

Step 3: Know your business numbers

A lot of people walk into banks and freeze.

They do not know their revenue.

They do not know their expenses.

They do not know their margins.

They do not know their business classification.

That makes the banker nervous.

Before applying, know your:

-

Monthly revenue

-

Annual revenue

-

Net income

-

Business expenses

-

Time in business

-

Business purpose

-

NAICS code

-

Use of funds

-

Current bank balances

-

Existing business debt

And again, the numbers need to be real.

Strong numbers help.

Fake numbers can bury you.

Step 4: Apply in branch when the relationship matters

Online applications are easy.

But easy is not always better.

For relationship banks, the branch can matter.

KeyBank’s business credit card FAQ says applicants can compare KeyBank small-business credit cards online and apply by calling or visiting a local branch. (Key.com)

For lines of credit, KeyBank also points business owners toward branch managers and business banking support. (Key.com)

That is why going in person can be powerful.

You get a chance to make the application more than just numbers on a screen.

Step 5: Do not ignore business age

Business age matters.

A brand-new LLC may still get approved for something.

But if you are going after higher limits, bigger lines, or less documentation, an older business can look stronger.

You have two main options:

Build naturally.

Or buy time with a clean shelf corporation.

Most people should probably build naturally unless they know exactly what they are doing.

If you form your LLC now and keep it in good standing, the clock starts. A year or two from now, you may be in a much better position than someone who formed their LLC the night before applying.

Step 6: Ask about the credit pull before applying

This is simple, but most people skip it.

Before applying, ask the banker:

“Will this application be a soft pull or a hard pull on my personal credit?”

Then ask:

“Does that apply to both the business credit card and the line of credit?”

Get clarity before you submit anything.

TJ’s data point was no hard pull, but that does not mean every KeyBank application works the same way.

A Quick Word About No-PG Business Cards

Business credit is powerful, but personal guarantees matter.

A personal guarantee means you may be personally responsible if the business does not pay.

That is why no-PG business cards are so interesting.

They can help separate business activity from your personal credit profile, depending on the card and terms.

But be careful with the way people talk about this online.

No-PG does not mean “free money.”

No-PG does not mean you can ignore business debts.

No-PG does not protect you from fraud, tax issues, legal claims, or other obligations.

It simply means the lender may not require you to personally guarantee that specific credit product.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you want business card options that may not require a hard pull, may not report to personal credit, and may not require a personal guarantee, my No PG Business Card Master List can help you compare options before applying.

The Safer Way to Use This Strategy

The smart version of this play is not “go buy a shelf corp and start guessing numbers.”

That is how people get themselves in trouble.

The smart version looks like this:

Build a real business.

Open the right bank accounts.

Keep clean records.

Let the business age.

Know your numbers.

Use the right NAICS code.

Keep personal credit strong.

Apply with the bank that matches your profile.

And when you sit down with the banker, present yourself like someone who is already operating a real business.

Because that is what banks want to fund.

Not confusion.

Not desperation.

Not a rushed LLC chasing money.

They want clean, organized, believable businesses that look like they can repay.

Helpful Resource: If you want to build the business credit foundation before chasing higher-limit approvals, my Business Credit Buildout System is designed to help business owners build a cleaner profile and prepare for funding.

Suggested internal links to add during publishing: How to Build Business Credit With a New LLC, Business Credit Cards That Don’t Report to Personal Credit, No-PG Business Credit Cards, What to Do Before Applying for Business Funding, and Best Business Checking Accounts for New LLCs.

Frequently Asked Questions

Does KeyBank business credit report to personal credit?

KeyBank says it does not report KeyBank business credit card accounts to personal credit bureaus. That is a major benefit if you are trying to keep business utilization off your personal credit report. (Key.com)

Does KeyBank do a hard pull for business credit?

TJ’s data point says he got a $20,000 KeyBank business credit card and $40,000 business line of credit without a hard pull. But this should not be treated as a guaranteed KeyBank rule. Ask the banker directly before applying because credit pull practices can vary by product, applicant, and underwriting.

What credit score did TJ have?

TJ reportedly had a 780 FICO score. That helped make the application stronger, but a 780 score does not guarantee a high-limit business credit approval.

Do you need a KeyBank checking account before applying?

KeyBank does not publicly say every business credit applicant must open checking first. But in TJ’s case, the checking relationship seemed to matter. His first application had a KeyBank checking account in place and led to $60,000 in approvals. His later application without that relationship led to more documentation requests and a much smaller approval.

Is a shelf corporation required to get business funding?

No. A shelf corporation is not required. It may help in some cases because the business looks older on paper, but it also comes with risks. A naturally aged LLC with real banking activity, clean records, and actual operations is usually the safer long-term path.

What is the difference between a business credit card and a business line of credit?

A business credit card is usually better for everyday purchases and expense tracking. A business line of credit is more flexible working capital that you can borrow from, repay, and use again when needed. KeyBank says its small-business lines of credit can help manage seasonal cash flow, inventory, and short-term working capital needs. (Key.com)

Conclusion

TJ’s KeyBank approval is a strong business funding data point.

He walked in with a 780 FICO score, strong existing credit limits, a KeyBank checking relationship, a prepared presentation, and a two-year-old business entity.

The result was $60,000 in business credit.

A $20,000 business credit card.

A $40,000 business line of credit.

And according to TJ, no hard pull.

But the real lesson is not just “apply at KeyBank.”

The real lesson is that setup matters.

Banking relationship matters.

Business age matters.

Your personal profile matters.

Your presentation matters.

And when TJ skipped two of the biggest pieces later — the KeyBank checking relationship and the aged business entity — the result dropped all the way down to a $5,000 card.

That tells you everything.

Do not walk into a bank hoping your score does all the work.

Build the profile.

Prepare the numbers.

Ask the right questions.

And make sure the business looks fundable before you ask the bank to fund it.