How to Join Navy Federal Without Serving in the Military

Jun 27, 2026

A lot of people assume Navy Federal is completely off-limits unless they personally served in the military.

That is not true.

Yes, Navy Federal is built around the military community.

But you may be eligible even if you never served a day yourself.

That is the part many people miss.

You may qualify through a family member who served, a family member who already banks with Navy Federal, or even someone in your household who is already a member.

And if you are eligible, this matters.

Because Navy Federal is one of the most talked-about credit unions in the credit card world for a reason.

People chase Navy Federal because of the high-limit approval stories, lower APR potential, relationship-based underwriting, and the chance to build a long-term credit union relationship.

But you need to get in the right way.

Do not lie.

Do not buy access.

Do not use fake military relationships.

That can create serious problems later.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

You may be able to join Navy Federal without personally serving in the military if you qualify through an eligible military family member, an immediate family member who is already a Navy Federal member, or someone in your household who is a Navy Federal member. You generally need to open a Membership Savings Account with a $5 minimum balance to establish membership. If you are not legitimately eligible, do not fake your way in because Navy Federal can verify eligibility later.

Why People Want Navy Federal Membership

Navy Federal gets a lot of attention because it behaves differently from many large banks.

It is a not-for-profit credit union.

That structure matters because credit unions are built to serve members instead of outside shareholders.

That does not mean they approve everyone.

And it does not mean they hand out giant limits to every new member.

But Navy Federal has a strong reputation for:

-

High credit limits

-

Lower APR credit cards

-

Relationship-based approvals

-

Strong customer service

-

Credit cards with no annual fee options

-

Useful banking products

-

Credit card prequalification tools

That is why people call Navy Federal the “House of High Limits.”

That nickname did not come from nowhere.

A lot of people have seen Navy Federal approve limits that were much higher than what they were getting from traditional banks.

Why Navy Federal Feels Different From Big Banks

Big banks can feel extremely automated.

You apply.

An algorithm reads your report.

You either get approved, denied, or stuck with a low limit.

Navy Federal still uses underwriting.

They still look at credit.

They still care about risk.

But relationship can matter more with a credit union.

If you build a real relationship, use the accounts, send deposits, and show responsible credit behavior, you may put yourself in a better position over time.

That is why membership is not just about getting access to one card.

It is about building a relationship with a credit union that may become part of your long-term credit strategy.

Navy Federal and Bad Credit Rebuilding

One reason people chase Navy Federal is because it can be more rebuilder-friendly than some major banks.

I have seen people with:

-

Past denials elsewhere

-

Mid-range scores

-

Thin profiles

-

Rebuilding credit files

-

Less-than-perfect history

Still get approved for Navy Federal cards.

Sometimes those approvals become their highest-limit card.

Now, that does not mean Navy Federal is easy.

It does not mean bad credit gets automatic approval.

Fresh late payments, recent charge-offs, high utilization, and unstable credit behavior can still hurt you.

But Navy Federal may be worth studying if your credit is improving and you want to build a relationship with a credit union that may look at more than just one number.

Navy Federal Banking Benefits

Credit cards get most of the attention, but Navy Federal’s banking setup matters too.

Depending on the account, Navy Federal offers checking options, savings accounts, credit cards, auto loans, personal loans, mortgages, and other financial products.

Some checking accounts have no monthly service fee.

Some accounts may offer ATM fee rebates when requirements are met.

And Navy Federal’s credit card APRs are often lower than many big-bank credit cards.

That is one of the reasons people are so interested in getting in.

The credit card limits are exciting.

But the full relationship can matter even more.

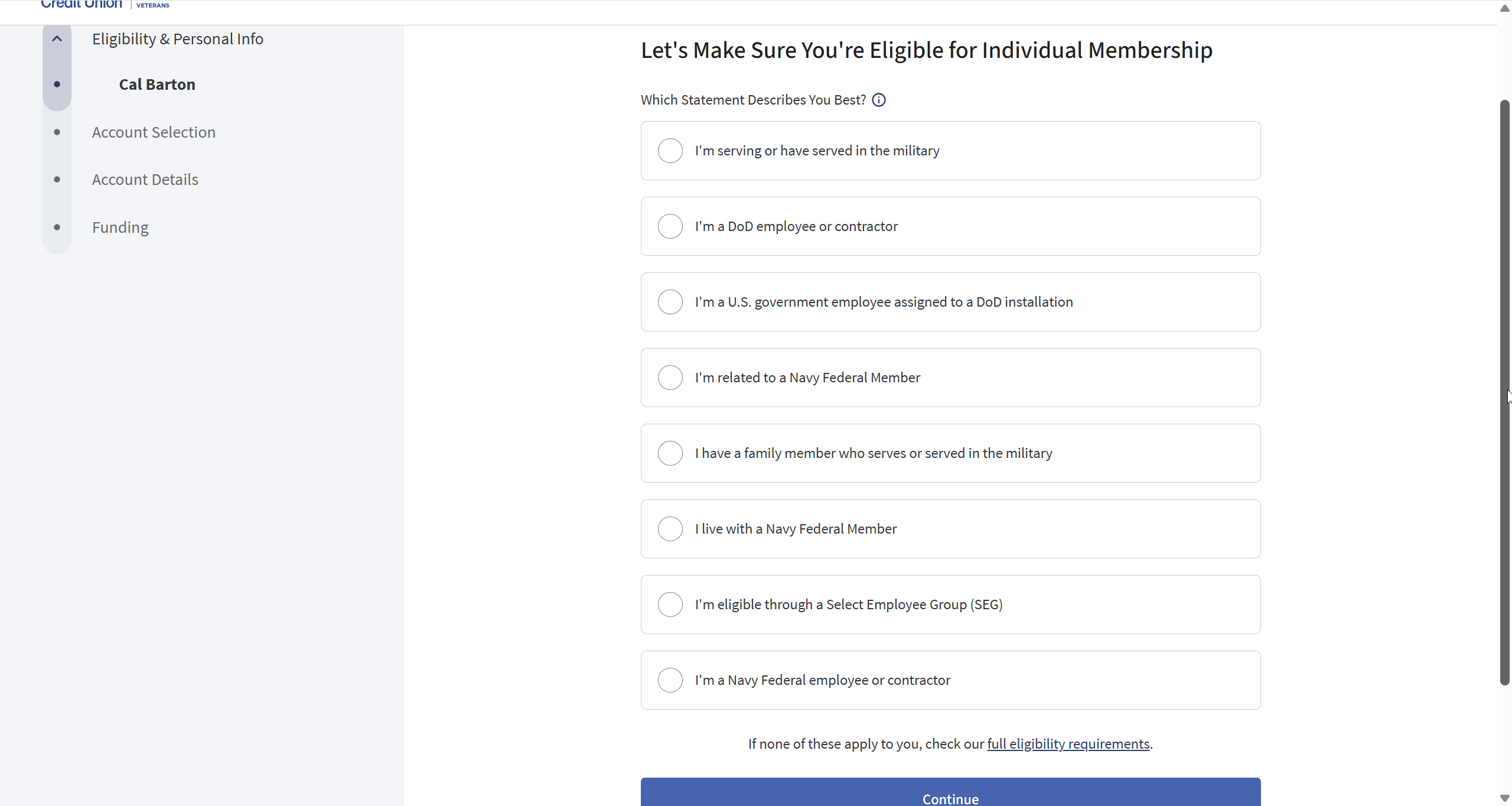

Who Can Join Navy Federal?

Let’s clear up the basic eligibility first.

You may qualify if you are:

-

Active duty military

-

A veteran

-

Retired from the military

-

In the National Guard

-

In the Reserves

-

A Department of Defense civilian employee

-

An eligible family member

-

An eligible household member

That is the part people miss.

You do not always need to be the person who served.

You may qualify because someone connected to you served or is already a member.

Path #1: Immediate Family of Someone Who Served

The first civilian path is through an eligible military family member.

If you have an immediate family member who served or is currently serving, you may be eligible for Navy Federal membership.

This can include relationships like:

-

Parent

-

Grandparent

-

Spouse

-

Sibling

-

Child

-

Grandchild

The important part is this:

The family member does not necessarily need to bank with Navy Federal for you to qualify through their military service.

If they served and the relationship qualifies, that may be enough.

You are not making them responsible for your account.

You are not dragging them into your finances.

You are simply using a legitimate eligibility path based on your family connection.

That is how I got in.

Path #2: Immediate Family of an Existing Navy Federal Member

The second path is through a family member who is already a Navy Federal member.

This is one of the most misunderstood paths.

Someone in your family may have never served personally, but if they are already a Navy Federal member through a legitimate path, that may help extend eligibility to other immediate family members.

This is how Navy Federal membership can spread over time.

One person serves.

Their immediate family becomes eligible.

Then eligible family connections can continue expanding membership access.

That is why you may have civilians all over the country who are legitimate Navy Federal members even though they personally never served.

It all traces back to a valid eligibility connection.

Path #3: Living With a Navy Federal Member

The third path surprises people.

You may qualify if you live in the same household as a Navy Federal member.

That can matter for:

-

Partners

-

Roommates

-

Family friends

-

Other household members

In this case, the key factor is household connection.

Not necessarily blood relation.

If you live with someone who is already a Navy Federal member, you may have a legitimate path to membership.

This is one of those details people often overlook.

How I Joined Navy Federal

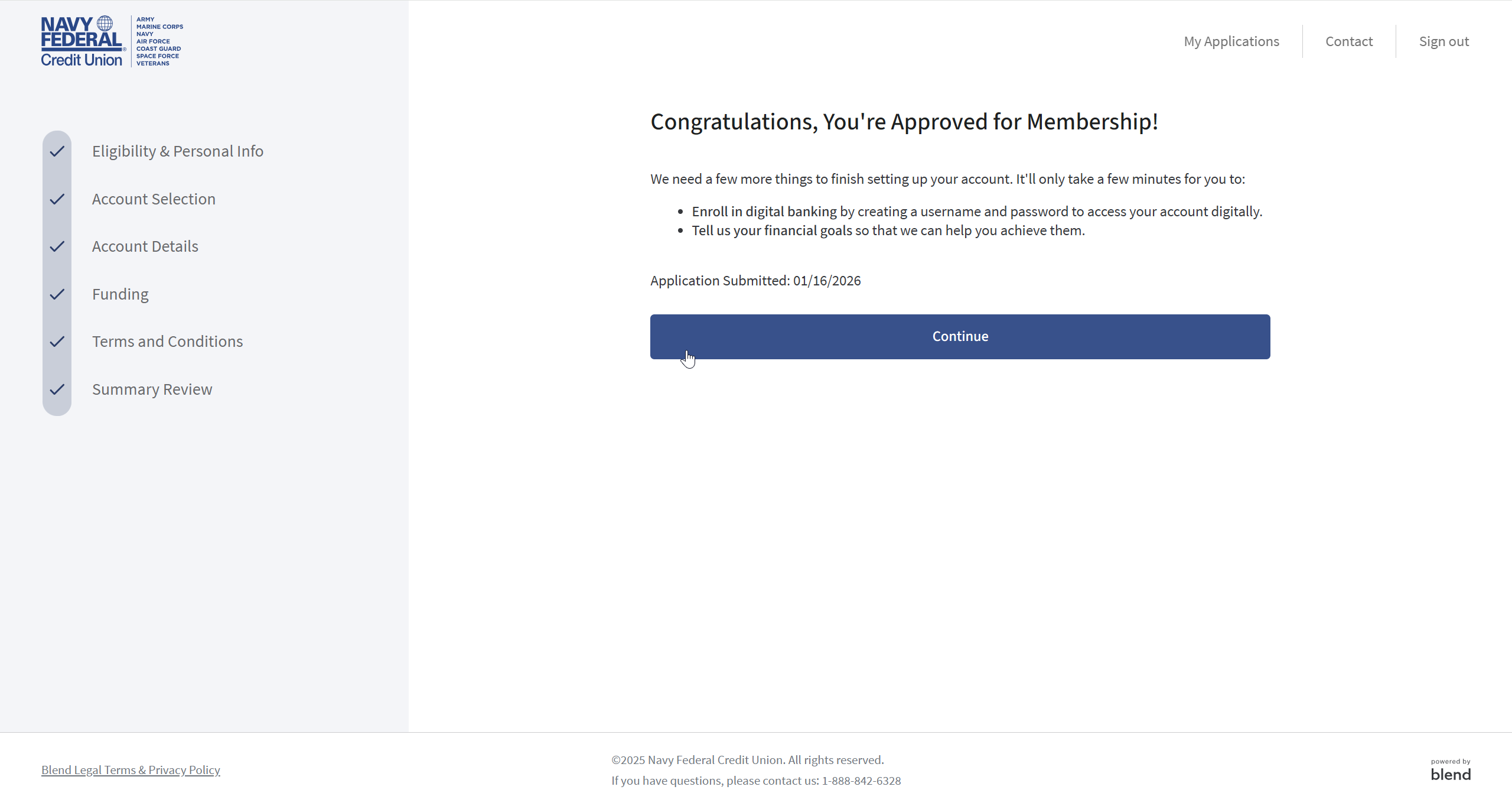

I signed up online.

The entire process took about five minutes.

When I was asked about eligibility, I selected that I had a family member who serves or served in the military.

That was true.

My father and my grandfather both served at different points in their lives.

During the signup process, Navy Federal did not ask me to upload military documents.

They did not stop the application.

They did not require proof during that moment.

The process felt similar to opening an account with a major bank.

But this is the part people need to understand:

Just because Navy Federal does not ask for documents upfront does not mean you are free to lie.

It means they are trusting you to be truthful when you apply.

They can still verify eligibility later if needed.

What You May Need to Apply

If you are eligible, the application process is fairly simple.

You can usually apply:

-

Online

-

Over the phone

-

At a branch

You may need:

-

Social Security number

-

Current home address

-

Driver’s license or government ID

-

A way to fund the account

-

$5 minimum balance for the Membership Savings Account

That $5 matters.

It is not just a random fee.

It establishes your membership savings account and your member relationship with the credit union.

Do You Need to Prove Military Service Upfront?

Not always.

In my case, I was not asked to provide documents during the online signup process.

But you should be ready to prove your eligibility if Navy Federal asks later.

That could mean being able to explain the family relationship or provide documentation if requested.

The safest way to think about it is simple:

Only apply if your eligibility is real.

If you qualify, great.

If you do not, do not force it.

What Not to Do

There is a bad trend online where people encourage others to fake Navy Federal eligibility.

I have seen people talk about:

-

Claiming fake military relatives

-

Using deceased relatives they cannot document

-

Buying or selling Navy Federal access numbers

-

Telling people to “just lie and get in”

-

Using someone else’s membership connection improperly

That is a terrible idea.

Navy Federal membership is valuable, but it is not worth risking account shutdowns, bans, or fraud problems.

If Navy Federal later decides your membership was not legitimate, they may restrict or close accounts.

That can become a much bigger problem than missing out on one credit union.

Do not lie to get in.

Why Fake Eligibility Can Backfire

The risk is not just that your membership gets denied.

The bigger risk is that you get in, build accounts, move money, open credit cards, and then later get reviewed.

If Navy Federal decides the membership was not legitimate, you may have a serious mess on your hands.

That could affect:

-

Checking access

-

Savings access

-

Credit cards

-

Loans

-

Future membership eligibility

-

Funds sitting in the account

That is not worth it.

If you are eligible, join the right way.

If you are not eligible, find another credit union.

There are plenty of strong credit unions that have broader membership paths.

Helpful resource: If you are not eligible for Navy Federal, my 150+ Credit Unions Anyone Can Join Database can help you find other credit unions with broader membership options: https://courses.calbartoncashback.com/CreditUnions

Navy Federal Prequalification

Another reason Navy Federal gets attention is that members can check credit card prequalification without affecting their credit score.

That is useful because applying blindly can get expensive.

If you submit a full credit card application and get denied, you may still take a hard inquiry.

A prequalification tool can help you see which cards you may qualify for before you officially apply.

It is not a guarantee.

But it gives you more information before taking the next step.

Helpful resource: If you want to compare other banks and credit unions that may let you check offers before applying, my Free Credit Card & Loan Pre-Approval Master List can help you avoid unnecessary hard inquiries: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Why Membership Alone Is Not Enough

Getting into Navy Federal is step one.

But membership alone does not guarantee approvals.

If you join, open the $5 savings account, and immediately apply for every card, you may still get denied.

The smarter move is to build the relationship.

That can mean:

-

Opening checking

-

Sending deposits

-

Setting up direct deposit if possible

-

Using the account

-

Keeping your credit utilization low

-

Letting the relationship age

-

Checking prequalification before applying

Navy Federal may be generous, but they still want to see responsible behavior.

What Card Should New Members Consider First?

This depends on your profile.

Some people may start with a rewards card.

Some may start with a lower-APR card like Platinum.

Some may need to start with a secured card if their credit profile is still weak.

The key is not to chase the biggest card first.

The key is to match the card to your current profile.

If you are rebuilding, getting in the door may matter more than getting the flashiest card.

If your credit is stronger, you may have more options.

But either way, do not treat one approval story online as a guarantee.

Your credit profile, income, debt, utilization, recent inquiries, and relationship with Navy Federal all matter.

Frequently Asked Questions

Can you join Navy Federal without being in the military?

Yes. You may be able to join Navy Federal without personally serving if you qualify through an eligible military family member, an existing Navy Federal member in your immediate family, or a Navy Federal member in your household.

Does my family member need to be a Navy Federal member?

If you are qualifying through a family member’s military service, they may not need to be a Navy Federal member. If you are qualifying through an existing Navy Federal member, then that person’s membership is the eligibility connection.

Can roommates qualify for Navy Federal?

Navy Federal includes eligible household members in its membership eligibility. If you live with a Navy Federal member, you may have a legitimate eligibility path.

How much does it cost to join Navy Federal?

Navy Federal requires a Membership Savings Account with a $5 minimum balance to establish and maintain membership.

Does Navy Federal ask for proof of military service?

Navy Federal may not always ask for documents upfront during online signup, but you should only apply if your eligibility is real and you can support it if asked later.

Should I lie to join Navy Federal?

No. Do not lie, buy access, or use fake eligibility. If you are not eligible, look for another credit union with broader membership options.

Final Thoughts

Navy Federal is not only for people who personally served in the military.

You may qualify through an eligible family member, an existing Navy Federal member in your family, or someone in your household who is already a member.

That is the part many people miss.

But the key is doing it the right way.

If you are eligible, Navy Federal can be a powerful credit union relationship.

You can open membership, build banking history, use prequalification tools, and potentially work toward stronger credit card approvals over time.

But if you are not eligible, do not fake it.

There are other strong credit unions out there.

Navy Federal is valuable, but it is not worth risking account closures or a permanent membership problem over a fake eligibility claim.

Join legitimately.

Build the relationship.

Then apply when your profile is ready.