GBank Visa Signature Prequalification: Up to $10,000 Before a Hard Pull?

Jun 27, 2026

I just got prequalified for the GBank Visa Signature card again.

And this time, the offer showed I could start with up to a $10,000 limit before taking a hard pull.

For a smaller bank card, that is higher than you might expect.

But this is also not a normal credit card.

The GBank Visa Signature card is built around a very specific niche: gaming and sports betting spend.

That makes it interesting.

But it also means you need to understand what you are applying for before you get excited about a big potential starting limit.

Because yes, the soft-pull prequalification is useful.

Yes, the limits can be surprisingly strong.

But there are also some reasons I would not treat this as your only or primary credit card.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

The GBank Visa Signature card may let you prequalify with a soft pull and see a potential starting limit before accepting the offer. In my most recent prequalification, the limit did not show clearly on the screen, but the follow-up email showed I was eligible for up to $10,000. If you accept the offer, GBank may then perform a hard pull, with Experian being the bureau most commonly reported in the data points I have seen.

What Is the GBank Visa Signature Card?

The GBank Visa Signature card is a no-annual-fee credit card issued by GBank.

It is different from most credit cards because it is designed around gaming and sports betting transactions.

The card currently offers:

-

1% cash back on gaming and sports app loads

-

2% cash back on eligible net purchases

-

No annual fee

-

A soft-pull prequalification path

That rewards structure is unusual.

Most credit cards either do not want anything to do with gaming transactions or may treat certain gambling-related activity like a cash advance.

GBank is different because gaming and sports app loads are part of the card’s core pitch.

That is why this card has gotten attention from people who want something different from the normal big-bank credit card setup.

Helpful resource: If you want to compare more cards with soft-pull prequalification options, my Free Credit Card & Loan Pre-Approval Master List can help you find banks and cards that may let you check your odds before risking a hard pull: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

My Most Recent GBank Prequalification

I decided to run the GBank prequalification again.

Not because I needed another card.

I wanted to see if anything had changed behind the scenes.

And something definitely changed.

When I went back to the GBank site and clicked into the application, I noticed the promo code field was already filled in.

That stood out because a few months earlier, I had a completely different experience.

Back then, I got blocked because I did not have a promo code.

I had to call in, explain that I had already been prequalified before, and then they manually gave me a code so I could continue.

This time, the field was already filled in.

That tells me the application path may have opened back up again, or at least become easier to access than it was before.

What the Prequalification Asked For

The prequalification process was pretty standard.

I had to enter basic information like:

-

Name

-

Phone number

-

Date of birth

-

Address

-

Social Security number

Then I submitted the form and waited a few seconds.

The result came back as a prequalification.

At that point, the process was still a soft pull.

That means it should not affect your credit score just to check.

But the key is what happens after that.

If you accept the offer and move forward with the full application, that is when the hard pull can happen.

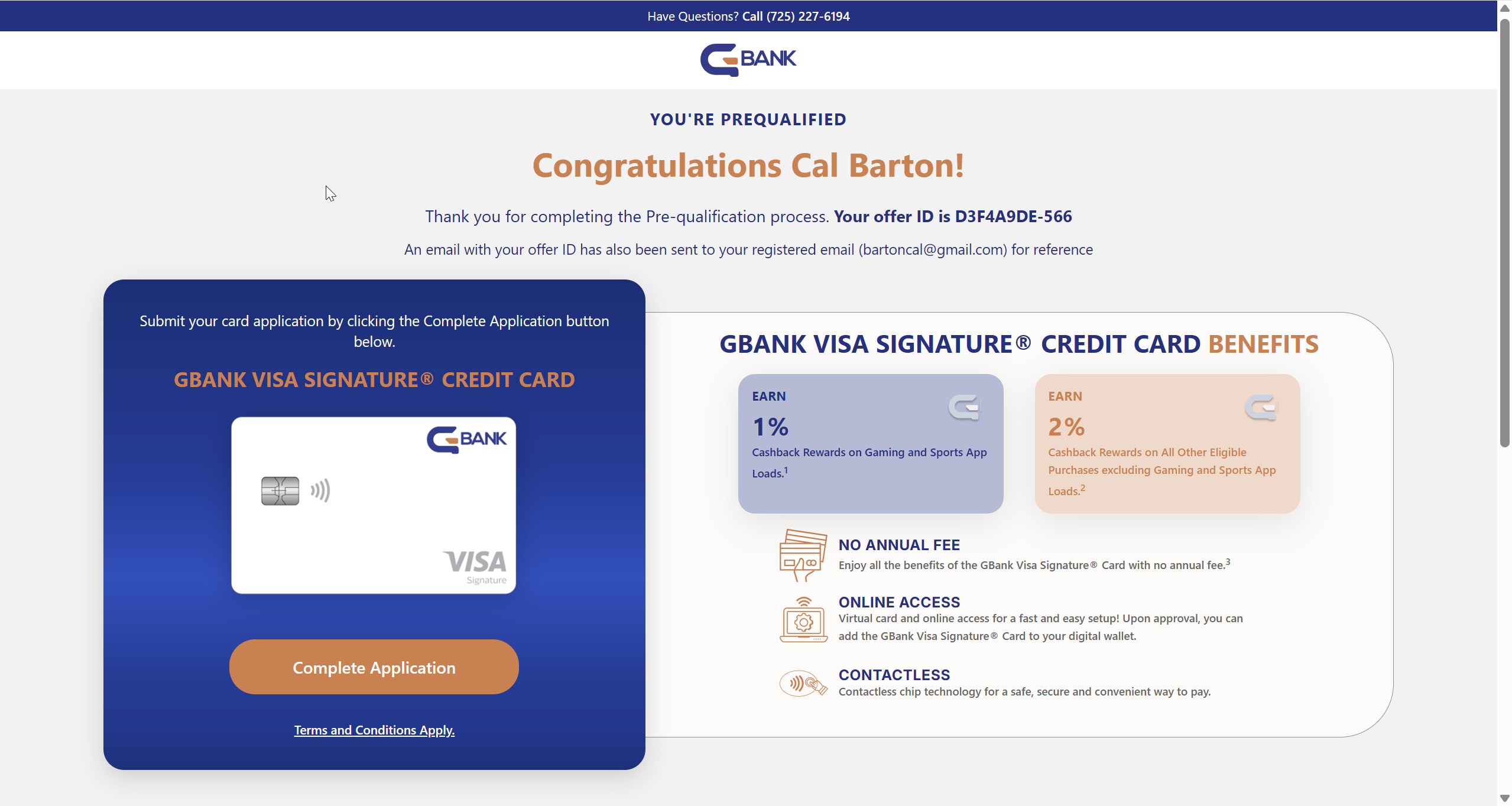

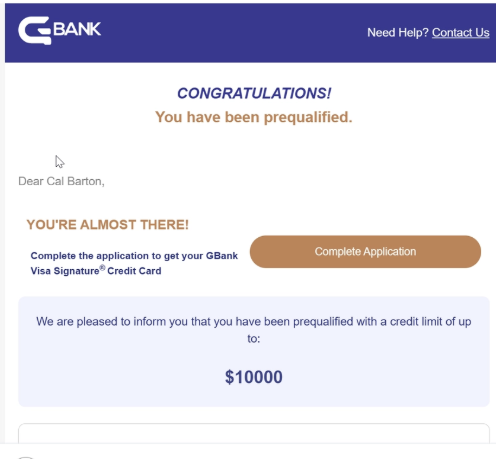

The Weird Part: The Limit Did Not Show Clearly On Screen

Here is where the process got a little strange.

The prequalification screen itself did not clearly show my potential starting limit.

Instead, I received an email shortly after.

Inside that email, it showed I was eligible for up to a $10,000 starting limit.

That is important because a lot of people might run the prequalification, look at the screen, and assume they did not get a useful result.

But in my case, the key information showed up in the email.

So if you test the GBank prequalification, do not only look at the immediate screen.

Check your email too.

That may be where the potential limit appears.

What Bureau Does GBank Pull?

Based on the approval data points I have seen, GBank most commonly appears to hard pull Experian after someone accepts the offer.

That matters because the soft-pull prequalification is only the first step.

The prequalification may let you check the offer without hurting your score.

But accepting the offer can still trigger a hard inquiry.

So before accepting, check your Experian report.

Look at:

-

Recent inquiries

-

Current utilization

-

New accounts

-

Payment history

-

Any freezes or fraud alerts

-

Whether your profile is clean enough to justify the pull

Do not treat soft-pull prequalification as the same thing as final approval.

It is a better starting point than applying blind.

But the final decision still matters.

GBank Approval Data Points I Have Seen

Here is a quick snapshot of the approval data points I have seen around this card:

-

$15,000 approval with an instant decision and no prior relationship

-

$11,300 approval after soft-pull prequalification

-

$9,600 approval after an initial denial tied to identity verification

-

Up to $10,000 prequalification shown by email in my most recent run

Those are not tiny starter limits.

For a smaller bank card, the limits are surprisingly strong.

This is not the type of card where every data point is $500 or $1,000.

Some people are seeing real, usable limits.

That is what makes the card interesting.

The Approval Patterns That Stand Out

A few patterns stand out from the data points.

First, the limits are higher than you would expect from a small bank.

A $10,000, $11,300, or $15,000 limit is meaningful.

Second, the prequalification appears to matter.

From the cases I have seen, people who were prequalified often ended up getting approved.

That does not mean approval is guaranteed.

But it does suggest this is not one of those meaningless “you may qualify” offers that tells you almost nothing.

Third, income documents are not always required.

Some of the approvals appear to happen with basic application data and identity verification.

Fourth, the system is not always instant.

Some people get a quick approval.

Others run into identity verification or delays that can take days or even weeks to resolve.

So the prequalification may look simple, but the back-end process can still be messy.

This Does Not Look Like a Fake Preapproval

Some credit card preapprovals are basically marketing.

They make you feel like you have an offer, but once you apply, the result does not feel connected to the preapproval at all.

GBank does not look like that from the data points I have seen.

There appears to be real underwriting happening during the prequalification process.

The limit may show before the hard pull.

The offer may be meaningful.

And several people who got prequalified appear to have been approved.

That is why I pay attention to cards like this.

Any card that may show you a potential limit before a hard inquiry is worth tracking.

The Big Warning: Do Not Chase Gambling Rewards

This card is connected to gaming and sports app loads, so I need to be clear.

Do not use this card as an excuse to gamble more.

A 1% reward rate does not offset gambling losses.

It does not make betting safer.

It does not make a bad habit profitable.

And it definitely does not mean you should carry a balance.

If you use this card for gaming or sports app loads, the only responsible way to think about it is this:

You were already going to do the transaction.

You can afford it.

You are not chasing losses.

You are not using credit to gamble money you do not have.

And you can pay the balance in full.

If any of that is not true, skip this card.

A credit card connected to betting spend can become dangerous fast if you are not disciplined.

Restrictions After Approval: What Happened Before

There was a period where things got strange with this card.

Some users reported their cards being restricted to only certain transaction types, mainly:

-

Online casinos

-

Horse and dog racing

That meant no normal everyday purchases.

No swiping at regular stores.

No using it like a typical Visa card.

GBank reportedly said the issue was tied to temporary internal updates.

From what I have seen since, that issue appears to have been resolved.

But the fact that it happened at all is worth paying attention to.

That is not normal behavior for a credit card.

And while temporary problems can happen with any issuer, it gives you a glimpse into why I would not rely on this card as my only card.

The Application Process Keeps Changing

Another thing that makes me cautious is how much the process appears to have changed.

At different points, people have seen:

-

Promo code requirements

-

No promo code requirements

-

Possible state restrictions

-

Access opening up

-

Access becoming limited again

-

The application path changing

That kind of back-and-forth usually tells me the bank is still figuring things out internally.

That does not mean the card is bad.

But it does mean you should go in with realistic expectations.

This is not Chase.

This is not Amex.

This is not a giant issuer with a perfectly polished application flow.

It may work.

But it may also require patience if something breaks.

Should You Run the GBank Prequalification?

Honestly, yes, if you understand what you are getting into.

The upside is real.

You may be able to:

-

Check without hurting your score

-

See a potential starting limit

-

Get a surprisingly high limit

-

Add available credit to your profile

-

Avoid applying completely blind

That is useful.

But I would not confuse a high potential starting limit with a card you should rely on for everything.

This is a niche card from a smaller bank with a history of some process changes.

So if you run the prequalification, treat it like a data point.

Not a guaranteed smooth experience.

Who the GBank Card Makes Sense For

The GBank Visa Signature card may make sense if:

-

You want to test a soft-pull credit card opportunity

-

You want a card that may show your limit before approval

-

You are trying to increase total available credit

-

You are okay with a smaller bank

-

You can handle possible follow-up or delays

-

You understand the gaming-related nature of the card

-

You pay in full and do not carry balances

For that type of person, this card is worth watching.

The limit potential alone makes it interesting.

Who Should Be Careful With GBank

I would be careful with this card if:

-

You expect a perfect big-bank experience

-

You do not want surprises after approval

-

You hate calling customer service

-

You need a card you can rely on every day

-

You plan to carry a balance

-

You struggle with gambling or betting

-

You do not want your card connected to gaming-related spending

That last point matters.

Just because a card is interesting from a credit strategy angle does not mean it is right for every person.

The Smart Way to Approach This Card

If I were approaching this card strategically, I would not start by applying.

I would start with the prequalification.

Then I would check:

-

Whether the offer shows a limit

-

Whether the limit appears in the email

-

Whether the APR is acceptable

-

Whether accepting triggers a hard pull

-

Which bureau is most likely to be pulled

-

Whether my Experian report is ready

-

Whether I actually want this card beyond the limit

That last question is important.

Do you want the card?

Or do you just like the number?

A high limit is helpful.

But it is not the only thing that matters.

A Better Way to Think About Prequalification Cards

The best part about cards like this is not just the card itself.

It is the process.

When a card lets you check your odds before a hard pull, you get more information before making a decision.

That is better than applying blind.

A blind application gives you no useful information until after the hard inquiry hits.

A good prequalification tool gives you a better read first.

Again, it is not a guarantee.

But it is a smarter starting point.

Helpful resource: If you specifically want cards that may reveal your starting limit before approval, check out my list of 9 credit cards that reveal your starting limit before approval: https://offers.calbartoncashback.com/Links

Frequently Asked Questions

Does the GBank Visa Signature card have prequalification?

Yes, the GBank Visa Signature card has had a soft-pull prequalification path. In my most recent run, I was prequalified and later received an email showing a potential starting limit of up to $10,000.

Does GBank show your credit limit before approval?

It may. In my case, the limit did not clearly show on the prequalification screen, but the follow-up email showed I was eligible for up to a $10,000 starting limit.

Does GBank do a hard pull?

The prequalification itself is a soft pull, but accepting the offer can trigger a hard pull. Based on the data points I have seen, Experian appears to be the most commonly reported bureau.

What rewards does the GBank Visa Signature card earn?

The card earns 1% cash back on gaming and sports app loads and 2% cash back on eligible net purchases.

Is the GBank Visa Signature card good for everyday spending?

It can be useful because it earns 2% back on eligible net purchases. But because of the card’s niche focus and past process issues, I personally would not rely on it as my only or primary card.

Should I get the GBank card if I gamble or bet on sports?

Only if you are already doing those transactions responsibly, can afford the spending, and pay in full. Do not use credit card rewards as a reason to gamble more or bet money you do not have.

Final Thoughts

The GBank Visa Signature card is one of the more interesting small-bank credit cards I have tested recently.

The soft-pull prequalification is useful.

The potential limits are stronger than expected.

And the fact that my latest prequalification showed up to a $10,000 limit makes it worth paying attention to.

But this card also comes with real caution flags.

The application process has changed multiple times.

Some users previously reported strange restrictions after approval.

The card is built around a gaming and sports betting niche.

And the most important limit information may show up in your email instead of clearly on the screen.

So yes, I think the GBank prequalification is worth checking if you are interested.

But I would not depend on this card as your main credit card.

Treat it as a soft-pull opportunity with upside.

Not as a perfect big-bank card you can blindly rely on.