Further Marketplace Soft Pull Credit Card Offers: What the Data Points Show

Jun 29, 2026

Someone just opened a $15,000 credit card at 10.74% APR without a hard pull.

That alone is enough to get my attention.

But the story gets even better.

The approval came through the Further Marketplace, a credit union marketplace powered by Union Credit that lets consumers check pre-qualified offers from credit unions with a soft pull.

And this is not just one clean approval story.

There are three different lessons here:

One person turned a $1,000 Clearview FCU credit card into $12,500 by refusing to accept a system error as the final answer.

Another person got a $15,000 Clearview FCU Mastercard with no hard pull after accepting a pre-approved offer.

And my own $20,000 Teachers Federal Credit Union pre-qualification went from “congratulations” to denied within about 72 hours.

That contrast is what makes this interesting.

Because Further Marketplace may be powerful.

But it is not magic.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Further Marketplace can show credit union credit card, personal loan, auto loan, and HELOC offers using a soft pull, but a pre-qualified or pre-approved offer is not always the same thing as final approval. In the data points reviewed, one Clearview FCU member had an existing $1,000 card increased to $12,500, another member opened a $15,000 card without a hard inquiry, and my own $20,000 Teachers FCU pre-qualification later stalled with a denial. The key lesson is simple: Further can surface strong credit union offers, but the credit union still controls the final decision.

Helpful resource: If you are tired of taking hard pulls just to guess whether you will be approved, my Free Credit Card & Loan Pre-Approval Master List can help you compare soft-pull pre-approval options before applying.

What Is Further Marketplace?

Further Marketplace is a credit union marketplace.

Instead of applying blindly with one lender, you can check for personalized financing offers from multiple credit unions.

The appeal is obvious:

You may be able to see offers upfront without hurting your credit score.

That is the part people care about.

Nobody wants to take a hard pull just to find out the bank was never serious.

Further gives you a front-end prequalification layer. It checks your profile, shows possible credit union offers, and then sends you into the credit union process if you decide to move forward.

That can include products like:

-

Credit cards

-

Personal loans

-

Auto loans

-

Home equity products

-

Other credit union financing offers

But here is the warning:

The marketplace can show the offer.

The credit union still has to finish the approval.

That difference matters.

Soft Pull Pre-Approval Is Not Always Final Approval

This is where people get too excited.

They see a number on the screen and think the deal is done.

Not always.

With Further, the front-end check may be a soft pull. That means checking the offer does not impact your credit score.

But once you accept an offer, the credit union may still review your membership, identity, eligibility, credit profile, internal rules, and account setup.

In some cases, the approval may finish with no hard inquiry.

In other cases, the credit union may ask for more information.

And in other cases, the offer can fall apart.

That is why you need to treat the offer as strong, but not untouchable.

A pre-approval is a door opening.

It is not always the money in your hand yet.

Data Point #1: $1,000 Clearview Card Turned Into $12,500

The first data point is wild.

This person already had a credit card with Clearview FCU since 2021.

But the limit was only $1,000.

Then inside the Further Marketplace, they found a new pre-approved offer from Clearview showing a much higher amount:

$12,000.

They accepted it.

But the system failed to process the acceptance.

That is where most people would stop.

They would call the credit union, get told to submit a new application, get annoyed, and move on.

But this person did not let it die.

They searched LinkedIn, found the co-founder of Union Credit, and messaged them directly to help locate the right person internally.

That is not normal.

That is persistence.

Union Credit eventually connected them with the correct underwriting contact at Clearview.

After a few short emails and calls over about 10 days, the existing Clearview card was updated to match the higher pre-approved amount.

The result:

$1,000 → $12,500

No hard pull.

Reports frozen.

Same APR.

That is a serious limit unlock.

Why That $12,500 Data Point Matters

The lesson here is not “go DM every fintech founder.”

The lesson is that sometimes the system breaks.

And if the offer was real, you may need the right human to connect the dots.

This person did not try to force an approval they did not qualify for.

They had a pre-approved offer.

They accepted it.

The system failed.

Then they tracked down the right path to get the original offer honored.

That is a big difference.

If you have a real pre-approved offer and something glitches during the handoff, do not assume the first customer service answer is the final answer.

Ask for escalation.

Ask for underwriting.

Ask who handles marketplace offers.

Document everything.

Screenshots matter.

Texts matter.

Emails matter.

If you do not have proof of the offer, it is much harder to fight for it later.

Data Point #2: $15,000 Clearview Approval With No Hard Pull

The second data point is even cleaner.

The same person’s sister also checked the Further Marketplace.

Her credit had been rough years ago because of health issues and no income, but she had since recovered and was reportedly sitting in the 800+ FICO range.

She logged into Further and saw a credit union offer:

Clearview FCU Mastercard — $15,000 limit — 10.74% APR

That is a strong offer.

Important detail:

She had already been a Clearview member since 2020.

That matters.

Credit unions often care about membership and relationship history. Even if the prequalification comes through a marketplace, the credit union still has to match the person to a real membership record.

After she accepted the offer, the credit union called her because they seemed to think she was not already a member.

She gave them the identifying information they needed to locate the membership and verify it was really her.

Shortly after that, the card was opened.

No document requests.

No income verification.

No hard inquiry.

She froze all three credit bureaus after accepting the offer, and the credit union never asked her to unfreeze them.

Then the card showed up in the mail.

That is the kind of data point people are looking for.

Why Existing Credit Union Membership May Help

Both Clearview wins had something in common.

The people already had a relationship with Clearview.

One had a credit card since 2021.

The other had been a member since 2020.

That is important.

A marketplace offer can get you in the door, but an existing credit union relationship may make the final process smoother.

The credit union already knows you exist.

They may already have your identity information.

They may already have your membership record.

They may already have some internal history.

That does not guarantee approval.

But it can reduce friction.

If you see an offer from a credit union where you are already a member, that offer may be more actionable than an offer from a credit union where you still need to open membership from scratch.

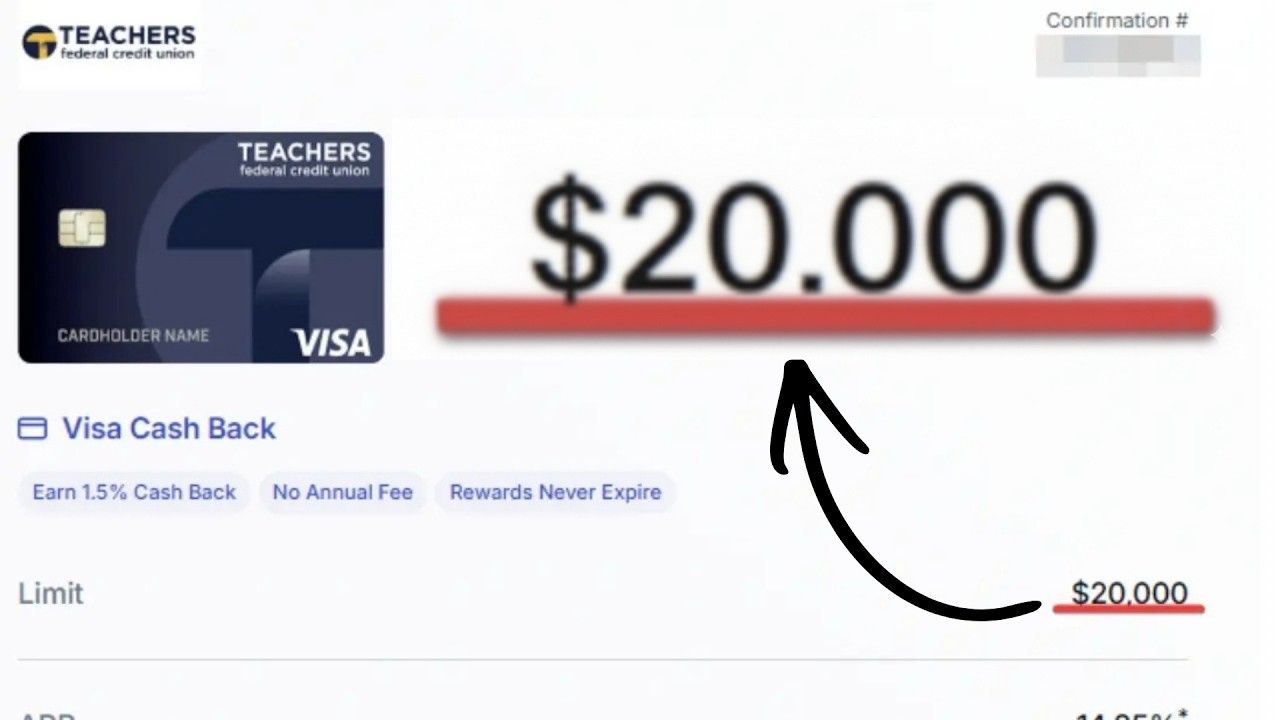

Data Point #3: My $20,000 Teachers FCU Offer Took a Weird Turn

Then I tested Further myself.

Right away, I did not just see one credit card offer.

I saw multiple products from Teachers Federal Credit Union:

-

Credit card

-

Personal loan

-

Auto loan

-

HELOC

The credit card offer specifically showed:

$20,000 limit — 14.85% APR — soft pull

That was enough to make me pay attention.

I even received a text message confirming the limit and APR.

That made it feel much more real than a normal prequalification screen.

Not just “you may qualify.”

More like:

“Here is the exact offer.”

But then things got weird.

My Timeline With Teachers FCU

Here is how it played out.

Tuesday: Pre-Approval

I ran the marketplace check and got the $20,000 Teachers FCU credit card offer.

No hard pull.

Just the prescreen results and a follow-up text confirming the card details.

Wednesday: Phone Call and First DocuSign

I scheduled a call with a relationship sales representative at Teachers FCU.

They actually called on time, which honestly is not always the case with smaller institutions.

We talked through the process, and I asked directly about the credit card.

The rep basically reassured me that I was near the end of the process and things looked good.

After the call, I received a DocuSign to open the membership account.

I also had to upload a copy of my driver’s license.

That was it.

No face scan.

No extra document chase.

They also told me they mainly have branches in New York and are expanding into Florida, but membership is open nationwide.

So me being in North Carolina was not supposed to be an issue.

Thursday: Updated DocuSign

I got another DocuSign updating the paperwork to include both checking and savings.

At this point, everything still looked consistent with the approval path.

Friday: Denial Email

Then came the curveball.

Out of nowhere, I received a credit card denial email.

No hard inquiry.

Just stopped.

So I immediately took action:

-

I emailed my relationship rep at Teachers FCU

-

I messaged a Union Credit founder to try to reach the right internal contact

-

I started treating it like a process issue, not a final emotional defeat

As of the recording timeline, I had not received a final resolution yet.

Why I Do Not Think the Teachers FCU Deal Is Automatically Dead

I do not think this is necessarily over.

It feels more like something broke in the handoff than a traditional decline.

That does not mean it will approve.

It might not.

But this is exactly why these marketplace flows are interesting.

The same system produced:

-

A completed $15,000 approval

-

A $1,000 to $12,500 limit unlock

-

A $20,000 prequalification that stalled after handoff

That tells us more than one perfect success story ever could.

It shows the upside.

It also shows the risk.

The credit union marketplace can surface the offer.

But the final path still depends on the credit union’s internal process, membership setup, identity verification, underwriting, and communication.

Further Marketplace Is a Fintech Front End on a Credit Union Process

This is the best way to understand it.

Further is not replacing the credit union.

It is creating the front-end offer layer.

The marketplace screens you, shows potential offers, and then hands you off to the credit union.

After that, the credit union still matters.

That means you may still deal with:

-

Membership setup

-

DocuSign paperwork

-

ID upload

-

Relationship reps

-

Underwriting teams

-

Internal communication delays

-

Manual review

-

Different departments not being perfectly aligned

So yes, the front end feels like fintech.

But the back end still feels like a credit union.

That is not always bad.

Credit unions can be generous.

But they can also be slow, manual, and inconsistent.

You need to be ready for both.

The Big Warning: Prequalification Can Be a Lead Funnel

Let’s be real.

Marketplace prequalification tools do not exist only to help you.

They also help credit unions find new members.

That does not make them bad.

But you need to understand the incentive.

A marketplace can show attractive offers to get you interested.

Then the credit union gets the chance to bring you into its ecosystem.

That means the goal is not always perfect certainty.

Sometimes the goal is member acquisition.

So you should treat these offers as useful, but not guaranteed.

The screen may say congratulations.

The text may show a limit.

The APR may look locked in.

But until the credit union finalizes the account, you are not done.

The Most Interesting Part: The Limit May Be Honored

One thing I do like about these data points is that when approvals worked, the shown limit appeared to matter.

The $15,000 offer became a $15,000 card.

The $12,000-ish pre-approved offer helped unlock a $12,500 limit.

That is very different from some prequalification tools where you get excited about a number, then final underwriting chops it down.

Now, I am not saying Further will always honor the displayed amount.

Do not turn two data points into a universal rule.

But it is encouraging.

If the shown offer lines up with the final approval, that makes the tool much more useful.

The “No Hard Pull” Angle

This is the part everyone wants to know.

Can you really get fully approved with no hard inquiry?

Based on these data points, yes, it can happen.

But that does not mean it will always happen.

Union Credit’s own FAQ says credit union partners use a soft pull to determine pre-approval eligibility, but if you move forward with a loan application, the credit union may perform a hard pull as part of final approval.

So the safer rule is this:

Checking offers may be soft pull.

Final approval may still vary.

If you are trying to preserve your credit reports, read every screen carefully before submitting.

And if you want to test the frozen-credit-bureau strategy, understand the risk.

Some credit unions may proceed with what they already have.

Others may ask you to unfreeze.

Others may deny.

The Credit Freeze “Hack”

The most interesting tactic from the $15,000 approval data point was the credit freeze.

After accepting the offer, she froze all three credit reports.

The credit union did not ask her to unfreeze them, and the card still opened.

That is not a guaranteed hack.

It is a data point.

The idea is simple:

If the marketplace already completed the soft-pull prescreen and the credit union can process the approval based on that data, a freeze may prevent a hard pull from going through.

But there are risks.

The credit union may require an unfreeze.

The application may stall.

You may get denied.

Or the offer may expire while you are trying to fix it.

So do not treat this like a universal trick.

Treat it like an advanced data-point strategy.

If you try it, take screenshots, read the application language, and be ready for the credit union to ask you to unfreeze.

How to Use Further Marketplace the Smart Way

If you want to test Further, I would not just click everything blindly.

Use a clean process.

Before checking offers:

-

Know your current credit scores

-

Know whether your reports are frozen

-

Check recent inquiries

-

Review your utilization

-

Decide which credit unions you would actually join

-

Make sure your phone and email are current

-

Be ready to screenshot every offer

When an offer appears, capture:

-

Credit union name

-

Product name

-

Limit

-

APR

-

Whether it says soft pull

-

Expiration date

-

Any membership requirement

-

Any application disclosures

-

Any text or email confirmation

If something goes wrong later, screenshots can matter.

Do not rely on memory.

What to Do If the Offer Breaks During Processing

If you accept an offer and the process breaks, do not panic.

And do not immediately start a brand-new application unless you understand the consequences.

Instead:

-

Contact the credit union first

-

Ask for the department that handles marketplace or Union Credit/Further offers

-

Ask whether they can locate the pre-approved offer

-

Provide screenshots if needed

-

Contact Union Credit/Further support if the credit union cannot find it

-

Ask whether a new application would trigger a hard pull

-

Keep everything in writing when possible

The $12,500 Clearview data point happened because the person kept pushing until the right internal contact found the issue.

Most people lose right there.

Not because they were unqualified.

Because they quit too early.

Who Further Marketplace May Be Best For

Further Marketplace may be worth checking if:

-

You want credit union offers without starting with a hard pull

-

You are looking for low-APR credit cards

-

You want to compare multiple product types

-

You already have credit union memberships

-

You have strong credit but want better rates

-

You are willing to deal with a manual credit union process

-

You understand prequalification is not final approval

This is probably not the best fit if you want instant, fully automated approval with no human involvement.

That is not really the credit union world.

Credit unions can offer strong deals.

But they often come with a little friction.

Who Should Be Careful

Be careful if:

-

You cannot risk a hard inquiry

-

You do not want to join new credit unions

-

You do not want manual follow-up

-

Your reports are messy right now

-

You are applying during a mortgage or auto loan process

-

You do not read application disclosures carefully

-

You assume every prequalification is guaranteed

Further can be useful.

But if your credit file is in a sensitive place, you need to move carefully.

What These Data Points Teach Us

The biggest lesson is not “Further always works.”

The real lesson is:

Further may show real credit union offers, but the handoff matters.

The data points show three possible outcomes.

A clean approval.

A broken process that got fixed.

A prequalification that stalled.

That is the full picture.

And honestly, that is more useful than a perfect success story.

Because if you try this, you need to know both sides.

Yes, there may be real soft-pull approvals.

Yes, the shown limits may be meaningful.

Yes, credit unions like Clearview and Teachers FCU may show up with strong offers.

But no, you should not assume the process is done until the credit union actually opens the card.

Frequently Asked Questions

What is Further Marketplace?

Further Marketplace is a credit union marketplace that lets consumers check personalized offers from credit unions. It can show products like credit cards, personal loans, auto loans, and home equity options.

Does Further Marketplace use a soft pull?

Further says users can explore personalized offers without impacting their credit score. Union Credit says credit union partners use a soft pull for pre-approval eligibility, but a credit union may perform a hard pull if you proceed with a final application.

Can you get a credit card through Further with no hard pull?

Yes, based on the Clearview FCU data points, it can happen. One person reportedly received a $15,000 card with no hard inquiry, and another had an existing card increased from $1,000 to $12,500 with no hard pull. But this is not guaranteed.

Is a Further pre-approval guaranteed?

No. A pre-approval or prequalification is not always final approval. The credit union can still review your membership, identity, eligibility, credit, and internal requirements.

What credit unions showed up in these data points?

The main credit unions in these data points were Clearview FCU and Teachers Federal Credit Union. Clearview had the completed $15,000 approval and $12,500 limit unlock. Teachers FCU showed a $20,000 offer that later stalled.

Should I freeze my credit reports after accepting an offer?

That tactic worked in one data point, but it is not guaranteed. A credit freeze may prevent a hard pull, but it can also cause the credit union to request an unfreeze, stall the application, or deny the account. Read all disclosures before trying it.

Conclusion

Further Marketplace is one of the more interesting soft-pull credit tools I have seen lately.

Not because it is perfect.

Because it is messy in a useful way.

The data points show real upside.

A $1,000 card turned into $12,500.

A $15,000 card opened at 10.74% APR with no hard inquiry.

A $20,000 Teachers FCU offer appeared with a confirmed limit and APR.

But the data points also show the risk.

The handoff can break.

The credit union can still deny.

A prequalification can look strong and still not finish.

So use Further the smart way.

Check offers.

Save screenshots.

Read the disclosures.

Understand that the credit union controls the final decision.

And do not take the first broken process as the final answer if the offer looked real.

Because sometimes the approval is not dead.

Sometimes it is just stuck in the credit union maze.