First Citizens Business Credit Card Approval: $20,000 With No Proof of Income

Jun 30, 2026

A small business owner reportedly walked away with a $20,000 First Citizens Bank business credit card approval with no proof of income required.

That is the kind of data point business owners pay attention to.

Because let’s be honest.

A lot of businesses do not have perfect revenue.

Some months are strong.

Some months are slow.

Some businesses are still building.

And if every lender asks for tax returns, bank statements, profit and loss statements, and full financials before even considering you, it can feel like a dead end.

That is why this First Citizens approval is interesting.

It shows how a relationship bank may still approve a strong applicant even when the business credit profile is not perfect.

Quick Answer

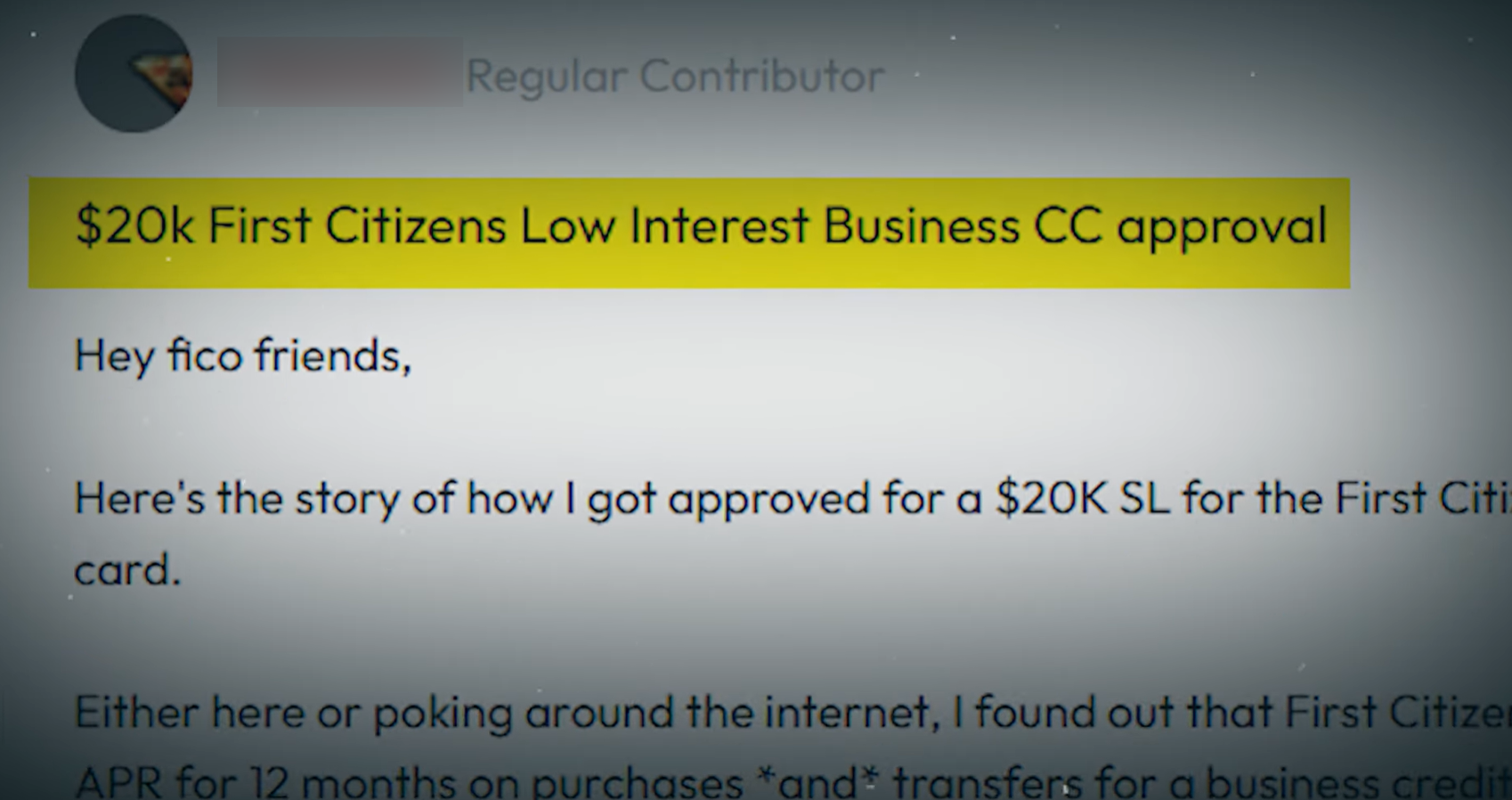

A business owner reportedly got approved for a $20,000 First Citizens Bank business credit card after opening a business checking account, funding it with only $100, applying through a branch relationship, and relying heavily on a strong personal credit profile. The bank reportedly did not require proof of income, tax returns, bank statements, or profit and loss documents for this approval. Your result may vary based on your personal credit, business credit, relationship with the bank, location, documentation, and underwriting.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you are comparing business credit cards with 0% APR offers, my 0% APR Business Credit Card Database can help you research banks, offers, bureau pulls, and approval data points before applying.

Why This First Citizens Approval Matters

First Citizens is not always the first bank people think about for business credit cards.

Most people jump straight to Chase, Amex, U.S. Bank, Bank of America, or Capital One.

But that is exactly why this data point matters.

Sometimes the best opportunities are hiding at regional or relationship-based banks.

First Citizens currently offers business credit cards, including a low-interest business card with 0% introductory APR for 12 months on purchases and balance transfers, no annual fee, and a variable APR after the intro period. That makes it worth paying attention to if you are trying to access business credit without paying interest right away.

The real story here is not just the card.

It is how the approval happened.

Finding the Hidden Opportunity

The business owner was not aggressively hunting for a new card.

They were doing normal credit research and found that First Citizens had a business card with a 0% intro APR offer.

That already made the card interesting.

But then came the twist.

Instead of a simple online application, the website pushed them to contact a local branch.

For people used to fully automated national banks, that can feel annoying.

But with relationship banks, the branch process can actually be the advantage.

A human can hear the story.

A human can understand the business.

A human can explain the process.

And sometimes, that human relationship helps the application land better than a cold online submission.

First Citizens Is a Relationship Bank

The person called the nearest branch, which happened to be only about 800 feet away from where they were staying.

The representative explained that First Citizens is a relationship bank.

That means they are not just looking at a one-time credit card application.

They want to know who you are as a business owner.

They want to build a banking relationship.

And before applying for the business credit card, the applicant was told they needed to open a First Citizens business checking account.

At first, that can sound like extra work.

But for relationship banks, it makes sense.

The checking account gives the bank a way to start the relationship before offering credit.

Why Opening Business Checking Helped

Opening a business checking account may seem like a small step.

But it can matter.

A business checking account can help show:

-

The business is real

-

The owner is willing to build a relationship

-

The bank may get future deposits

-

The applicant is not just applying and disappearing

-

There may be future product opportunities

Banks like customers who can grow with them.

A business owner who opens checking, uses the account, and applies through the branch may look more serious than someone submitting a random online application.

That does not guarantee approval.

But it can help with positioning.

The Credit Pull Question

One of the most important questions was how First Citizens would evaluate credit.

According to the data point, the representative explained that First Citizens looks at more than one score and may review personal and business credit to create an internal rating.

The business owner was naturally worried about multiple hard inquiries.

Nobody wants to see three hard pulls just to apply for one card.

But the actual result was better than expected.

The approval reportedly involved a hard pull on Experian Business only.

That is a big detail.

If accurate, that means the approval did not hit all three personal bureaus the way the applicant feared.

But this needs verification before publishing because credit pulls can vary by applicant, product, state, relationship, and underwriting path.

The Applicant’s Personal Credit Profile

The applicant’s personal credit was solid.

Here were the reported personal credit data points:

-

TransUnion: 752

-

Experian: 746

-

Equifax: 753

-

Overall utilization: 35.6%

The scores were good.

Not perfect.

But good.

The utilization was higher than I would normally like before a business credit application.

I prefer utilization closer to 10% or lower before applying for major credit.

But this approval shows you do not always need a perfect file to win.

A strong enough personal profile can still carry weight, especially when the bank takes a broader view.

The Business Credit Profile Was Not Perfect

This is where the data point gets even more interesting.

The business owner did not have perfect business credit.

They had some good pieces, but also some weak spots.

Reported business credit data points included:

-

D&B score: 80

-

Experian Business score: 67

-

Equifax Business score: 380

-

Only one tradeline reporting to Equifax Business

That Equifax Business score was weak.

And the Experian Business score had recently dropped.

The applicant believed the Experian Business drop may have been tied to a lack of reported net 30 accounts.

That is one of the frustrating things about business credit.

Not every account reports to every bureau.

You can look decent with Dun & Bradstreet and weak with Equifax Business at the same time.

That is why business credit can feel messy.

Existing Business Credit Cards Helped

The business owner already had multiple business credit cards reporting or in use.

Reported cards included:

-

Citizens Business Platinum: $25,000 limit, 35% utilization

-

NBKC Business Card: $3,000 limit, 47% utilization

-

Ameris Bank Business Card: $3,000 limit, 47% utilization

The utilization on those cards was not low.

But the existing limits showed the applicant had already managed business credit.

That matters.

If a bank sees other business cards already open, it may help show experience with business credit products.

The strongest card in the file was the $25,000 Citizens Business Platinum.

That likely helped.

Banks often pay attention to the highest limits other lenders have already trusted you with.

The Business Checking Visit

After the phone call, the business owner scheduled an in-person visit at the branch.

This part matters because relationship banking is human.

You are not just typing numbers into a form.

You are meeting someone.

You are answering questions.

You are creating a first impression.

The business owner had a tight schedule, and the bank representative was accommodating.

That matters too.

A helpful banker can make the process smoother.

The $100 Deposit

Here is the part people will love.

The business owner forgot to fund the account at first.

So they went to an ATM, withdrew $100, and funded the business checking account on the spot.

That was enough to get the account opened.

Not $10,000.

Not $25,000.

Not six months of business deposits.

Just $100.

Now, do not misunderstand this.

A $100 deposit did not magically cause a $20,000 approval.

The approval was based on the full profile.

But it does show that you may not need a massive deposit just to start the relationship.

For many business owners, that makes the bank feel more approachable.

How They Answered the Account Purpose Question

When asked why they were opening the business checking account, the owner gave a simple answer:

“To establish a relationship.”

That is clean.

That is honest.

That is exactly what they were doing.

You do not need to overcomplicate this.

If you are opening a business checking account because you want to build a relationship with the bank, say that.

Banks understand relationship-building.

They want more of it.

The Questions Banks May Ask

The bank asked some normal compliance-style questions.

For example, they wanted to know whether anyone in the applicant’s family was a public official in a foreign country.

They also asked whether 80% of the business income came from one client.

Questions like that can catch you off guard if you are not ready.

But they are normal.

Banks ask risk, identity, anti-money-laundering, and business activity questions all the time.

The key is simple:

Stay calm.

Answer honestly.

Do not overthink it.

Do not try to sound bigger than you are.

The Business Credit Card Application

The business owner had already emailed over the Articles of Incorporation ahead of time to speed up the process.

At the branch, they provided the basics:

-

ID

-

Business EIN

-

Social Security number

-

Annual gross income

-

Business documents

-

Signed application forms

The process was straightforward.

No unusual documentation.

No tax returns mentioned.

No bank statements mentioned.

No profit and loss statement mentioned.

That is why this approval stands out.

The Approval Came Fast

Less than 30 minutes after leaving the bank, the business owner received a phone call.

They were approved.

The limit:

$20,000.

That is a strong business credit card approval.

Especially considering the lower business credit scores and the small checking deposit.

The representative reportedly said the applicant’s personal credit profile was strong enough to support the approval.

That is the biggest lesson.

Even when business credit is imperfect, strong personal credit can still carry the file.

Why the Personal Credit Profile Carried the Approval

This approval appears to have leaned heavily on personal credit.

That makes sense.

The business credit profile had weak spots.

The checking relationship was brand new.

The account deposit was small.

So what made the bank comfortable?

Most likely:

-

Solid personal scores

-

Existing business credit experience

-

A strong prior business card limit

-

D&B score of 80

-

Relationship-based branch application

-

Proper business documentation

-

A real business banking setup

That combination was enough.

This is why I say business credit approvals are not about one score.

They are about the whole picture.

What They Did Right

This business owner did several things correctly.

First, they researched a less obvious bank.

That matters because everyone is chasing the same few lenders.

Second, they called the branch and talked to a real person.

That helped them understand the process before applying.

Third, they opened business checking first.

That showed relationship intent.

Fourth, they brought business documents.

That made the application cleaner.

Fifth, they had existing business credit cards.

That showed experience.

Sixth, they had strong enough personal credit.

That gave the bank comfort.

This was not luck.

It was a good profile meeting the right bank process.

Business Credit Does Not Have to Be Perfect

This is the most encouraging part.

The applicant’s business credit was not perfect.

Experian Business had dropped.

Equifax Business was weak.

Only one tradeline was reporting to Equifax Business.

Some existing business card utilization was high.

And they still got approved.

That does not mean business credit does not matter.

It does.

But it means imperfect business credit does not automatically kill the deal.

If the rest of the profile is strong enough, you can still win.

Why Tradelines Matter

One issue in this data point was thin reporting across business bureaus.

The applicant had vendors like:

-

Staples

-

Quill

-

Grainger

Those types of vendor accounts can help build business credit when they report.

But reporting can be inconsistent.

One account may report to Dun & Bradstreet.

Another may report to Experian Business.

Another may not report where you expected.

That is why business credit building can be frustrating.

You need tradelines, but you also need the right tradelines reporting to the right bureaus.

Helpful resource: If you want to build a cleaner business credit profile before applying for higher-limit cards, my Business Credit Buildout System is designed to help business owners prepare their profile for stronger funding approvals.

Why Relationship Banks Can Be Worth the Extra Work

A lot of people hate branch applications.

They want everything online.

I get it.

Online is faster.

But sometimes faster is not better.

A relationship bank can be worth the extra steps because the application may get more context.

Instead of a cold algorithm looking at a thin business file, you may have a banker who understands the full picture.

That does not guarantee approval.

But it can help when your file is not perfect.

This is especially true for business credit.

Business owners are not always clean and simple on paper.

A human conversation can matter.

How to Improve Your Odds With a Relationship Bank

If you want to try this kind of strategy, do not walk in unprepared.

Do this first:

-

Research the bank’s business credit card offers

-

Call the branch before visiting

-

Ask whether business checking is required

-

Ask what documents are needed

-

Bring ID

-

Bring Articles of Organization or Incorporation

-

Bring EIN confirmation if available

-

Know your annual gross income

-

Know your business revenue

-

Know your business purpose

-

Be ready to explain your business clearly

-

Keep personal credit utilization as low as possible

-

Know your business credit reports

The goal is to look organized.

Not perfect.

Organized.

What I Would Do Differently

This was a good approval.

But there are a few things I would improve before applying.

First, I would try to get personal utilization lower than 35.6%.

That is not terrible, but it is higher than ideal.

Second, I would work on getting more business tradelines reporting across Experian Business and Equifax Business.

Third, I would try to lower utilization on the existing business cards.

The NBKC and Ameris cards were both at 47% utilization.

That is not where I would want them before applying.

Fourth, I would confirm the bank’s credit pull policy before applying.

The rep may explain the process one way, but the actual pull can vary.

No Proof of Income Does Not Mean No Underwriting

This approval did not require proof of income, according to the data point.

But that does not mean the bank did not underwrite the file.

They still reviewed credit.

They still reviewed the business.

They still opened a checking account.

They still asked questions.

They still reviewed documents.

They still made a risk decision.

“No proof of income” does not mean “no review.”

It means this applicant was not asked to provide tax returns, bank statements, or income documentation for this specific approval.

That can happen.

But it is never guaranteed.

Frequently Asked Questions

Does First Citizens offer business credit cards?

Yes. First Citizens offers multiple business credit cards, including low-interest, cash back, and rewards options. Its low-interest business card currently lists a 0% introductory APR for 12 months on purchases and balance transfers.

Can you get a First Citizens business credit card with no proof of income?

This data point says the applicant was approved for $20,000 without proof of income, tax returns, bank statements, or profit and loss statements. But document requests can vary by applicant, product, branch, and underwriting.

Does First Citizens require a business checking account first?

In this data point, the applicant was told to open a First Citizens business checking account before applying for the business credit card. Verify with your local branch because requirements may vary.

What credit bureau does First Citizens pull for business cards?

In this data point, the approval reportedly involved a hard pull on Experian Business. But the representative also described a broader internal review process, and credit pulls can vary.

Can weak business credit still get approved?

Yes, it can happen if the rest of the profile is strong enough. In this data point, the applicant had weak Equifax Business and imperfect Experian Business scores, but stronger personal credit and existing business credit experience helped.

How much did the applicant deposit into First Citizens business checking?

The applicant reportedly funded the business checking account with only $100. That started the relationship, but the approval was likely based on the full credit and business profile, not the deposit alone.

Conclusion

This First Citizens Bank data point is powerful because it shows a real-world business credit approval that was not perfect on paper.

The applicant had solid personal credit.

But business credit had weak spots.

The checking account was brand new.

The deposit was only $100.

And First Citizens still reportedly approved a $20,000 business credit card without requiring proof of income.

That is why relationship banks deserve attention.

Sometimes the best move is not another giant national bank application.

Sometimes it is a regional bank, a branch conversation, and a clean business setup.

But do not copy this blindly.

Get your documents together.

Lower utilization if possible.

Know your business credit reports.

Build tradelines.

Open the relationship the right way.

And remember:

No-doc approval does not mean no underwriting.

It just means the file was strong enough that the bank did not ask for more.