Fetch American Express Card Approval: $7,000 Limit With No Hard Pull

Jun 27, 2026

I just got approved for a $7,000 limit on the Fetch American Express Card.

And the most interesting part is this:

I did not get hit with a hard pull.

If you have ever stared at an “Apply” button like it was a loaded weapon, you already know why that matters.

Most credit card applications feel like a gamble.

You apply.

You take the hard inquiry.

Then you hope the bank likes you.

But when a card lets you see your offer first, the whole experience feels different.

You get more information before making a decision.

And in my case, the Fetch card showed the approval, showed the limit, and let me accept without a hard pull appearing on my reports.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I was approved for the Fetch American Express Card with a $7,000 limit after applying through the Fetch app. The application first went under review, then about two hours later I was approved. I used a bureau-freeze strategy before accepting the offer, and in my case, no hard pull appeared. This is my personal data point, not a guarantee that every applicant can avoid a hard inquiry.

What Is the Fetch American Express Card?

The Fetch American Express Card is a no-annual-fee credit card tied to the Fetch rewards app.

It runs on the American Express network.

But the account itself is issued by First Electronic Bank, with Imprint powering the card program and backend experience.

That distinction matters.

This is not the same as applying for an American Express Gold Card, Platinum Card, Blue Cash Everyday, or Blue Business Plus.

You are not being underwritten by American Express the same way you would be with a traditional Amex-issued card.

This is a co-branded card that uses the American Express payment network.

That means you can use it where American Express is accepted.

But the issuer and underwriting setup are different.

And that explains why this card may approve profiles that a traditional Amex-issued card might not approve.

Why People Are Paying Attention to This Card

There are a few reasons the Fetch card is getting attention.

The big ones are:

-

You can see if you are approved before accepting

-

The initial application does not impact your score

-

Some people are seeing real starting limits

-

No income documents were required upfront in my case

-

The card has no annual fee

-

It runs on the American Express network

-

The rewards can stack with the Fetch app ecosystem

That combination is not common.

A no-annual-fee card that can show an offer before acceptance and potentially avoid a hard pull is worth watching.

Especially for people who are tired of applying blindly.

Helpful resource: If you want more cards with soft-pull preapproval paths, my Free Credit Card & Loan Pre-Approval Master List tracks cards and lenders that may let you check your odds before risking a hard pull: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

My Real Fetch Card Approval Experience

Here is exactly how it played out for me.

I applied through the Fetch app.

After submitting the application, I did not get an instant final approval.

Instead, the app showed that my application was under review.

So I waited.

About two hours later, I received a notification that I had been approved.

No income documents.

No email asking me to upload bank statements.

No extra verification steps.

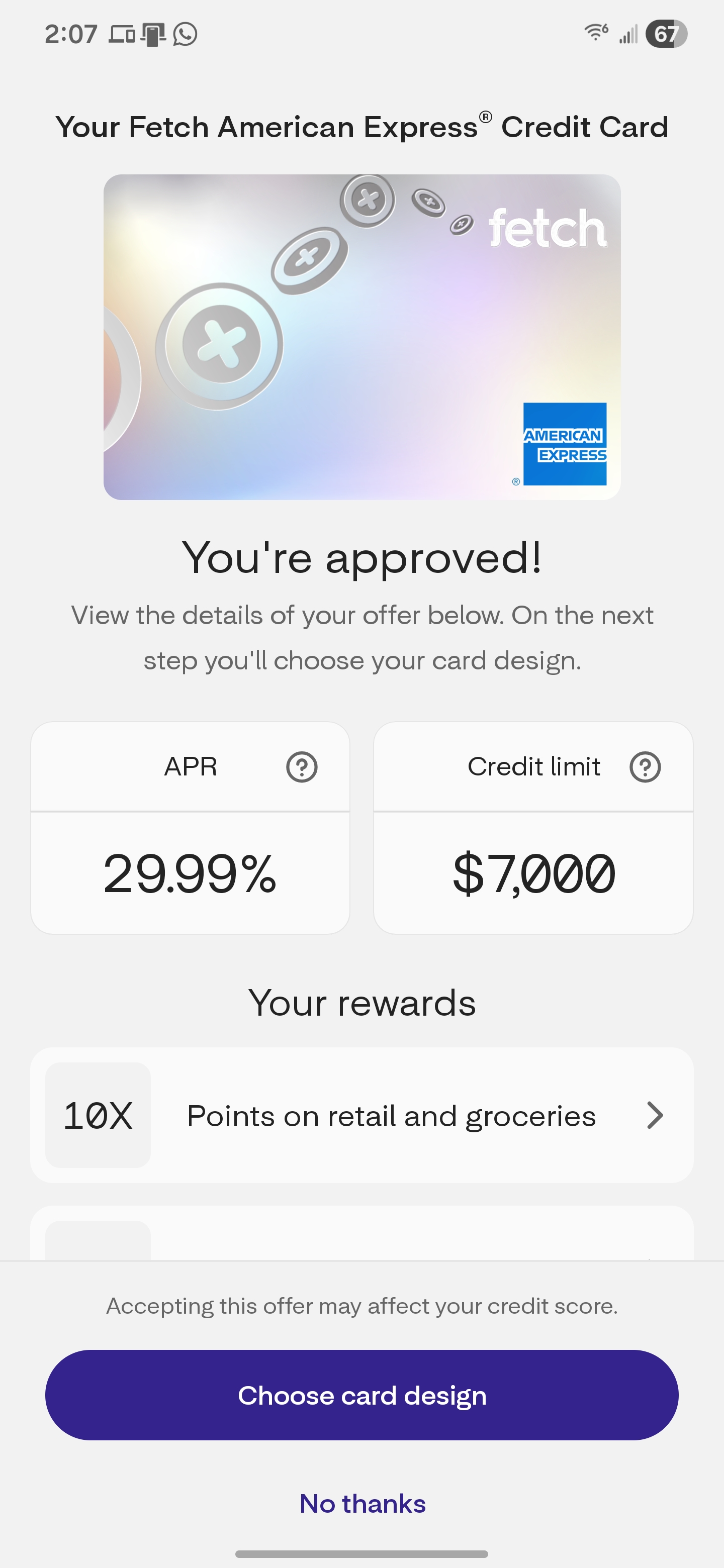

The starting limit came in at $7,000.

For a newer co-branded card, that was a solid result.

The Credit Bureau Data Point

One important data point is that Imprint has commonly been associated with TransUnion pulls in my experience.

That is what they used on my other Imprint card, the Rakuten card.

And based on that, TransUnion was likely the bureau involved here too.

So if you are thinking about applying, make sure your TransUnion report is unfrozen before you try to view the offer.

If the bureau they need is frozen, you may not be able to see the offer at all.

That does not mean every applicant will see the same bureau pull behavior.

But based on my Imprint experience, TransUnion is the bureau I would pay attention to first.

The 3-Step Play I Used Before Accepting

Before accepting the Fetch card, I used the same basic three-step play I have used with other cards.

Here is what I did:

-

I unfroze my TransUnion credit report so I could view the offer.

-

I confirmed the approval and limit inside the app.

-

I immediately re-froze all three credit bureaus, waited about 10 minutes, then accepted the card.

The result?

No hard pull appeared.

Nothing showed before acceptance.

Nothing showed after acceptance.

And once the account was approved, I opened the Imprint app and could see two cards listed:

-

My Rakuten card

-

My new Fetch card

That confirmed the card was added to my Imprint setup.

This Is Not a Guaranteed No-Hard-Pull Method

I want to be clear.

This is not a guarantee.

Freezing your reports before accepting an offer does not force every issuer to approve you without a hard pull.

Some lenders may still require you to unfreeze before acceptance.

Some may deny the application.

Some may delay the account.

Some may use a different bureau than expected.

Some may change their process over time.

So do not treat this like a loophole that works everywhere.

Treat it like one personal data point.

In my case, it worked.

But your result may be different.

About the “Guaranteed Limit” Language

You may hear people call this type of offer a “guaranteed limit.”

I understand why.

If the app shows you a limit and you accept the card, that appears to be the limit you receive.

In my case, the approval showed the $7,000 limit, and that is what I received.

But I would still be careful with the word guaranteed.

Nothing is guaranteed for every applicant.

The better way to say it is this:

If you are shown a firm offer with a specific limit and you accept it, the limit appears to be the actual starting limit you receive.

That is different from a normal credit card application where you apply first and only learn the limit after approval.

How Fetch Rewards Work

The Fetch card earns Fetch points instead of traditional cash back or Membership Rewards points.

The rough math many people use is:

1,000 Fetch points is around $1 in value.

But redemption value can depend on how and where you redeem.

The base earning structure is:

-

10 points per dollar at grocery and retail

-

5 points per dollar everywhere else

So on the surface, this is not a traditional 2% cash back card.

It is a Fetch points card.

That means the value depends on how much you use the Fetch ecosystem.

Spin & Win Adds Another Layer

The card also includes a Spin & Win feature.

Every purchase gives you the chance to open the Fetch app and spin for bonus points.

That makes the card more interactive than a normal credit card.

Some people will like that.

Others will find it annoying.

If you want a card that quietly earns rewards without you touching an app, this may not be the best fit.

But if you already use Fetch, scan receipts, activate offers, and check the app regularly, the card may fit your behavior better.

How Fetch Stacks Rewards

This is the part most people misunderstand.

Fetch is not just a credit card.

It is a rewards ecosystem.

The credit card is only one layer.

Here is how the stacking can work:

First, there is basic receipt earning.

You scan receipts or link online retailers, and Fetch gives you points.

That can happen whether you have the credit card or not.

Second, there are brand bonuses.

Fetch partners with specific brands and stores, so certain products and offers may earn extra points.

Those offers rotate, and that is where a lot of the extra value can come from.

Third, there is the credit card layer.

When you use the Fetch card, you can earn points from the card itself.

Fourth, every card purchase can unlock Spin & Win.

So one grocery trip could potentially generate:

-

Receipt points

-

Brand offer points

-

Card points

-

Spin bonus points

That is the real play.

The value is not just swiping the card.

The value is stacking the card with the rest of the Fetch app.

This Card Rewards Participation

The Fetch card works best for people who actually use the app.

If you are opening the app, scanning receipts, activating offers, and spinning after purchases, the value can stack.

If you are not doing those things, the card becomes much weaker.

That is why I would not compare this card only to a basic flat cash back card.

A flat 2% card is passive.

You swipe and move on.

The Fetch card is more interactive.

That can be good if you already like Fetch.

It can be annoying if you do not.

The Mistake I Already See People Making

The mistake is trying to turn this into your main card.

That is not how I would use it.

I see this more as a bridge card.

Use it lightly.

Use it consistently.

Let it age.

Let it report.

Let it help your profile.

But do not force spending just to chase Fetch points.

And definitely do not carry a balance.

The card’s purchase APR can be high, so paying interest would wipe out the value of the rewards quickly.

A rewards card is only a win if you pay it in full.

Why This Card Can Help Your Credit Profile

A $7,000 limit can still be useful even if the card is not your main card.

It can help your profile by adding available credit.

That can support lower utilization if you manage the account correctly.

It can also add another positive tradeline if the card reports properly and you pay on time.

But this only helps if you treat the card responsibly.

That means:

-

Pay on time

-

Keep utilization low

-

Do not overspend

-

Do not carry a balance

-

Do not apply just because you like the limit

The approval is the start.

How you manage the card afterward is what matters.

Who the Fetch Card Makes Sense For

The Fetch American Express Card may make sense if:

-

You already use the Fetch app

-

You like scanning receipts

-

You activate offers regularly

-

You do not mind opening the app after purchases

-

You want a card with no annual fee

-

You want to see your approval and limit before accepting

-

You are trying to add available credit without applying blindly

-

You pay your balances in full

For that type of person, this card is interesting.

Especially if the app shows you a solid starting limit.

Who Should Skip the Fetch Card

The Fetch card may not make sense if:

-

You hate managing rewards apps

-

You want simple cash back

-

You do not use Fetch

-

You do not want Amex acceptance limitations

-

You plan to carry a balance

-

You are only applying because you saw someone else get approved

-

You want a premium rewards card with travel perks

This is not a luxury card.

This is not a travel card.

This is not a traditional cash back card.

It is a Fetch ecosystem card.

That is either useful or annoying depending on how you already shop.

Frequently Asked Questions

Is the Fetch American Express Card issued by Amex?

No. The Fetch American Express Card runs on the American Express network, but the account is issued by First Electronic Bank and powered by Imprint.

Does applying for the Fetch card hurt your credit?

According to Fetch, applying lets you see whether you are approved without impacting your credit score. If you accept the offer, there may be a standard credit check that could affect your score.

What credit bureau does the Fetch card pull?

Based on my experience with Imprint cards, TransUnion is the bureau I would watch closely. However, bureau pulls can vary, so do not assume every applicant will have the exact same experience.

What limit did you get on the Fetch card?

I was approved for a $7,000 starting limit.

Does the Fetch card have an annual fee?

No. The Fetch American Express Card has no annual fee.

How do Fetch card rewards work?

The card earns Fetch points. The base earning structure is 10 points per dollar at grocery and retail and 5 points per dollar on all other purchases. Those points can stack with receipt points, brand offers, and Spin & Win bonuses inside the Fetch app.

Final Thoughts

The Fetch American Express Card is one of the more interesting newer soft-pull-style credit card approvals I have tested.

I got approved for a $7,000 limit.

The application went under review first.

About two hours later, I got the approval.

And after using my bureau-freeze strategy before accepting, no hard pull appeared on my reports.

That makes the data point worth paying attention to.

But I would not treat this as a universal no-hard-pull guarantee.

The issuer can change the process.

Your bureau situation may be different.

And some applicants may still be required to complete a credit check before acceptance.

The better takeaway is this:

Cards that show your approval and limit before acceptance give you more control than blind applications.

And if you already use Fetch, this card may be a useful bridge card that adds available credit and stacks with the app’s reward system.

Just do not force spending.

Do not carry a balance.

And do not apply only because someone else got a good limit.

Use the offer as data.

Then decide whether the card actually fits your wallet.