I Got Approved for a Credit Union 1 Card With 21 Months of 0% APR

Jun 25, 2026

Getting approved for a credit card from a giant national bank is one thing.

But getting approved by an out-of-state credit union with no prior relationship?

That makes me pay attention.

I recently got approved for a Credit Union 1 credit card offering 21 months of 0% APR, even though I had no checking account, no savings account, no deposits, no direct deposit, and no history with the credit union at all.

And honestly, approvals like this are exactly why I keep telling people not to ignore smaller banks and credit unions.

Some of the best credit card and funding opportunities are not always sitting at Chase, Amex, Capital One, or Wells Fargo.

Sometimes they are hiding inside regional banks and credit unions most people have never even considered.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

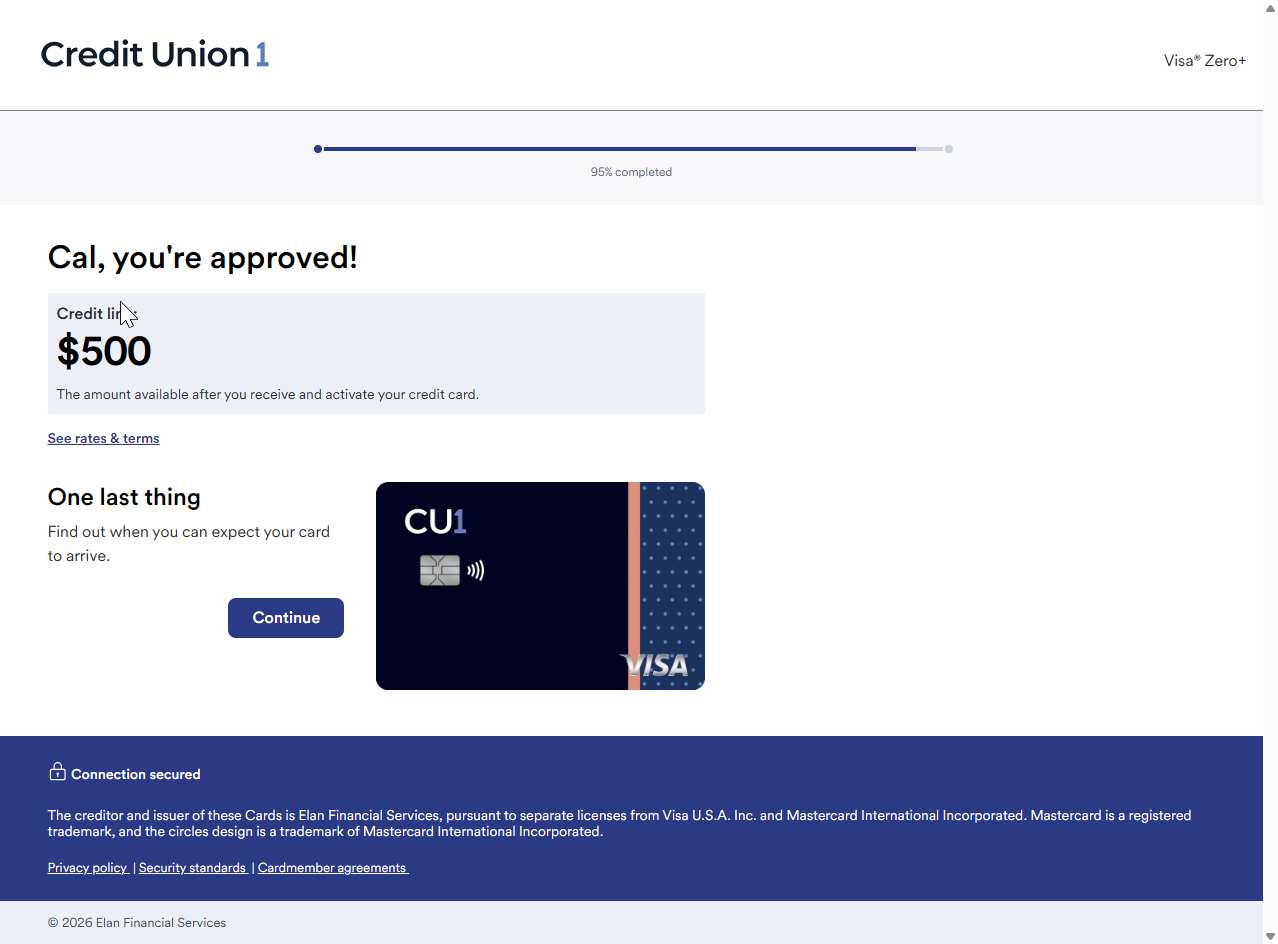

I was approved for a Credit Union 1 credit card with a 21-month 0% APR offer after receiving a soft-pull pre-approval first. I had no prior relationship with Credit Union 1, and the hard pull landed on Equifax for me. My starting limit was only $500, but the bigger story is that I was able to get approved cold through an out-of-state credit union.

What Is Credit Union 1?

The credit union is called Credit Union 1.

They have been around for 68 years, and most of their physical branches are in places like Illinois, Minnesota, Indiana, and Michigan.

Meanwhile, I’m in North Carolina.

So when I first saw the card, my immediate thought was:

“There’s no way I can even join this thing.”

But after calling them directly, the rep told me nationwide membership was available through a small membership fee of around $5.

That immediately got my attention.

Because a lot of smaller banks and credit unions have extremely competitive products, but most people never even look into them because they assume membership is restricted.

And sometimes it is.

But sometimes there is a simple membership path that opens the door.

Helpful resource: If you want to find more credit unions that may be open to people outside their local area, my 150+ Credit Unions Anyone Can Join Database can help you start your research: https://courses.calbartoncashback.com/CreditUnions

The Soft-Pull Pre-Approval Was the Big Surprise

The most interesting part of this approval was not even the card itself.

It was the soft-pull pre-approval.

Before I fully applied, Credit Union 1 showed me a pre-approval.

And remember, I was not even a member yet.

That matters because applying with smaller banks and credit unions can sometimes feel risky.

You do not always know if you are walking into:

-

An instant denial

-

A tiny limit

-

A hard inquiry for nothing

-

A long manual review

-

A real approval opportunity

But in this case, I got a soft-pull pre-approval first.

Then I went through the full application.

And the pre-approval ended up being accurate.

I was approved.

The hard pull landed on Equifax for me, which is an important data point if you are tracking credit bureau pulls.

Helpful resource: Before applying for a new card, it may be worth checking my Free Credit Card & Loan Pre-Approval Master List so you can find lenders that may let you check your odds before taking a hard pull: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Why Elan Financial Services Matters

The Credit Union 1 credit card is managed through Elan Financial Services.

Most people have never heard of Elan, but Elan quietly powers credit card programs for a large number of banks and credit unions across the country.

That is why this approval caught my attention.

If more Elan-backed banks and credit unions start rolling out soft-pull pre-approvals directly on their card landing pages, this could become a much bigger opportunity over time.

Because now you are not just looking at one credit union.

You are potentially looking at a whole network of smaller institutions that may eventually offer a similar pre-approval experience.

That does not mean every Elan-backed card will approve you.

It does not mean every institution will use the same rules.

And it definitely does not mean pre-approval is guaranteed.

But it does mean this trend is worth watching.

My Starting Limit Was Only $500

Now, let me be fully transparent.

My starting limit was low.

Only $500.

And I know some people will immediately say:

“What can I even do with a $500 limit?”

I get it.

But I do not think the starting limit is the most interesting part of this story.

The more important part is how I got approved.

This approval was completely cold.

No checking account.

No savings account.

No direct deposits.

No branch visits.

No prior relationship at all.

That changes how I look at the $500 starting limit.

Instead of seeing it as the final result, I see it more like Phase 1.

The real test is what happens after the relationship begins.

Why Relationship Banking Still Matters

This is the part a lot of people underestimate with smaller institutions.

Regional banks and credit unions can care a lot about relationship banking.

Sometimes they want to see:

-

Deposits

-

Account activity

-

Direct deposits

-

Debit card usage

-

Savings growth

-

Internal trust

-

Time as a member

That does not always mean you need a long relationship before getting approved.

Clearly, in my case, I got approved without one.

But the relationship may matter more when it comes to future credit limit increases, additional products, or stronger approvals later.

So instead of looking at this approval like:

“Only $500?”

I’m looking at it like:

“Okay, now the relationship starts.”

And with a 21-month 0% APR offer attached to the card, this is still an interesting approval even with a low starting limit.

Why the 21-Month 0% APR Offer Stands Out

The 0% APR offer is one of the biggest reasons this card caught my attention.

A lot of cards people talk about offer:

-

12 months

-

15 months

-

Maybe 18 months

But 21 billing cycles of 0% APR is strong.

Especially in today’s environment.

And it stands out even more because this is coming from a credit union many people outside its region may not even know about.

That is the bigger lesson here.

Sometimes smaller institutions quietly have strong products, but they do not get the same attention as the giant national banks.

So people miss them.

The Bigger Trend: Soft-Pull Pre-Approvals Are Becoming More Important

I think more people should pay attention to the soft-pull pre-approval trend.

Because psychologically, it changes the entire application experience.

There is a big difference between:

“I hope this works.”

And:

“They already told me I have a real shot.”

That matters when hard inquiries are involved.

Now, pre-approvals are never guarantees.

Your credit profile, income, state, relationship, debt, inquiries, utilization, and lender rules can all affect the final decision.

But I do think consumers are becoming way more sensitive to unnecessary hard pulls.

Especially experienced applicants.

People do not want to burn hard inquiries just to get denied instantly or approved for a limit that does not make sense.

That is why soft-pull pre-approval tools are becoming more valuable.

Helpful resource: I also put together a list of cards that may reveal your starting limit before approval. You can check it here: https://offers.calbartoncashback.com/Links

What I’m Testing Next

For now, I’m probably going to become a member officially and start building the relationship properly.

That may include:

-

Deposits

-

Debit card activity

-

Internal transfers

-

Possibly direct deposits

-

More account activity over time

Then I want to see what happens over the next several weeks or months.

The big question is whether the relationship helps the limit grow.

Because if the card starts at $500 but grows meaningfully after internal activity, that becomes a much more useful data point.

And if it does not grow?

That is useful too.

Either way, I’ll have a better understanding of how Credit Union 1 treats this type of approval after the account relationship begins.

Frequently Asked Questions

Does Credit Union 1 offer credit card pre-approval?

In my case, I was able to see a soft-pull pre-approval before completing the full application. Pre-approval is not a guarantee, but it gave me a much better idea that I had a real shot before moving forward.

What credit bureau does Credit Union 1 pull?

For my application, the hard pull landed on Equifax. Your result may vary based on your state, profile, product, or underwriting details.

Do you need to live near Credit Union 1 to join?

I was in North Carolina while Credit Union 1 is mostly based in states like Illinois, Minnesota, Indiana, and Michigan. After calling them, I was told nationwide membership was available through a small membership fee of around $5.

What was the starting limit?

My starting limit was $500. That is low, but I still think the approval is interesting because I had no prior relationship with the credit union before applying.

Is a soft-pull pre-approval a guaranteed approval?

No. A pre-approval is never a guaranteed approval. It can be a useful signal, but the lender can still deny the final application after reviewing your full profile.

Why does this approval matter?

This approval matters because it shows that some smaller banks and credit unions may offer strong credit card products, soft-pull pre-approvals, and possible approval opportunities even if you do not live near a branch or already have a relationship.

Final Thoughts

This Credit Union 1 approval changed how I look at smaller institutions.

Yes, the starting limit was only $500.

But the card came with a 21-month 0% APR offer, a soft-pull pre-approval before the full application, and an approval with no prior relationship.

That combination is what makes this interesting.

The bigger lesson is simple:

Do not only look at the giant national banks.

There may be hidden credit card and funding opportunities sitting inside smaller banks and credit unions that most people never research.

And if more Elan-backed institutions start rolling out soft-pull pre-approvals, this could become an even bigger trend over time.

For now, I’m treating this as the beginning of the data point, not the end.

The real question is what happens after I build the relationship.