Credit Union 1 Auto Credit Limit Increase: From $500 to $10,000 in Less Than a Week

Jun 27, 2026

Over a week ago, Credit Union 1 approved me for a credit card with a $500 starting limit.

And honestly, I was not excited.

A $500 limit is not exactly what you hope for when you are chasing higher-limit credit cards.

But I also said something important at the time:

The real story was not the $500 limit.

The real story was how I got approved.

I had no prior relationship with Credit Union 1.

I was not located in the same state.

I was able to check for a soft-pull preapproval first.

And the card was backed by Elan Financial Services, which powers credit card programs for banks and credit unions all over the country.

So I looked at the $500 approval as Phase 1.

Then Phase 2 happened way faster than I expected.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

My Credit Union 1 credit card was first approved with a $500 limit, but less than a week later the limit automatically increased to $10,000 after I activated the card. I did not request the increase, call the credit union, open a checking account, or send a secure message. This may have been an internal review, a placeholder-limit adjustment, or something triggered after activation, but I cannot confirm the exact reason yet.

The Original Credit Union 1 Approval

The first approval was underwhelming on the surface.

A $500 starting limit is low.

Especially when you are used to looking for credit cards that can produce more usable limits.

But the approval still caught my attention because of the setup.

This was not a local credit union I had banked with for years.

This was not a card where I had a strong existing relationship.

This was not even a situation where I lived in the same state.

The more interesting part was that Credit Union 1 allowed me to check for preapproval first.

That matters because a soft-pull preapproval can help you test the waters before risking a hard inquiry.

It does not guarantee final approval.

But it is much better than applying completely blind.

Helpful resource: If you are tired of taking hard pulls just to get denied or stuck with low limits, my Free Credit Card & Loan Pre-Approval Master List can help you find banks and cards that may let you check your odds before applying: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Why the Elan Connection Matters

The other reason this approval stood out is because Credit Union 1’s credit cards are backed by Elan Financial Services.

That matters because Elan is not a tiny one-off card issuer.

Elan powers credit card programs for a large number of banks and credit unions nationwide.

So when something unusual happens with one Elan-backed credit card, I pay attention.

Not because it automatically means the same thing will happen everywhere else.

But because it raises a bigger question:

Could similar underwriting patterns, reviews, or limit adjustments be happening across other Elan-backed credit card programs?

That is what makes this data point more interesting than one random $500 approval.

Phase 2 Happened Fast

A few nights later, I was sitting on the couch with my wife watching YouTube.

It was around 9 PM.

I was halfway through a conversation when my phone buzzed.

I assumed it was just another normal notification.

Maybe a promo email.

Maybe a random account alert.

Maybe something I would ignore.

But when I glanced down, I saw it was from Credit Union 1.

At first, I thought it might be a welcome email or some account setup reminder.

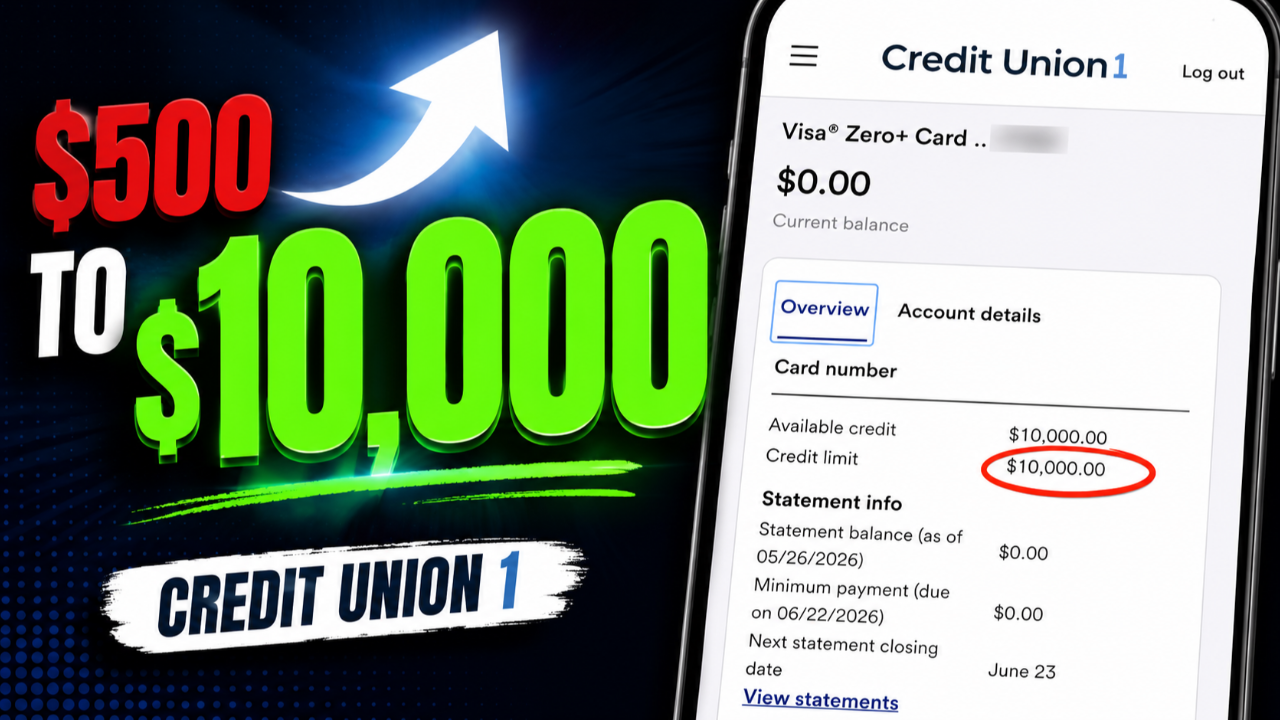

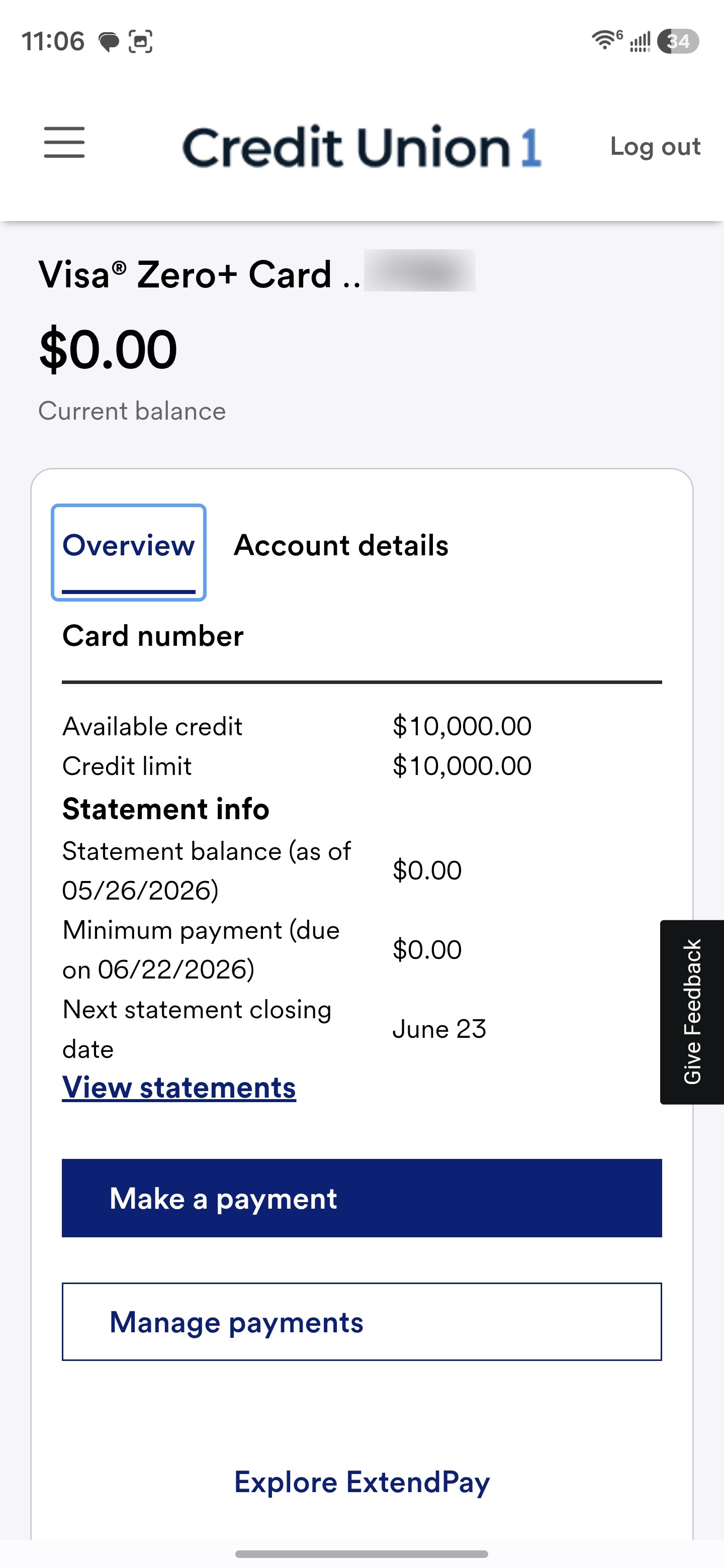

Instead, it was a notification telling me my credit limit had been increased.

Not from $500 to $1,000.

Not from $500 to $2,500.

From $500 all the way to $10,000.

That got my attention immediately.

I Did Not Request the Credit Limit Increase

This is the part that makes the data point so interesting.

I did not request a credit limit increase.

I did not call customer service.

I did not open a checking account.

I did not send a secure message.

I did not move money into Credit Union 1.

I had literally done nothing other than activate the card.

That is why I started asking a different question.

Was the original $500 limit just a placeholder?

Did activating the card trigger another review?

Did Elan or Credit Union 1 take a second look at my profile behind the scenes?

Was this an internal adjustment that was already planned?

I do not know yet.

But I do know this:

Going from $500 to $10,000 in less than a week completely changes how I look at the original approval.

The Starting Line Is Not the Finish Line

This is one of the biggest lessons from the whole situation.

The starting line is not always the finish line.

Most people would have seen the $500 limit and moved on.

And honestly, I get it.

A $500 approval can feel like a waste of time when you were hoping for a real limit.

But if I had dismissed the card immediately, I would have missed the bigger development.

Less than a week later, that same $500 card turned into a $10,000 card.

That is a massive difference.

And it is a reminder that some approvals may have more going on behind the scenes than the first screen shows.

Was the $500 Limit a Placeholder?

I cannot prove the $500 limit was a placeholder.

But that is one possibility.

Sometimes a lender may approve an account at a low initial limit while something is still being finalized.

Then later, after activation, verification, or an internal review, the limit may adjust.

Again, I am not saying that is officially what happened here.

I am saying the sequence raises the question.

Because a jump from $500 to $10,000 without a request is not normal.

That is not a standard credit limit increase experience.

That is not the typical “wait six months and ask again” process.

Something clearly happened behind the scenes.

Could Activation Have Triggered Another Review?

Another possibility is that card activation triggered some kind of additional review.

Maybe activating the card confirmed the account was real.

Maybe it completed the opening process.

Maybe it moved the account into a different status.

Maybe that caused the system to finalize the real credit line.

I do not know.

But the timing is hard to ignore.

I activated the card.

Then the limit jumped.

That does not prove activation caused it.

But it is enough to make me pay attention.

Why This Matters for Credit Union Cards

Credit union cards can be weird in a good way.

Some are conservative.

Some are relationship-heavy.

Some are slow.

Some are surprisingly generous.

And some are powered by third-party issuers like Elan, which means the credit union name on the front of the card may not tell the full underwriting story.

That is why these data points matter.

They help us understand what is happening underneath the surface.

A small credit union card with a soft-pull preapproval and an automatic jump to $10,000 is not something I would ignore.

What This Means for Elan-Backed Credit Cards

The Elan angle is the part I am most curious about now.

Elan works with a large number of banks and credit unions.

That means many local or regional financial institutions may offer credit cards that are actually issued and serviced through Elan.

So now I am wondering:

Are other Elan-backed cards doing similar post-approval reviews?

Are other small starting limits turning into larger lines after activation?

Are some institutions showing conservative limits first and adjusting later?

Are there patterns across different Elan bank and credit union partners?

I do not have those answers yet.

But this Credit Union 1 update makes me want to keep watching the entire Elan ecosystem more closely.

Why Soft-Pull Preapproval Still Matters

The soft-pull preapproval is a major part of this story.

A $500 starting limit would be much more frustrating if I had blindly taken a hard pull with no warning.

But because I was able to test the preapproval first, the risk was lower.

That is why I like cards that let you check before applying.

Preapproval is not perfect.

It does not guarantee approval.

It does not guarantee a certain limit.

And the final application can still involve a hard pull.

But it gives you more information before making a decision.

That is the key.

You are not walking in completely blind.

Why You Should Not Automatically Dismiss Low-Limit Approvals

I still do not love low starting limits.

Nobody gets excited about a $500 credit line.

But this situation shows why you should be careful before writing off an account immediately.

A low starting limit can sometimes be:

-

A true low-limit approval

-

A conservative first decision

-

A temporary placeholder

-

A limit that may grow after activation

-

A relationship-building starting point

The problem is you usually do not know which one it is at first.

That does not mean you should accept every low-limit card.

But it does mean you should understand the system before assuming the card is useless.

In my case, the card went from disappointing to very interesting in less than a week.

What I’m Doing Next

For now, I am going to keep using the card and continue documenting what happens.

I want to see:

-

How the account reports

-

Whether the $10,000 limit reports correctly

-

Whether future credit limit increases are possible

-

Whether Elan offers more products later

-

Whether Credit Union 1 starts showing other relationship opportunities

-

Whether similar patterns appear with other Elan-backed cards

This is not just about one card anymore.

Now I am curious about the broader system.

Should You Try Credit Union 1?

Credit Union 1 may be worth researching if you are interested in:

-

Out-of-state credit union opportunities

-

Soft-pull preapproval paths

-

Elan-backed credit cards

-

Cards that may start small but have growth potential

-

Credit union approvals without a prior relationship

But do not apply just because I got an auto increase.

Your result could be completely different.

You may not get approved.

You may get a low limit that stays low.

You may face different membership rules.

You may receive different underwriting treatment.

This is a data point.

Not a guarantee.

A Smarter Way to Approach Cards Like This

If you are going to test cards like this, I would approach them carefully.

First, check whether there is a soft-pull preapproval path.

Second, read the terms before applying.

Third, understand whether the final application may create a hard inquiry.

Fourth, pay attention to emails after approval.

Fifth, do not ignore the account just because the first limit is low.

And finally, document what happens.

Sometimes the most important part of the story happens after the approval screen.

Helpful resource: If you specifically want cards that may reveal your starting limit before approval, check out my list of 9 credit cards that reveal your starting limit before approval: https://offers.calbartoncashback.com/Links

Frequently Asked Questions

Did Credit Union 1 automatically increase your credit limit?

Yes. My Credit Union 1 card started with a $500 limit and automatically increased to $10,000 less than a week later. I did not request the increase.

Did you ask for the Credit Union 1 credit limit increase?

No. I did not call, send a secure message, open checking, or request a credit limit increase. The increase happened automatically after activation.

Was the original $500 Credit Union 1 limit a placeholder?

It may have been, but I cannot confirm that yet. The limit jumping from $500 to $10,000 so quickly makes that a reasonable question, but I do not know the official reason.

Is Credit Union 1 backed by Elan Financial Services?

Credit Union 1 credit cards are issued by Elan Financial Services. That matters because Elan powers credit card programs for many banks and credit unions.

Does Credit Union 1 offer soft-pull preapproval?

In my case, I was able to check for preapproval before moving forward. Soft-pull preapproval can help reduce the risk of applying blindly, but final approval may still involve a hard pull.

Should I apply for Credit Union 1 just because of this data point?

No. This is one personal data point, not a guarantee. Research the card, membership requirements, preapproval path, bureau pull, and current terms before applying.

Final Thoughts

My Credit Union 1 card started as a disappointing $500 approval.

Less than a week later, it became a $10,000 limit.

That completely changed how I viewed the account.

And it reminded me of something important:

The starting line is not always the finish line.

Sometimes the first approval screen does not tell the full story.

Sometimes the real action happens after activation, internal review, or relationship setup.

I still do not know exactly why the limit jumped.

But I do know this was one of the more interesting credit union updates I have seen recently.

And because the card is backed by Elan Financial Services, I am now paying closer attention to what may be happening across other Elan-backed credit card programs.

For now, I will keep using the card, track how it reports, and watch what happens next.

Because if a $500 approval can become $10,000 in less than a week, this is definitely worth documenting.