Credit Key Business Credit Review: I Got Approved for $5,000 With No Hard Pull

Jun 29, 2026

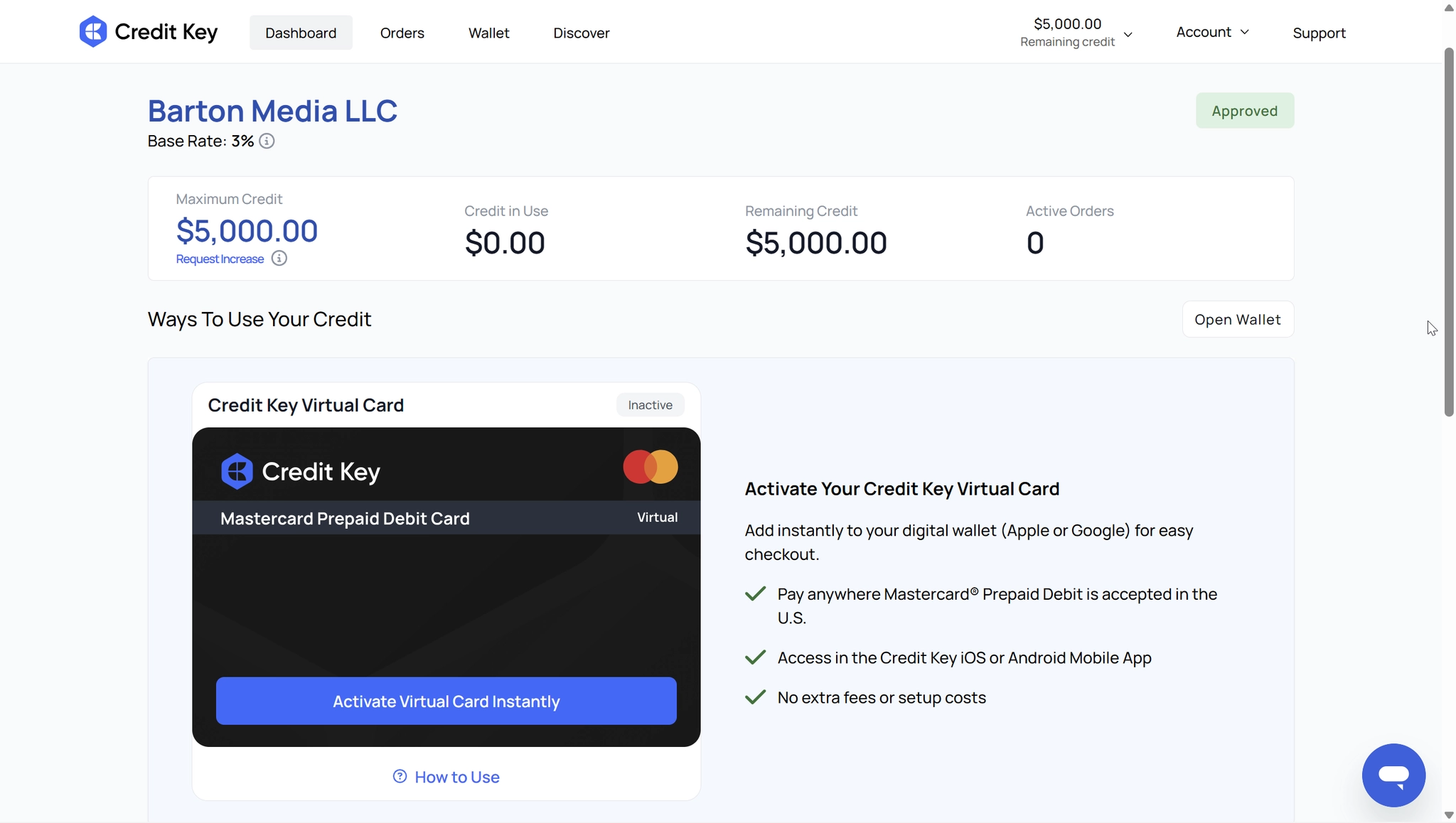

I just got approved for a $5,000 business credit line with Credit Key.

No hard pull.

Approval in under 5 minutes.

And less than 24 hours later, that limit increased to $7,500 after I submitted business bank statements.

That got my attention fast.

Credit Key was not even on my radar the day before. But when I saw the basic requirements; a 600 FICO, $40,000 in annual business revenue, and soft pull only. I had to test it myself.

And honestly, Credit Key is more useful than I expected.

It is not a perfect product. Most small business owners should expect a personal guarantee, and the extended payment plans can come with monthly fees. But if you want a business credit option that does not hard pull your personal credit during the application process, this one is worth understanding.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Credit Key is a business credit line that may approve registered U.S. businesses with a 600 FICO score, at least $40,000 in annual revenue, and a soft pull from Equifax. I was approved for $5,000 in under 5 minutes, then increased to $7,500 overnight after submitting 3 months of business bank statements. Credit Key may require a personal guarantee for most small businesses, but the application can still be soft pull only, which makes it lower-risk upfront than many business credit products.

What Is Credit Key?

Credit Key is a business credit product that lets approved businesses buy now and pay later.

At first, it looked like a vendor-style credit line. That means you could use it with partner merchants and suppliers instead of swiping it anywhere like a normal business credit card.

But Credit Key has become more interesting because now it can include a virtual prepaid Mastercard and a physical Mastercard.

That changes the whole conversation.

Instead of only being useful with a limited vendor network, a portion of your line may be unlocked for general business purchases anywhere Mastercard is accepted.

That makes Credit Key feel more like a mix between:

-

A net-30 vendor account

-

A business credit line

-

A business charge card

-

A buy now, pay later financing tool

-

A vendor marketplace credit account

It is not exactly the same as a traditional business credit card, but it can be useful if your business needs short-term purchasing power without a hard pull.

Why Credit Key Matters for Business Owners

Most business funding options create friction.

Some lenders want hard pulls.

Some want tax returns.

Some want years in business.

Some want long bank statement reviews.

Some report to personal credit.

Some require strong credit and high revenue before they even take you seriously.

Credit Key stands out because the starting requirements appear more accessible than many business credit products.

The big appeal is:

-

Soft pull only

-

600 FICO minimum

-

$40,000 annual business revenue requirement

-

Fast approval potential

-

Reports to Dun & Bradstreet

-

Net-30 0% APR structure by default

-

Extended repayment options available

-

Virtual and physical Mastercard access

-

Vendor marketplace purchasing power

That is a solid combination.

But there are some important warnings too, especially around the personal guarantee and monthly fees.

Credit Key Requirements

Based on my application experience and the original data, Credit Key may require:

-

A registered U.S. business

-

LLC, corporation, or sole proprietorship

-

At least $40,000 in annual business revenue

-

A 600 FICO minimum

-

Equifax soft pull

-

Personal guarantee in most cases

That last part matters.

A lot of people hear “business credit” and assume it automatically means no personal guarantee. That is not true.

Credit Key may be soft pull only, but most small business owners should expect to personally guarantee the credit line.

There may be situations where larger businesses can qualify without a personal guarantee. The original content mentioned businesses doing $5 million or more in annual revenue or falling under an “Enterprise” classification as possible examples.

But for most small business owners, assume a PG may be required.

Helpful resource: If you are specifically looking for business cards that may not require a personal guarantee, my No PG Business Credit Card Master List can help you compare more options.

Does Credit Key Do a Hard Pull?

Credit Key did not hard pull my personal credit.

They used a soft pull from Equifax.

That means the application did not add a hard inquiry to my personal credit report.

This is the main reason Credit Key got my attention. A soft pull application gives you a chance to test the approval without taking the same credit score risk you would take with many traditional business credit cards or loans.

But here is the catch: your Equifax report may need to be unfrozen.

That is exactly what happened to me.

My Credit Key Approval Data Point

Here was my approval data point:

-

Equifax FICO was around 785

-

Instant approval limit was $5,000

-

Approval came in under 5 minutes after the freeze issue was fixed

-

20% of my limit was unlocked for general business use

-

That gave me $1,250 in universal spend right away

-

Less than 24 hours later, my limit increased to $7,500 after submitting bank statements

I did not get the highest possible limit.

But I did get a usable business credit line with no hard pull.

That is the part that matters.

Even better, the product became more useful because part of the limit could be used anywhere Mastercard is accepted.

My Approval Almost Got Stuck

My first application did not go through smoothly.

Not because my credit was bad.

Not because my business failed the basic requirements.

It got stuck because my Equifax report was frozen.

That is a good reminder.

A credit freeze protects you from fraud, but it can also block legitimate lenders from accessing your report, even when they are only doing a soft pull.

So Credit Key’s system could not see what it needed.

I called support expecting the usual nightmare: a chatbot, a long hold time, or someone reading from a script.

That is not what happened.

A U.S.-based rep answered in under 2 minutes. They pulled up my application quickly and told me the issue was my frozen Equifax report.

I unfroze Equifax, and the rep manually pushed the application back through underwriting.

Not even 5 minutes later, I received the approval email for $5,000.

That was one of the better customer support experiences I have had with a business credit product.

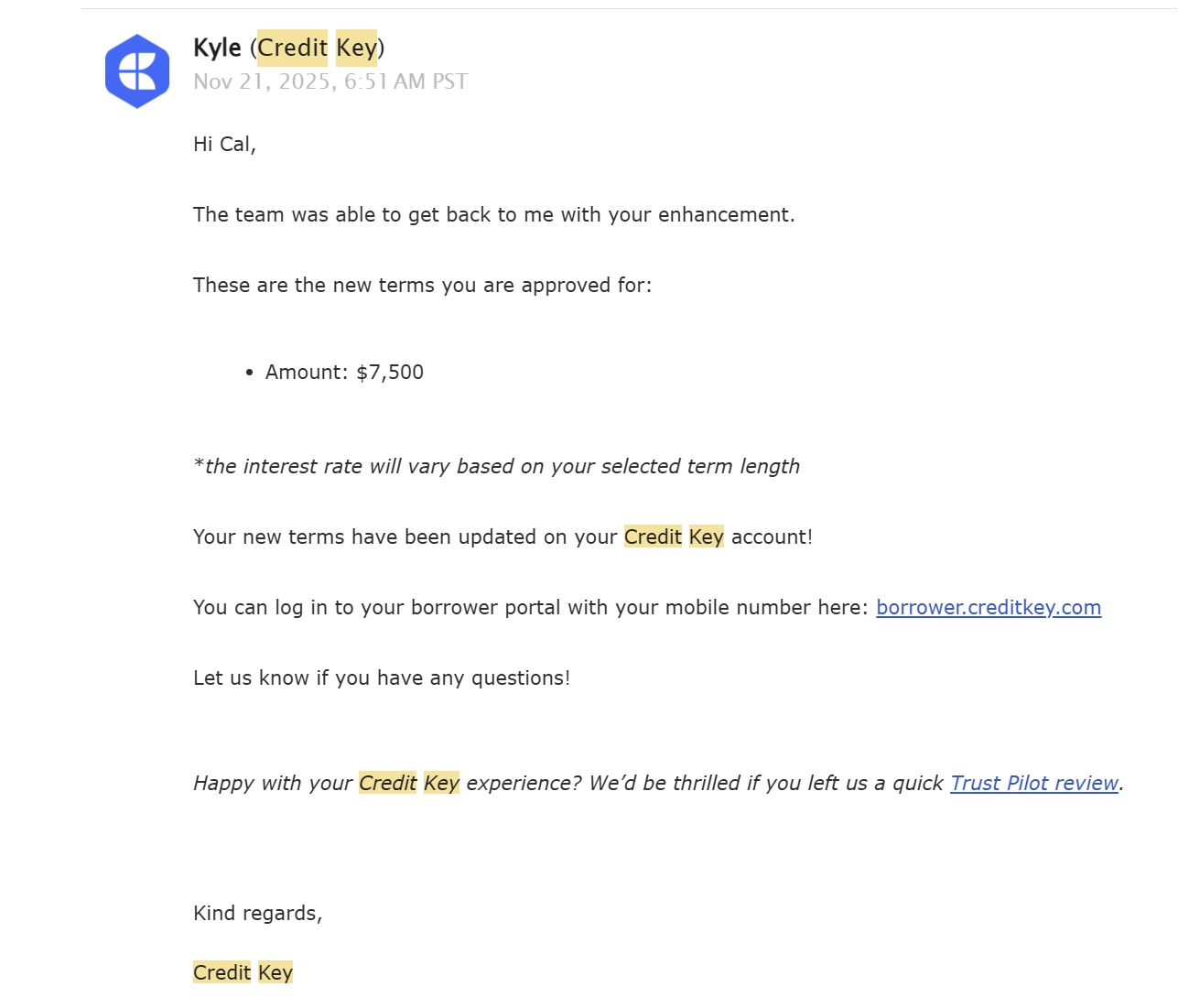

How I Increased My Credit Key Limit to $7,500

About an hour after I got approved, I received a call from a Credit Key relationship manager named Kyle.

He told me that if I wanted a higher limit, he could walk me through the process.

All I needed to do was fill out a short form and upload my last 3 months of business bank statements.

So I did it the same day.

The next morning, I checked my email and saw the new approval.

My limit increased from $5,000 to $7,500 overnight.

That was fast.

This is where Credit Key became more interesting to me. It was not just an instant approval product. There was also a path to a higher limit if you were willing to show business bank statements.

How Much Can Credit Key Approve You For?

Credit Key instant approvals may range from $1,000 to $50,000.

That does not mean everyone gets $50,000.

Your approval amount can depend on your credit profile, business revenue, business structure, underwriting, and any financial documents you provide.

In my case, the first approval was $5,000. After bank statement review, it increased to $7,500.

So the initial soft pull can get you in the door, but stronger business financials may help you get more.

How Credit Key Payments Work

By default, Credit Key uses a 0% APR net-30 structure.

That means you can make a purchase and pay it back within 30 days without interest.

That can be useful if you are using the credit line to cover short-term business expenses and then paying it off when revenue comes in.

If you need more time, purchases may be extended over 3, 6, or 12 months.

But those extended terms can come with monthly fees.

The original content mentioned monthly fees that typically range from 1% to 5% per month, depending on the term length, business profile, and underwriting.

That means this is not free money.

Net-30 can be powerful if you pay on time.

Extended terms can get expensive if you are not careful.

Does Credit Key Report to Business Credit?

Credit Key reports to Dun & Bradstreet, based on the original content.

That can help you build business credit history and vendor tradelines if you use the account responsibly.

Positive payment history can help your business profile.

Negative payment history can hurt it too.

That is why you need to treat Credit Key like a real credit line.

Because it is one.

The original content also said reporting may happen within the first 60 days.

That should be verified before publishing, but if accurate, it makes Credit Key useful for business credit building.

Helpful Resource: If your goal is to build a stronger business credit profile before applying for bigger funding, the Business Credit Buildout System is designed to help business owners build the foundation lenders want to see.

Where Can You Use Credit Key?

This is where Credit Key surprised me.

A portion of your limit may be unlocked as “universal spend.”

That means you can use that portion anywhere Mastercard is accepted.

For me, 20% of my $5,000 limit was unlocked right away. That gave me $1,250 for general business purchases.

Some people may get up to 50% of their limit unlocked, depending on their profile.

That makes the line much more useful.

You may be able to use the unlocked portion for normal business expenses like:

-

Amazon orders

-

Fuel and gas

-

Software subscriptions

-

Online tools

-

Office supplies

-

Facebook ads

-

Repairs

-

Client expenses

-

Equipment

-

Other legitimate business purchases

This is a major improvement over old-school vendor credit lines that only let you buy a narrow list of products you may not actually need.

Credit Key Vendor Marketplace

Credit Key also has a partner vendor marketplace.

That means you can shop with integrated merchants and choose Credit Key at checkout, similar to how you might use PayPal or Amazon Pay on different websites.

The original content mentioned big-name brands like:

-

Apple

-

Samsung

-

Advance Auto Parts

-

Ferguson

-

Carrier

-

Uline

-

Quill

-

Office Depot

-

AED USA

-

Cardinal Health

-

CareWell

That makes the product more practical.

Instead of being locked into random net-30 vendors that only sell office supplies, Credit Key may let you finance real business purchases from brands your business may already use.

Example: HVAC or Contractor Business

Let’s say you run a small HVAC or handyman business.

A commercial client calls because an AC unit is down. You need parts, tools, refrigerant, and supplies before you can finish the job.

Without business credit, you might have to swipe a personal credit card, drain cash, or wait until the customer pays a deposit.

With Credit Key, if your supplier is part of the network, you may be able to get the parts now, complete the job, invoice the client, and pay Credit Key when the money comes in.

That is the kind of situation where net-30 business credit can actually make sense.

It helps bridge the gap between buying materials and collecting revenue.

Example: E-Commerce Business

Now let’s say you run an e-commerce business.

Your product starts taking off. Orders spike. Inventory starts moving fast. But your payout from Amazon or another platform is still weeks away.

That creates a cash flow problem.

You need packaging, labels, shipping supplies, or replacement inventory now, not after the payout clears.

If you can use Credit Key with suppliers like Uline, Quill, or Office Depot, you may be able to keep operations moving without immediately draining cash.

That is where short-term business credit can protect momentum.

Example: Medical or Aesthetics Business

Credit Key may also be useful for certain medical, wellness, or aesthetics businesses.

Let’s say you run a med spa or small practice, and clients keep asking for a new service.

You find a device or equipment upgrade that could generate revenue, but paying cash upfront would hurt.

If the supplier accepts Credit Key, you may be able to acquire the equipment, launch the service sooner, and use the new revenue to help repay the balance.

That is the right way to think about business credit.

Not as free money.

As a tool to buy something that can help the business produce more revenue.

Who Credit Key Is Best For

Credit Key may be a good fit if your business has real revenue and needs short-term purchasing power.

It may work well for:

-

Contractors

-

HVAC businesses

-

Handyman businesses

-

E-commerce businesses

-

Medical offices

-

Med spas

-

Service businesses

-

Businesses that buy supplies or equipment

-

Businesses that need net-30 terms

-

Owners trying to build business credit with D&B

It is especially interesting if you want to avoid hard pulls while still testing business credit approval.

Who Should Avoid Credit Key?

Credit Key is not for everyone.

You should be careful if:

-

Your business has unstable cash flow

-

You cannot repay purchases within 30 days

-

You do not understand the monthly fees

-

You are only applying because it is soft pull

-

You are not comfortable with a personal guarantee

-

You do not have real business expenses to finance

-

You are using credit to cover losses instead of growth

A soft pull does not make bad debt safe.

If the purchase does not help the business generate revenue, save money, or solve a real cash flow timing issue, think twice before financing it.

What to Do Before Applying for Credit Key

Before applying, I would do a few things.

First, check your Equifax status.

If your Equifax report is frozen, you may need to temporarily unfreeze it before Credit Key can process the soft pull.

Second, know your real business revenue.

Credit Key may ask for annual revenue, and if you want a higher limit, they may request business bank statements.

Third, understand the PG.

If you are a small business, assume you may need to personally guarantee the account unless Credit Key clearly says otherwise.

Fourth, know how you will use it.

Do not apply just to apply. Have a real business purpose.

Frequently Asked Questions

Does Credit Key do a hard pull?

Based on my experience, Credit Key did not do a hard pull. It used a soft pull from Equifax. However, policies can change, so always read the application language before submitting.

What credit score do you need for Credit Key?

The original content states that Credit Key has a 600 FICO minimum. Approval still depends on your business revenue, business profile, and underwriting.

Does Credit Key require a personal guarantee?

Most small business owners should expect a personal guarantee. The original content says some larger businesses, such as businesses doing $5 million or more in annual revenue or those under an Enterprise classification, may have no-PG possibilities.

How much can Credit Key approve you for?

Credit Key instant approvals may range from $1,000 to $50,000. I was initially approved for $5,000, then increased to $7,500 overnight after submitting 3 months of business bank statements.

Does Credit Key report to Dun & Bradstreet?

The original content says Credit Key reports to Dun & Bradstreet and may report within the first 60 days. Positive payment history can help business credit, while negative history can hurt it.

Can you use Credit Key anywhere?

A portion of your Credit Key limit may be unlocked for universal spend through a virtual or physical Mastercard. The rest of the line may be usable through Credit Key’s partner vendor marketplace.

Conclusion

Credit Key surprised me.

I went into it expecting another limited vendor account, but the soft pull approval, fast underwriting, Mastercard access, D&B reporting, and overnight limit increase made it more useful than I expected.

My approval started at $5,000 with no hard pull, then moved to $7,500 after I submitted bank statements.

That is not life-changing funding, but it is a real business credit line that can help with short-term purchases, vendor expenses, and business credit building.

Just do not ignore the fine print.

Most small business owners should expect a personal guarantee, extended repayment can come with monthly fees, and negative payment history can still hurt your business credit.

Used correctly, Credit Key can be a solid tool.

Used carelessly, it can become another expensive payment obligation.