Citi Is Killing the Custom Cash Card for New Applications

Jun 25, 2026

Citi is officially killing the Custom Cash card for new applications.

And for a lot of cashback users, this feels like watching another legendary rewards card bite the dust.

The Citi Custom Cash has been one of the easiest cashback cards to love because it does not require much strategy. You use it in your top eligible spending category, and the card automatically earns 5% cash back on that category each billing cycle, up to the monthly spending cap.

Simple.

Useful.

Dangerously easy to optimize.

And that may be exactly why Citi is closing the door to new applicants.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

This One Personally Hits Me

I’ve personally held two Citi Custom Cash cards for years.

One for dining.

One for gas.

I use both of them every month, and honestly, they have become two of those cards that basically never leave my wallet.

They’re easy. They’re reliable. And they earn 5% back in categories I actually spend money on in real life.

So when rumors first started floating around that Citi might shut the card down for new applicants, I did not fully believe it.

But now, based on internal-looking screenshots circulating online, this looks real.

What Citi Is Changing

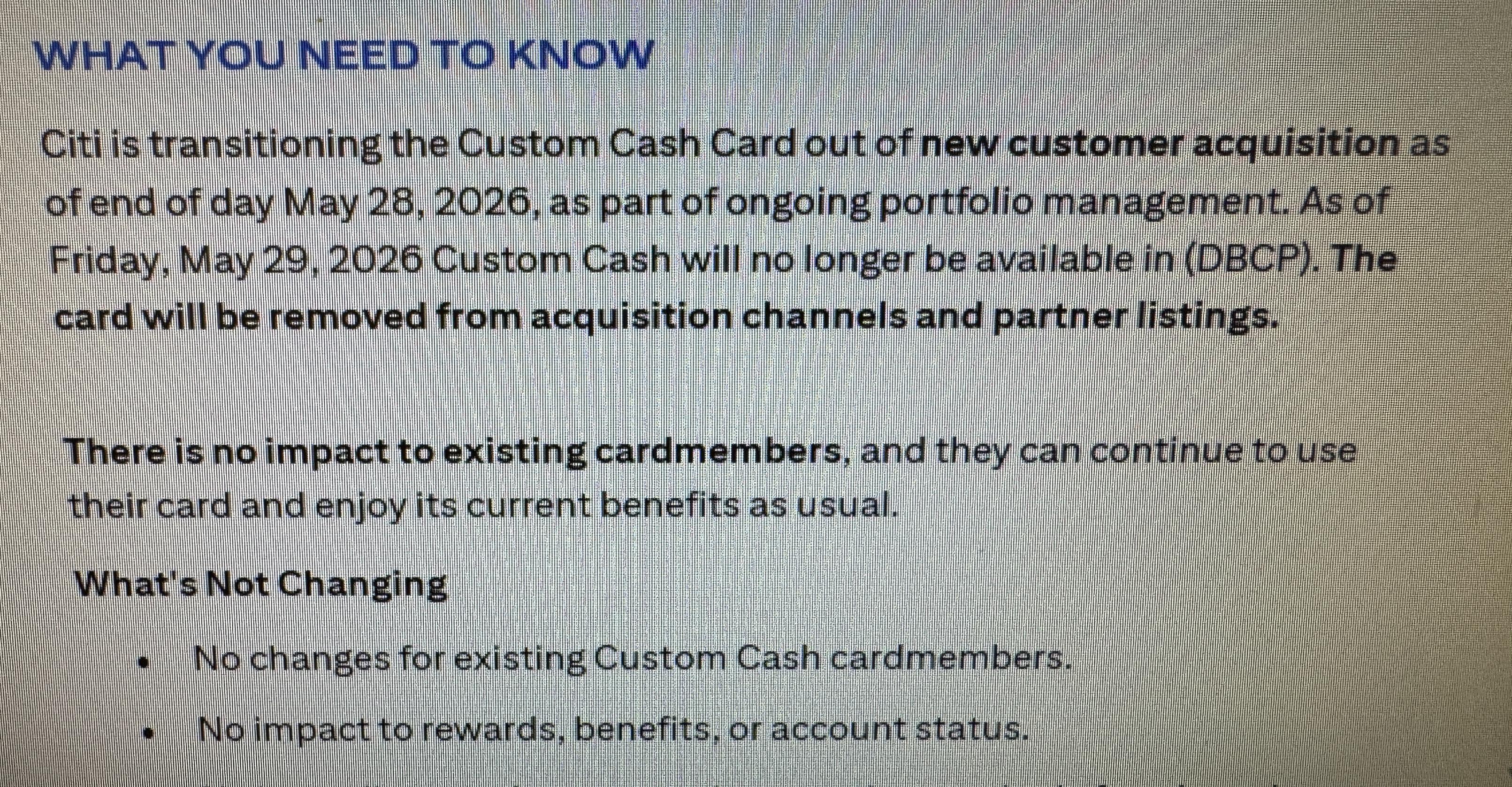

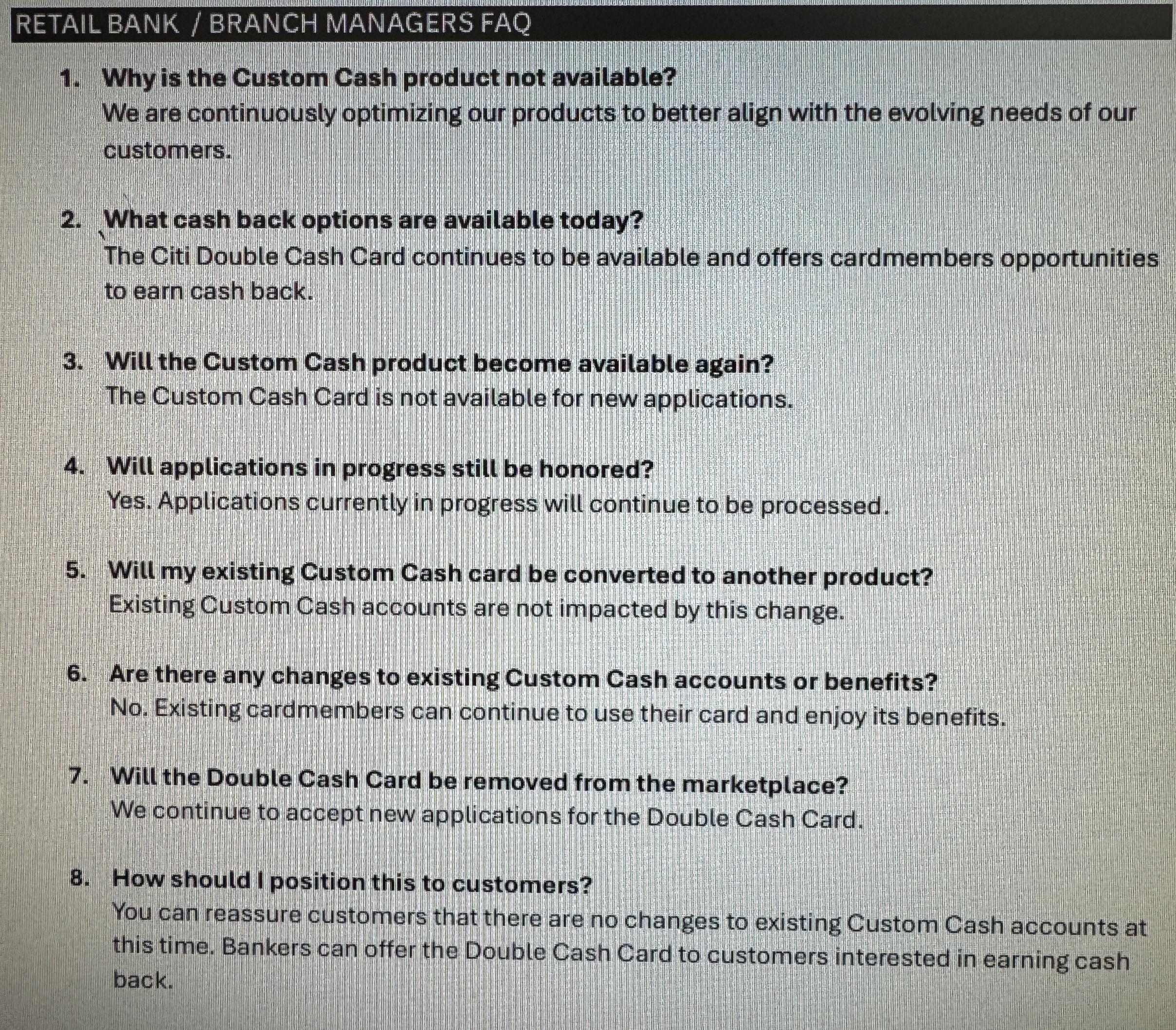

According to the screenshots, Citi is transitioning the Custom Cash card out of new customer acquisition as of end of day May 28, 2026.

The part that really stands out is this:

Citi says the card will be removed from acquisition channels and partner listings.

That wording sounds final.

Not paused.

Not temporarily unavailable.

Removed.

That sounds like Citi is closing the door on one of the best cashback cards it has ever released.

And when you see the standard corporate language about “optimizing products” and “evolving customer needs,” it feels like corporate code for something much simpler:

Too many people figured out how good this card was.

Existing Citi Custom Cash Cardholders Are Safe for Now

This is the part existing cardholders will care about most.

According to the information circulating, Citi is not changing existing Custom Cash accounts right now.

That means:

-

No changes for existing cardholders

-

No changes to rewards

-

No changes to account status

-

Existing users can keep using the card normally

That is a huge deal.

At first, people were worried about forced conversions, immediate reward changes, or accounts being moved into another Citi product.

But right now, this looks less like a complete shutdown and more like the Citi Custom Cash becoming a grandfathered card.

That puts it in the same general category as other cards people still talk about years later, like the Citi Prestige, Chase Ritz-Carlton, and old Chase Freedom cards.

Once they’re gone for new applicants, the people who already have them start treating them differently.

Why People Are Panic Applying

The internet reaction has been exactly what you would expect.

People are scrambling.

Some are submitting last-second applications before the May 28 deadline. Others are trying to product change older Citi cards into the Custom Cash while they still can.

And some people are trying to get a second, third, or even fourth Custom Cash card before the window closes.

One person summed it up perfectly:

“Panic applied and panic approved.”

That is basically the vibe right now.

The screenshots also say that applications currently in progress will continue to be processed, which makes the urgency feel even more real.

This is not just people overreacting. There really does appear to be a closing window.

Before rushing into any new credit card application, it is worth checking whether you are pre-approved first when possible so you can avoid unnecessary hard pulls.

Why the Citi Custom Cash Card May Have Been Too Good

I think this entire situation comes down to one simple issue.

The Citi Custom Cash became too optimized.

The card’s main appeal is simple: you automatically earn 5% cash back on your top eligible category each billing cycle, up to $500 per month in spending.

So instead of using it as a general everyday card, people started using it as a dedicated category card.

One Custom Cash for gas.

One Custom Cash for groceries.

One Custom Cash for dining.

One Custom Cash for home improvement stores.

One Custom Cash for transit.

And because Citi allowed product changes into the card for years, people figured out how to stack multiple Custom Cash cards together.

That is where the math probably started getting ugly for Citi.

Because the most optimized users are usually the least profitable users.

A lot of them:

-

Do not carry balances

-

Do not pay interest

-

Only use the card in 5% categories

-

Avoid spending on the card once they hit the cap

-

Use multiple Custom Cash cards to maximize rewards

One person joked that they never buy anything with their Custom Cash cards unless it earns 5%.

That line probably explains the entire problem.

Citi Seems to Be Steering People Toward Double Cash

Another important detail from the screenshots is that Citi repeatedly references the Double Cash card as the alternative.

That says a lot.

From Citi’s perspective, a 2% cash back card is much safer than people squeezing maximum value out of multiple 5% cards.

The Double Cash is still a useful card, but it is not the same type of weapon for cashback optimizers.

The Custom Cash gave people an easy way to earn elevated rewards without tracking rotating categories or activating quarterly bonuses.

That made it powerful.

Maybe too powerful.

This Looks Like Part of a Bigger Rewards Trend

This story is bigger than one credit card.

I think this is another sign that the easy rewards era is slowly changing.

Over the last few years, we have watched banks pull back in different ways:

-

Rewards getting nerfed

-

Loopholes disappearing

-

Cashback programs tightening up

-

Banks becoming more cautious about profitability

-

Popular cards getting removed from new applications

Once Reddit, YouTube, TikTok, and blogs teach millions of people how to optimize a card perfectly, the banks eventually adapt.

The Citi Custom Cash may just be the latest casualty.

And that is why I always tell people the same thing:

When you find a genuinely great financial product, do not assume it will be around forever.

Some of the best cards in history are already gone.

Now the Citi Custom Cash may officially be joining that list.

What This Means for Cashback Users

If you already have the Citi Custom Cash, this card just became more valuable.

Not because the rewards changed, but because access changed.

When a strong card closes to new applicants, existing cardholders usually start treating it like something they need to protect.

That means you may want to think carefully before closing it, product changing it, or letting it sit unused for too long.

If you do not have the card yet, the lesson is simple:

Great cashback cards do not stay available forever.

Banks can change products, close applications, remove cards from partner channels, or push customers toward safer alternatives whenever they want.

That does not mean you should apply for every card out of fear.

But it does mean you should pay attention when a card is genuinely useful for your real spending.

Final Thoughts

The Citi Custom Cash was one of the cleanest cashback cards on the market.

No rotating categories.

No complicated point strategy.

No guessing which category to choose.

You just used the card where you spent the most, and Citi handled the rest.

That simplicity is what made the card so good.

And honestly, it may also be what made the card a problem for Citi.

For existing cardholders, this is probably a card worth holding onto.

For everyone else, this is another reminder that great rewards cards can disappear faster than people expect.

The banks are watching how people use these products.

And when too many people figure out how to win, the rules usually change.