10 Credit Cards That May Show Your Limit Before You Accept

Jun 30, 2026

I found 10 credit cards that may show you your credit limit before you accept the offer.

That matters.

Because one of the worst feelings in credit is taking a hard pull, getting approved, and then realizing the bank gave you a tiny limit you never would have accepted if you saw it upfront.

A $300 approval is still an approval.

But let’s be real.

Sometimes it feels more like an insult with a hard inquiry attached.

That is why cards that show you the offer first can be useful.

You get to see the numbers.

Then you decide whether the card is worth it.

Quick Answer

Some Bread Financial and Comenity-issued cards may let you prequalify first and see a credit limit before accepting the offer. This can help you avoid blindly applying for a card that gives you a low limit. These cards are not always premium cards, and many are store cards, but they can be useful “bridge cards” if you need to build available credit, reduce utilization, or get a quick win while working toward stronger cards later.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you want to compare more soft-pull options before applying, my Free Credit Card & Loan Pre-Approval Master List can help you research cards that may let you check offers before risking a hard inquiry.

Why Seeing Your Limit First Matters

Most credit card applications feel backwards.

You apply first.

You take the risk first.

Then the bank tells you what you got.

That might be fine if the approval is strong.

But if the card comes back with a tiny limit, you are stuck wondering whether the hard pull was even worth it.

That is why “see your limit first” cards are interesting.

They can help you answer the most important question before fully committing:

Is this card actually worth adding to my profile?

Because approval alone is not the goal.

A useful approval is the goal.

The 10 Cards to Research

Here are the 10 cards from this data point:

-

myAcademy Rewards Mastercard

-

Midas Credit Card

-

B&H Payboo Credit Card

-

Big O Tires and Service Credit Card

-

Michaels Credit Card

-

All Pet Credit Card

-

Alphaeon Cosmetic Credit Card

-

Ford Rewards Visa Signature Credit Card

-

Nest Credit Card

-

Saks Fifth Avenue Mastercard

The most important thing to understand is that these cards are tied to Bread Financial, which used to be more commonly known through the Comenity name.

Some of these cards are open-loop cards, meaning they may run on a major network like Mastercard or Visa and can be used more broadly.

Others are store cards, meaning they may only work with that specific retailer or brand.

That difference matters a lot.

Do not assume every card on this list works everywhere.

The Catch: They Are Bread Financial Cards

Here is the catch.

These cards are issued through the Bread Financial and Comenity ecosystem.

And I already know what some of you are thinking:

“Wait, isn’t that kind of like Synchrony?”

Yeah.

Similar lane.

Similar reputation in some ways.

Bread/Comenity and Synchrony both issue a lot of retail and store cards.

And people complain about the same types of issues:

-

Customer service problems

-

Random credit limit cuts

-

Account closures

-

Store-card-heavy portfolios

-

Lower prestige than major bank cards

-

Cards that may not grow the way premium cards grow

So I am not saying these are amazing cards.

I am saying they can solve a very specific problem.

They may help you see your credit limit before accepting, which can keep you from wasting a hard pull on a card that does not help you.

That is the angle.

How These Cards Can Fit

These cards can make sense if you want to:

-

Prequalify first

-

See the limit before accepting

-

Avoid applying completely blind

-

Build more available credit

-

Lower reported utilization

-

Thicken your credit profile

-

Get a quick positive approval

-

Use a store card at a place you actually shop

That is the key.

If the card solves a real problem, it may have a place.

If it does not, skip it.

Do not collect store cards just because they are available.

A card needs a job.

My Quick Data Points

I tested a couple of these myself.

I got:

-

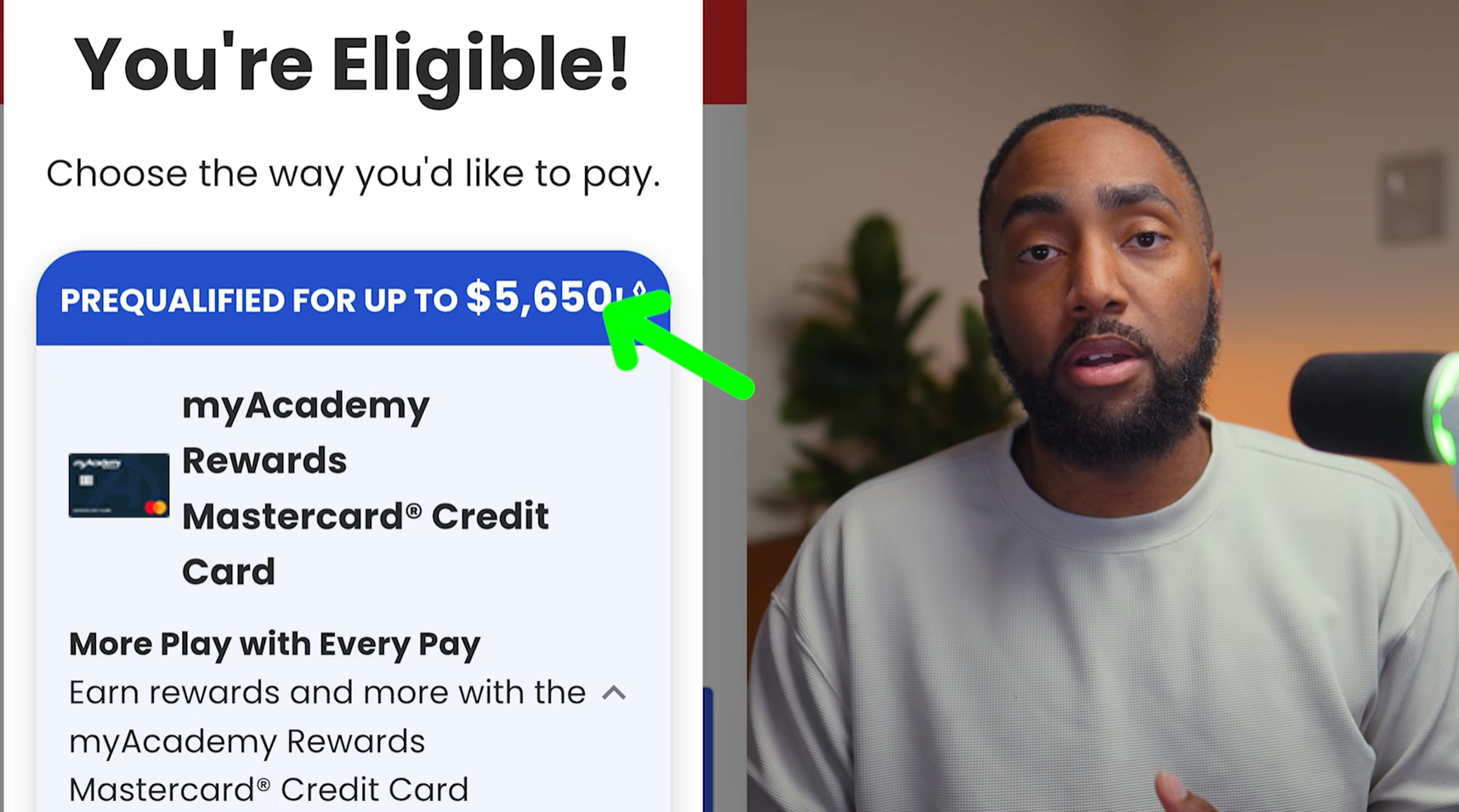

$5,650 on the myAcademy Rewards Mastercard

-

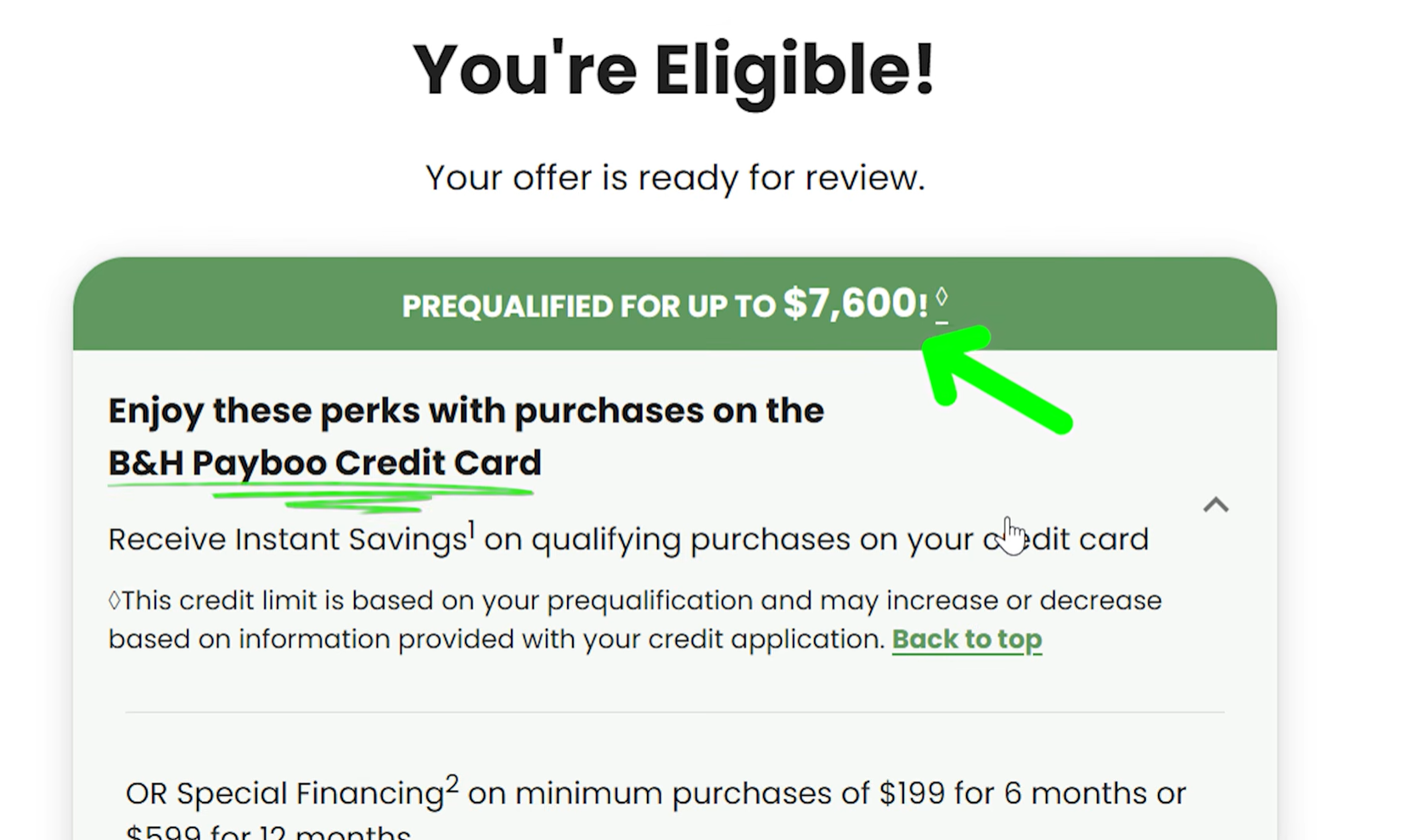

$7,600 on the B&H Payboo Credit Card

Those are real available credit lines.

And the important part is that I was not guessing blindly.

I could see the offer and decide whether it made sense.

That is powerful.

Not because these are the best cards on earth.

They are not.

But because seeing the number first changes the whole decision.

Why the myAcademy Rewards Mastercard Is Interesting

The myAcademy Rewards setup is interesting because Academy says applicants are first considered for the myAcademy Rewards Mastercard.

If they are not eligible, they may then be considered for the myAcademy Rewards Credit Card, which is the store-only version.

That matters because the Mastercard version can be used more broadly, while the store-only version is more limited.

Academy also says checking whether you prequalify will not affect your credit score, but proceeding with an application will result in a hard inquiry.

So this is not “no hard pull forever.”

It is more like:

Check first.

Review the offer.

Then decide whether moving forward is worth it.

That is exactly how more applications should work.

Why the B&H Payboo Card Is Different

The B&H Payboo Credit Card is more niche.

It is built for people who shop at B&H Photo.

That means it can make sense for photographers, creators, camera buyers, computer buyers, and people buying electronics or gear.

But if you never shop at B&H, it may not make sense.

This is where people mess up with store cards.

They see a credit limit and get excited.

But then they realize the card does not fit their spending.

Do not do that.

If the card is closed-loop or brand-specific, make sure you actually use that brand.

A limit is only useful if the card has a real purpose.

Let’s Be Real About Store Cards

Most of these cards are store cards or retail-connected cards.

And no, they are usually not the cards people flex.

Banks may not view them the same way as premium travel cards from Chase, Amex, Citi, or Capital One.

But that does not mean they are useless.

Store cards can still help certain people.

Especially if you are in this position:

-

Your score is stuck in the 600s

-

Your limits are low

-

Your utilization is high

-

You keep getting denied by big banks

-

You shop at one of these stores anyway

-

You need more available credit

-

You need a quick positive account

-

You want to see the limit before accepting

If that is you, a store card can be a tool.

Not the endgame.

A tool.

Think of These as Bridge Cards

The right way to think about these cards is simple:

Bridge cards.

You are not trying to build your final wallet around them.

You are using them to get from one stage to the next.

A bridge card can help you:

-

Build payment history

-

Add available credit

-

Lower utilization

-

Thicken your credit profile

-

Create a positive approval data point

-

Prepare for better cards later

That is the role.

Use the card responsibly.

Keep utilization low.

Pay on time.

Do not carry unnecessary balances.

Then, once your profile improves, move toward better cards.

Who These Cards May Be Best For

These cards may make sense for people who want more visibility before applying.

They may be useful if:

-

You are rebuilding

-

You have low limits

-

You want to reduce utilization

-

You want to avoid blind applications

-

You are trying to build confidence after denials

-

You already shop at one of the retailers

-

You want a card that may show the limit first

-

You understand the card is not your final destination

For someone rebuilding or trying to escape tiny limits, seeing a $3,000, $5,000, or $7,000 offer upfront can be a big deal.

But only if the card fits the plan.

Who Should Probably Skip Them

These cards are not for everyone.

You may want to skip them if:

-

You already have strong major-bank cards

-

You do not shop at the retailer

-

You are trying to avoid store cards

-

You are close to a mortgage application

-

You are chasing premium travel rewards

-

You already have too many new accounts

-

You do not want to deal with Bread/Comenity

-

You only want cards from major banks

There is nothing wrong with passing.

A card can be useful for one person and pointless for another.

That is why context matters.

Do These Cards Pull Experian?

The data points around these Bread/Comenity cards often point to Experian.

That said, bureau pulls can vary.

Issuer, state, product, profile, timing, and application path can all matter.

So do not apply assuming Experian is guaranteed.

Treat Experian as a common data point, not a permanent rule.

If a hard pull matters to you, freeze reports you do not want accessed only if you understand the risk.

A frozen report can stop the application, cause a denial, or require an unfreeze.

Prequalification Is Not Final Approval

This is important.

Prequalification is helpful, but it is not the same as final approval.

Bread/Comenity prequalification language can vary by card, but generally, prequalification is not a guarantee of credit.

That means the issuer may still verify information, review your full application, or deny you after the prequalification stage.

So do not treat the prequal screen like money already in your wallet.

Use it as a decision tool.

If the offer is strong, you can decide whether to move forward.

If the offer is weak, you can walk away before taking the next step.

The Right Way to Use These Cards

Here is how I would approach these cards.

First, check prequalification where available.

Second, look at the limit.

Third, look at whether the card is open-loop or store-only.

Fourth, decide whether you would actually use the card.

Fifth, check whether moving forward creates a hard pull.

Sixth, only accept if the card helps your bigger credit strategy.

Do not get blinded by the limit.

A $7,000 store card you never use may not be better than a $3,000 card that actually fits your life.

What to Watch Out For

Before accepting any offer, watch for:

-

Annual fees

-

Deferred interest promotions

-

High APRs

-

Store-only restrictions

-

Limited redemption options

-

Low usefulness outside one retailer

-

Credit limit decrease risk

-

Account closure risk

-

Hard inquiry language

-

Whether the card reports to all three bureaus

Store cards can be useful.

But they can also get people into trouble if they use them carelessly.

Especially with deferred interest.

Deferred interest is not the same as 0% APR.

If you do not pay the balance in full by the deadline, interest can come back and hit hard.

Read the terms.

Do Not Carry Balances Just to Build Credit

This part matters.

If you use one of these cards as a bridge card, do not use it as an excuse to carry debt.

You do not need to pay interest to build credit.

Use the card lightly.

Let a small balance report if needed.

Pay in full.

Keep utilization low.

That is the play.

These cards can help your available credit, but they can also hurt you if you run them up.

A higher limit only helps if you manage it correctly.

Frequently Asked Questions

What cards may show your credit limit before you accept?

Some Bread Financial and Comenity-issued cards may show your credit limit during the prequalification process before you accept. The list in this article includes myAcademy Rewards Mastercard, B&H Payboo, Midas, Big O Tires, Michaels, All Pet, Alphaeon, Ford Rewards Visa Signature, Nest, and Saks Fifth Avenue Mastercard.

Does prequalification hurt your credit score?

Prequalification usually uses a soft pull and should not affect your credit score. But if you proceed with a full application after seeing the offer, the issuer may perform a hard inquiry.

Are Bread Financial and Comenity the same?

Bread Financial is the company behind many credit card and payment products, and Comenity Bank/Comenity Capital Bank issue many of the retail cards connected to Bread Financial. Many people still refer to these cards as Comenity cards.

Are these cards good credit cards?

They can be useful for a specific purpose, but they are not always amazing long-term cards. Many are store cards or retail-connected cards. They may work best as bridge cards for building limits, lowering utilization, or getting a positive approval before moving to stronger cards later.

Do these cards pull Experian?

Many Bread/Comenity data points suggest Experian is commonly pulled, but bureau pulls can vary by product, state, application path, and profile. Do not treat Experian as guaranteed.

Should I apply for store cards to build credit?

Maybe, but only if the card fits your plan. A store card can help with available credit and payment history, but it can also add a new account, hard inquiry, high APR, and limited usefulness. Use prequalification first when possible.

Conclusion

These 10 cards are not magic.

And they are not all cards I would call amazing.

But they solve a real problem:

They may let you see your credit limit before you accept.

That is valuable.

Because credit card applications should not feel like a mystery box.

You should not have to take a hard pull just to find out the bank only trusts you with $300.

If you are rebuilding, stuck with low limits, fighting high utilization, or trying to get a quick win, these Bread/Comenity cards may be worth researching.

Just use them for the right reason.

Treat them like bridge cards.

Pay in full.

Keep utilization low.

Avoid unnecessary debt.

Then use the stronger profile to go after better cards later.