Capital One and Synchrony Account Closures: What Cardholders Need to Watch

Jun 26, 2026

Imagine logging into your credit card account and seeing your available credit drop to zero.

No warning.

No heads-up.

Just a closed account.

Now, to be clear, almost any bank can close a credit card account. That is not unique to one issuer.

But after reviewing dozens of real-world account closure reports, two names kept showing up more than others:

Capital One and Synchrony.

And the scary part is that many of these closures did not happen randomly.

There were patterns.

Returned payments.

High usage.

Fraud concerns.

Too much credit exposure.

Sudden changes in account behavior.

If you have cards with either of these banks, this is worth paying attention to.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Capital One and Synchrony appeared frequently in the account closure reports I reviewed. With Capital One, returned payments showed up as the biggest recurring issue, while Synchrony appeared especially sensitive to high usage, large balances, and overall credit exposure across multiple cards. These patterns do not guarantee your account will be closed, but they are warning signs cardholders should take seriously.

Why Banks Close Credit Card Accounts

A lot of people do not realize this, but credit card issuers generally have the right to close accounts.

That does not mean they can ignore legal notice requirements.

But it does mean that your credit card account is not guaranteed to stay open forever.

Banks constantly review risk.

And when they want to reduce risk, they may:

-

Close accounts

-

Lower credit limits

-

Tighten approvals

-

Reduce exposure to certain customers

-

Review accounts with unusual activity

-

Pull back during uncertain economic periods

This tends to happen more when banks are getting nervous.

And there are a few big reasons that can happen.

Economic Uncertainty Can Make Banks More Conservative

When the economy gets weaker, more consumers start struggling with payments.

Credit card balances can rise.

Delinquencies can rise.

Minimum payments become harder for some people to manage.

When that happens, banks may start looking more carefully at which customers they want to keep lending to.

That does not always mean they immediately close accounts.

But it can make them more conservative.

And when banks get conservative, customers with risk signals may get reviewed more closely.

Higher Interest Rates Can Add More Pressure

Higher interest rates can also change how banks look at risk.

When borrowing gets more expensive, carrying credit card balances becomes more dangerous for consumers.

A customer who seemed fine before may start looking riskier if balances are rising and monthly payments are getting harder to manage.

Banks know this.

So during higher-rate environments, lenders may become more cautious about extending credit or keeping large unused credit lines open.

Lending Standards Can Tighten Fast

Banks do not keep the same risk appetite forever.

They adjust.

Sometimes they get aggressive and approve more people.

Other times they pull back.

That can lead to:

-

More denials

-

Smaller starting limits

-

Credit limit decreases

-

Account reviews

-

Account closures

And sometimes the customer does not feel like anything changed.

But from the bank’s perspective, the risk model changed.

That is why people can wake up one day and feel completely blindsided by an account closure.

Capital One Account Closures: The Patterns I Found

Capital One appeared frequently in the account closure reports I reviewed.

Among the major national banks, it stood out.

The three biggest themes were:

-

High usage

-

Fraud concerns

-

Returned payments

Returned payments were the biggest issue by far.

Helpful resource: Before applying for new cards blindly and risking unnecessary hard inquiries, my Free Credit Card & Loan Pre-Approval Master List can help you find cards that may let you check your odds before applying: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Capital One Closure Reason #3: High Usage

Around 10% of the Capital One closures I reviewed involved unusually high credit usage.

High usage usually means using a large percentage of your available credit limit, especially if those balances report to the credit bureaus.

But it is not always just about carrying a balance.

Sometimes sudden large spending can also attract attention.

In one case, a cardholder reportedly charged more than $40,000 across two Capital One cards for luxury purchases and travel.

The balances were reportedly paid off immediately.

But both accounts were later closed.

That is important.

Because even if you pay the balance, sudden spending that looks very different from your normal account behavior can still trigger scrutiny.

From the bank’s perspective, a sudden jump in activity can look risky.

Especially if it happens across multiple accounts.

High usage does not guarantee your account will be closed.

But it did show up as a recurring factor in the cases I reviewed.

Capital One Closure Reason #2: Fraud Concerns

Around 20% of the Capital One closures I reviewed involved fraud concerns or account activity that may have triggered fraud-related review.

And fraud concerns do not always mean someone stole your card.

Banks also monitor for behavior that looks unusual.

That can include:

-

Sudden spending spikes

-

Unusual purchase locations

-

Multiple new authorized users

-

Activity that does not match your normal pattern

-

Rapid changes in account behavior

In one reported case, a cardholder had maintained an account for roughly eight years with an excellent payment history.

Then a few months before the closure, two relatives were added as authorized users.

Shortly afterward, the account was shut down.

Capital One reportedly cited activity that was inconsistent with its expectations for account usage.

Now, it is impossible to know exactly what triggered that closure.

But the timing matters.

One of the biggest lessons from account closure cases is this:

Look at what changed shortly before the shutdown.

A lot of the time, the trigger is not something that had been happening for years.

It is something that recently changed.

Capital One Closure Reason #1: Returned Payments

The biggest Capital One pattern was returned payments.

Around 70% of the Capital One closures I reviewed involved one or more returned payments.

That is a huge signal.

A returned payment happens when a credit card payment is submitted but fails to clear.

This can happen because of:

-

Insufficient funds

-

Incorrect bank account information

-

Closed or old bank accounts

-

Failed transfers between accounts

-

Autopay pulling from the wrong account

-

Timing issues with deposits or transfers

In one case, a cardholder reported that two payments were returned because funds had not been moved between accounts in time.

The account was later closed.

In another case, a cardholder reported that a single returned payment was followed by an account shutdown, even though they had an otherwise clean payment history.

The theme was hard to ignore.

Capital One appeared highly sensitive to returned payments in the cases I reviewed.

And from the bank’s perspective, that makes sense.

A returned payment can signal cash flow problems, payment risk, or unreliable repayment behavior.

Even if it was an honest mistake.

That is why I would treat returned payments as one of the biggest things to avoid with Capital One.

How to Reduce Capital One Shutdown Risk

If you have Capital One cards, I would be extra careful with payment reliability.

A few simple habits can help reduce risk:

-

Double-check your linked payment account

-

Make sure old checking accounts are removed

-

Confirm autopay is pulling from the right place

-

Keep enough money in the account before payment day

-

Check that payments actually post

-

Avoid sudden spending spikes that look unusual

-

Be careful adding multiple authorized users at once

None of this guarantees your account stays open.

But if returned payments are showing up repeatedly in closure reports, I would not play around with that.

Especially with Capital One.

Synchrony Account Closures: The Patterns I Found

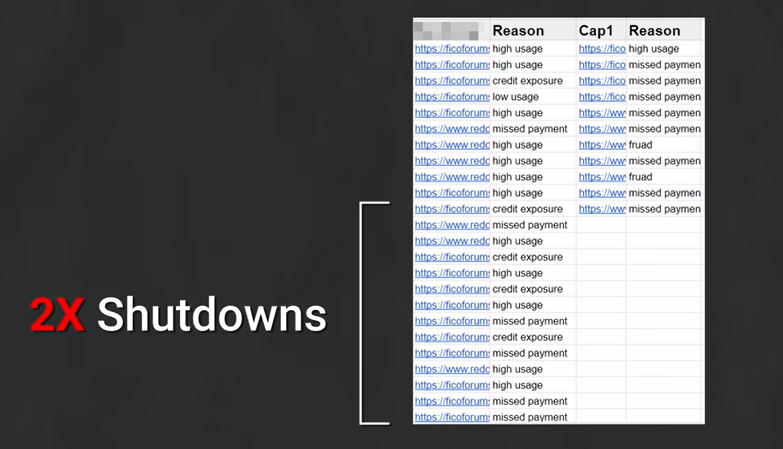

Synchrony stood out even more than Capital One in the reports I reviewed.

Out of 34 account closure cases reviewed, 22 involved Synchrony.

That caught my attention because Synchrony is much smaller than Capital One.

Three common themes kept showing up:

-

Returned payments

-

Credit exposure

-

High usage

And with Synchrony, high usage appeared to be the biggest issue.

Synchrony Closure Reason #3: Returned Payments

Around 20% of the Synchrony closures I reviewed involved returned payments.

Again, a returned payment means the payment was started but never successfully cleared.

In one reported case, a cardholder said Synchrony closed their account after autopay attempted to pull funds from an old checking account that was still linked to the card.

The cardholder later made payments manually.

But the original payment attempts had already failed.

That is the key lesson.

Initiating a payment and successfully completing a payment are not the same thing.

A lot of people assume the payment is handled once they click submit.

But if the funds do not clear, the bank sees a returned payment.

That can create a serious problem.

If you pay Synchrony manually or through autopay, it is worth checking a few days later to make sure the payment actually posted.

Synchrony Closure Reason #2: Credit Exposure

Around 24% of the Synchrony closures I reviewed appeared to involve excessive credit exposure.

To be clear, Synchrony did not necessarily say “credit exposure” in these cases.

But it was a recurring pattern.

Credit exposure means the total amount of credit a bank has extended to one customer.

For example, if someone has several Synchrony cards, each with large limits, Synchrony may eventually decide it has extended too much credit to that one person.

One cardholder reported:

-

A credit score around 750

-

Years of perfect payment history

-

Low overall utilization

-

Multiple Synchrony cards

-

Limits ranging from several thousand dollars to $20,000

Despite the strong profile, Synchrony reportedly closed nearly all of the accounts at the same time.

And this was not an isolated pattern.

Across several reports, widespread Synchrony closures often involved people with five or more Synchrony accounts open at the same time.

That suggests Synchrony may have internal limits around:

-

Total available credit

-

Number of accounts

-

Total exposure

-

Balances across accounts

-

Risk across the full relationship

Many major banks have internal exposure limits.

The difference with Synchrony is that some people seem to reach those limits after building up multiple large credit lines across different retail cards.

Why Synchrony Exposure Can Build Fast

One reason this matters is because Synchrony can be attractive to people chasing approvals and credit limit increases.

Synchrony is known for offering:

-

Easy pre-approvals

-

Store card approvals

-

Promotional financing

-

Frequent credit limit increases

-

Large credit lines across multiple products

That can feel like a good thing.

And sometimes it is.

But it can also cause your total exposure with Synchrony to build faster than you realize.

You may not think of your Synchrony cards as one relationship.

You may think:

“This is my furniture card.”

“This is my Amazon card.”

“This is my Lowe’s card.”

“This is my PayPal card.”

“This is my CareCredit account.”

But Synchrony may look at the entire relationship.

That is the part people miss.

Synchrony Closure Reason #1: High Usage

The most common Synchrony pattern I found was high usage.

Around 52% of the Synchrony closures I reviewed involved elevated balances or heavy usage.

Several cardholders described similar situations:

-

Financing furniture after buying a house

-

Using promotional 0% APR offers

-

Carrying large balances across multiple Synchrony cards

-

Running up balances after major life events

-

Sudden spending increases compared to normal account behavior

-

Heavy spending at one retailer

In one case, a cardholder reported furnishing an entire home using Synchrony financing.

The accounts were later closed despite payments being made on time.

In another case, a customer reported carrying elevated balances for several months before the shutdown happened.

In a third case, someone reported heavy spending at a retailer and earning substantial rewards before the account was closed.

The common theme was not missed payments.

The common theme was elevated risk from the bank’s perspective.

High balances.

Rapid spending increases.

Large exposure.

Multiple accounts with balances at the same time.

That is where Synchrony seems especially sensitive.

Why Promotional Financing Can Still Create Risk

This is the tricky part.

A lot of people use Synchrony cards for promotional financing.

That might be furniture.

Dental work.

Retail purchases.

Home improvement.

Electronics.

Medical expenses.

And the whole point of a promotional financing offer is to carry the balance during the promo period.

So it feels normal.

But from the bank’s perspective, a large balance is still a large balance.

Especially if it happens across multiple Synchrony accounts at once.

That does not mean you should never use a promotional offer.

But if you are carrying high balances across several Synchrony cards at the same time, I would be careful.

The fact that a balance is promotional does not mean the bank ignores the risk.

What If Synchrony Closes Your Account?

The good news is that a Synchrony closure does not necessarily mean you are permanently blacklisted.

Several reports showed cardholders eventually getting approved again after some time.

But getting the closed account reopened immediately seemed far less common.

In most cases, once the account was closed, the decision appeared final.

That does not mean the relationship is over forever.

Some cardholders reported getting approved for new Synchrony accounts months or years later after improving their profile and reducing the issues that likely caused the closure.

If Synchrony closes your account, one possible strategy is to wait 60 to 90 days, fix whatever likely triggered the closure, and then see if future pre-approved offers become available.

Again, approvals are never guaranteed.

But some people do seem to rebuild with Synchrony over time.

How to Reduce Synchrony Shutdown Risk

If you have Synchrony cards, the big thing I would watch is concentration.

Do not just think about one card.

Think about your full Synchrony relationship.

That means watching:

-

Total number of Synchrony accounts

-

Total credit limits across Synchrony

-

Total balances across Synchrony

-

Promotional financing balances

-

Returned payments

-

Sudden spending spikes

-

High utilization on multiple Synchrony cards at the same time

If you have one Synchrony card with a reasonable balance, that is one thing.

If you have six Synchrony cards, several large limits, multiple promo balances, and recent heavy usage, that is a different risk profile.

That is the difference a lot of people miss.

The Two Biggest Lessons

After reviewing these shutdown reports, the two biggest lessons are simple.

First, avoid returned payments at all costs.

Second, be careful with high balances and heavy usage, especially across multiple accounts with the same issuer.

Capital One seemed especially sensitive to returned payments.

Synchrony seemed especially sensitive to high usage and total exposure.

Neither bank publicly discloses every factor that goes into account closures.

So nobody can say exactly what will or will not trigger a shutdown.

But when the same patterns show up across dozens of reports, I pay attention.

And you should too.

Frequently Asked Questions

Can Capital One close my credit card account without warning?

Capital One, like other credit card issuers, can close accounts based on its account terms and risk policies. The bank may still have notice requirements, but cardholders should understand that credit card accounts are not guaranteed to remain open forever.

What is the biggest Capital One account closure risk?

In the cases reviewed, returned payments were the most common Capital One account closure pattern. That does not mean every returned payment will lead to closure, but it is a risk signal cardholders should avoid.

Why does Synchrony close credit card accounts?

In the cases reviewed, Synchrony closures often involved high usage, elevated balances, multiple Synchrony accounts, returned payments, or what appeared to be too much credit exposure across the relationship.

Is high credit utilization dangerous with Synchrony?

High utilization can be risky with any issuer, but Synchrony appeared especially sensitive to elevated balances and heavy usage across multiple accounts in the reports reviewed.

Can you get approved by Synchrony again after a closure?

Some reports showed cardholders getting approved by Synchrony again after time passed and their credit profile improved. But getting a closed account reopened immediately appeared less common.

How can I reduce my risk of a credit card shutdown?

Avoid returned payments, keep utilization under control, do not let old bank accounts stay linked to autopay, watch sudden spending spikes, and pay attention to your total exposure with each issuer.

Final Thoughts

Unexpected credit card closures can be frustrating.

Especially when you feel like you did everything right.

But banks are always watching risk.

And the patterns I saw with Capital One and Synchrony were hard to ignore.

With Capital One, returned payments seemed to matter a lot.

With Synchrony, high usage, elevated balances, and total credit exposure showed up again and again.

That does not mean you should panic if you have cards with these banks.

But it does mean you should be intentional.

Check your autopay.

Confirm your payments post.

Watch your utilization.

Be careful carrying large balances across multiple accounts.

And do not assume a bank will always be comfortable with the amount of credit it has extended to you.

Because sometimes the account closure does not come after years of bad behavior.

Sometimes it comes after one recent change that made the bank nervous.