How I Got My Capital One Credit Limit Increased to $39,000

Jun 29, 2026

I did not expect this one.

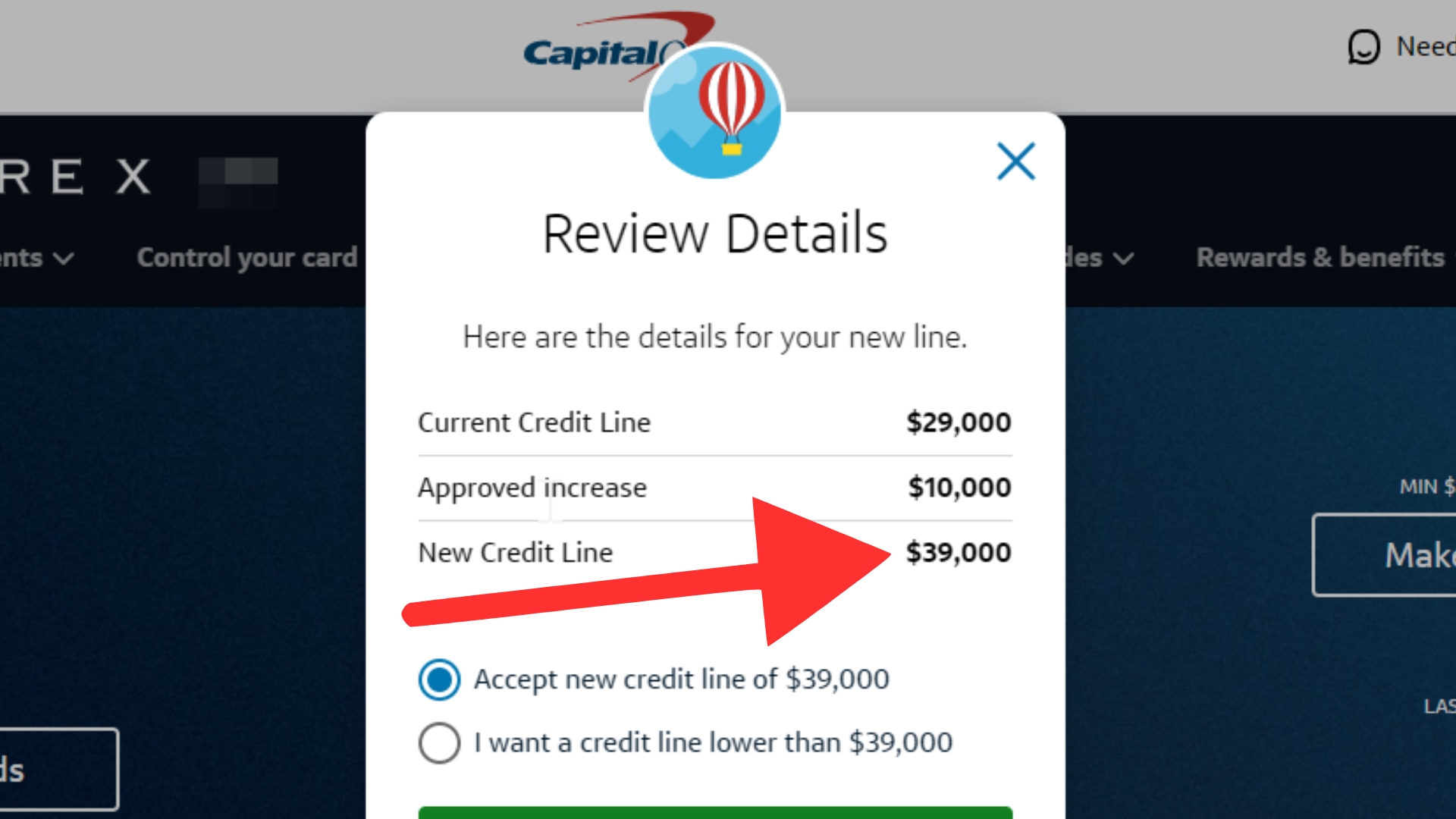

Capital One just increased my credit limit to $39,000.

That is a full $10,000 increase from my previous $29,000 limit.

And the funniest part?

I barely even use the card anymore.

For years, I used to get nothing but “7–10 business day” messages every time I requested a Capital One credit limit increase. If you’ve dealt with Capital One before, you already know that message usually feels like a polite denial.

But after testing for years, I finally figured out the pattern that worked for me.

I kept usage light. I requested increases consistently. I product changed from Quicksilver to Venture X. And before each request, I updated my household income.

Now I’ve had nine Capital One credit limit increases in six years, all without a hard pull.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

I grew my Capital One credit limit from $15,000 to $39,000 by starting with a strong approval bucket, product changing from Quicksilver to Venture X, keeping light but consistent usage on the card, manually requesting credit limit increases, and updating my household income before each request. My latest increase was a $10,000 jump from $29,000 to $39,000, even though my only recent recurring charge was about $140 per month. Capital One says credit limit increase reviews use soft inquiries, so they do not impact your credit score. Results can vary based on your card, credit profile, income, account history, usage, and Capital One’s internal rules. (Capital One)

Helpful resource: If you want to see which cards you may be pre-approved for before applying, my Free Credit Card & Loan Pre-Approval Master List can help you compare soft-pull pre-approval options before risking unnecessary hard pulls.

My Capital One Starting Point: A $15,000 Quicksilver Approval

Back in 2019, I was not chasing massive credit limits.

My FICO score was somewhere in the high 600s to low 700s. I applied for the Capital One Quicksilver card, and the approval screen came back with a $15,000 starting limit.

At the time, that was huge for me.

It was my highest credit limit ever, and it instantly changed how my credit profile looked.

Looking back, I believe I got placed into Capital One’s stronger approval bucket early. That matters because Capital One can be very bucket-driven. Some people get approved into lower-limit products or lower-growth accounts, and it can feel like they’re stuck forever.

I didn’t fully understand it at the time, but that $15,000 approval became the foundation for everything that came later.

I Had No Real Strategy at First

After getting the Quicksilver card, I basically shelved it.

I was chasing sign-up bonuses, trying different cards, and not thinking about Capital One as a long-term credit limit play.

Then in March 2022, I randomly clicked the “Request Credit Limit Increase” button.

Capital One approved me for a $1,000 increase, taking the card from $15,000 to $16,000.

Looking back, I think a small travel purchase around 90 days before the request may have helped wake up the account. It was not heavy spend. It was around $411.

Nothing crazy.

But it was enough activity to show Capital One I still used the card.

That was my first real clue.

Capital One was not going to just hand me more credit because time passed. I had to ask, test, and give their system enough activity to respond to.

My Capital One Credit Limit Increase Timeline

Here is the full timeline of how my Capital One limit grew from $15,000 to $39,000.

| Date | Card | New Limit | Notes |

|---|---|---|---|

| Jul 2019 | Quicksilver | $15,000 | Starting approval |

| Mar 2022 | Quicksilver | $16,000 | First manual CLI |

| Jul 2022 | Quicksilver → Venture X | $17,000 | Small jump before upgrade |

| Oct 2022 | Venture X | $18,000 | Testing pattern begins |

| Aug 2023 | Venture X | $23,000 | First major jump |

| Sep 2023 | Venture X | $24,000 | Back-to-back approval |

| Feb 2024 | Venture X | $25,000 | Steady rhythm |

| Jun 2024 | Venture X | $26,000 | Continued growth |

| Sep 2024 | Venture X | $29,000 | Multi-thousand jump |

| Oct 2025 | Venture X | $39,000 | Latest $10,000 increase |

That is nine increases and $24,000 in total growth.

And no, every request was not approved.

Not even close.

I got plenty of 7–10 business day messages along the way. But I treated every denial like a data point.

I looked at my usage. I looked at the timing. I looked at my income field. Then I adjusted and tried again.

That is how you learn the bank’s pattern.

The Latest $10,000 Increase

For the latest request, I filled out the form like this:

-

Monthly spend estimate: $10,000

-

Maximum desired line: $39,000

-

Reason for increase: “I expect higher expenses over the next few months.”

-

Employment status: Employed

-

Income: Household income, kept under the $300,000 mark

Now let me explain something important.

Even though I am self-employed, I listed myself as employed because I am employed by my own business. I also updated my household income before making the request.

The CFPB says card issuers can evaluate ability to pay based on individual income or, for applicants at least 21 with a spouse or partner, combined income or assets as part of a couple. That means household income can matter if it is income you reasonably have access to. (Consumer Financial Protection Bureau)

The wild part is that I barely use this card anymore.

The only recurring charge on it was my wife’s $140 monthly gym membership.

That is it.

No massive spend.

No $10,000 month.

No aggressive cycling.

Just one small recurring charge keeping the account alive.

So when Capital One instantly approved the increase to $39,000, I was surprised.

Strategy #1: Start in the Right Capital One Bucket

The biggest lesson is this:

How you enter Capital One matters.

If you start with a low-limit starter card, you may have a harder time growing that card into something massive.

That does not mean it is impossible.

But it can be harder.

Capital One has a reputation for serving both ends of the market. They have cards for people rebuilding credit, and they have premium cards for strong profiles.

The middle can feel weird.

When I got the Quicksilver at $15,000, I believe I avoided low-limit jail from the beginning. That gave me room to grow.

So if you are brand new to Capital One and your credit is not ready yet, you may want to think carefully before applying.

Sometimes the first approval sets the tone for the relationship.

Strategy #2: Product Change Up When It Makes Sense

The product change from Quicksilver to Venture X was a turning point.

It felt like getting promoted inside Capital One’s ecosystem.

The Quicksilver was fine, but Venture X is a premium travel card. It is a different product tier with a different type of customer profile.

After the upgrade, my increases started getting more interesting.

I went from small $1,000 moves to bigger jumps like $5,000 and eventually $10,000.

That does not mean everyone should product change to Venture X.

But if your card feels stuck, it may be worth checking whether Capital One gives you upgrade options.

Sometimes you do not need a new application.

You may just need to move the relationship you already have into a stronger product.

Capital One says cardholders can request a credit limit increase online or in the mobile app, and Capital One may consider factors like account history, income, employment status, monthly housing payment, and other credit factors. (Capital One)

Strategy #3: Use the Card Lightly but Consistently

This is where people get confused.

A lot of people think you need to run thousands of dollars through a card to get a credit limit increase.

That was not my experience.

Most of my increases came after spending less than $300 per month.

Some happened after almost no real activity besides a small recurring charge.

But this depends on your bucket.

If you are in a lower-tier or rebuilding bucket, Capital One may want to see more usage. You may need to make the card a top-of-wallet card for a while, use a good portion of the limit during the cycle, and pay it down before the statement closes.

But if you are already in a stronger bucket, the rules can feel different.

You may not need heavy spend.

You may just need consistent activity, clean reports, and enough income to support the larger line.

That is why I do not believe there is one Capital One strategy for everybody.

There are different strategies depending on where Capital One placed you.

Strategy #4: Request Credit Limit Increases Manually

Every Capital One increase I received came from me manually asking.

Automatic increases can happen, but I would not sit around waiting on them.

Capital One lets you request a credit limit increase through your account, and the company says its credit line increase reviews use soft inquiries that do not impact your credit score. (Capital One)

That is a big deal.

Because if the request is a soft pull, I am much more willing to test.

I made it a routine.

About every 30 days, usually after my statement cut, I would log in and request an increase.

Sometimes I got denied.

Sometimes I got approved.

And one time, I even got back-to-back increases in consecutive months.

Now, Capital One also says accounts that have been open only a few months are generally too new to be considered, and accounts with a recent credit line change may not be considered again right away. (Capital One)

So this is not guaranteed monthly approval.

But asking consistently helped me collect data and catch the approvals when Capital One’s system was ready.

Strategy #5: Update Household Income Before Requesting

This one is overlooked.

Before every credit limit increase request, I update my income.

Not just personal income.

Household income that I can reasonably count.

That matters because lenders do not only care about your credit score. They care about your ability to repay.

If your income has increased but your profile still shows old income, you may be leaving credit limit growth on the table.

Capital One’s credit limit increase process asks for information like annual income, employment status, and monthly rent or mortgage payment. (Capital One)

So yes, income matters.

But do not get reckless.

Do not make up numbers.

Do not inflate income you cannot explain.

I personally keep my stated household income believable and consistent. My general rule of thumb has been staying under the $300,000 mark, but that is my personal comfort zone.

Your number needs to match your real financial life.

Why Light Usage Worked for Me

The most surprising part of this whole journey is that light usage worked.

That goes against what a lot of people repeat online.

But here is what I think happened:

Capital One already trusted my profile.

The card had a strong limit from the beginning.

My credit reports were clean.

My utilization was controlled.

My income supported a larger line.

The account stayed active.

And I kept asking.

That combination mattered more than heavy spending.

If you are trying to grow a $500 or $1,000 Capital One limit, your experience may be different. Capital One may need to see more usage to justify giving you more credit.

But once you are in the higher-tier bucket, you may not need to force spending just to impress the algorithm.

Use the card enough to keep it alive.

Then ask.

The Capital One “7–10 Business Day” Denial Pattern

I got a lot of 7–10 business day messages over the years.

And yes, most of the time, that meant denial.

But those denials were useful.

They taught me what did not work.

Sometimes I requested too soon.

Sometimes usage was too low.

Sometimes the income field needed updating.

Sometimes Capital One simply was not ready to give me more.

The key is not to emotionally spiral every time you get denied.

A denial is data.

Track the timing. Track the usage. Track your reported income. Track your recent credit activity.

Then try again later if the request is still a soft pull.

That is how I went from repeated denials to a $39,000 limit.

The Credit Snowball Effect

Higher limits changed everything.

When my Capital One limit moved into the high $20Ks and $30Ks, I started seeing something I call the credit snowball effect.

One big limit helps attract more big limits.

Why?

Because other lenders can see that another bank trusts you with a large line.

That does not guarantee they will match it.

But it can help.

Higher limits can also lower your utilization if your balances stay the same. Capital One explains that a credit limit increase may help lower your credit utilization ratio if you do not increase your spending. (Capital One)

That is exactly the game.

More available credit.

Same or lower balances.

Cleaner utilization.

Stronger profile.

More approvals.

That is the snowball.

A $16,000 Real-World Test

Last year, I had to make a $16,000 payment to my general contractor during a home renovation.

That is the type of payment the old me would not have even imagined putting on one credit card.

I called Capital One first to make sure it would go through without issues.

The rep told me I was good to go.

And the payment cleared instantly.

That is the practical power of higher limits.

It is not just about bragging rights.

It is about flexibility.

When your limits are high enough, you can handle large expenses without instantly wrecking your utilization or triggering payment stress.

That does not mean you should overspend.

It means you have room to move.

Who This Strategy Works Best For

This Capital One credit limit increase strategy is best for people who already have a decent relationship with Capital One and a clean credit profile.

It may work well if:

-

Your Capital One card is at least several months old

-

You have no recent late payments

-

Your utilization is low

-

Your income supports a higher limit

-

You use the card at least occasionally

-

You update your income accurately

-

You request increases manually

-

You are already in a stronger Capital One bucket

It may be harder if:

-

Your card is very new

-

You recently got a limit change

-

You barely have credit history

-

Your score is weak

-

You are in a low-limit starter bucket

-

Your income does not support more credit

-

Your reports show recent delinquencies

-

Your utilization is high

Capital One can be unpredictable, but it is not random.

There is a pattern.

You just need to know which pattern applies to your profile.

What I Would Do If Capital One Keeps Saying No

If Capital One keeps denying you, I would not keep smashing the button emotionally.

I would look at the reason.

Then I would fix the profile.

Start with these questions:

-

Is the card too new?

-

Did you recently get an increase or decrease?

-

Are you using the card at all?

-

Is your reported income updated?

-

Is your utilization too high?

-

Are there recent late payments?

-

Are there too many new accounts?

-

Are you in a starter bucket with limited growth?

-

Would a product change help?

-

Would a different bank be a better fit?

That last one matters.

Sometimes the answer is not to fight Capital One forever.

Sometimes the smarter move is building with a bank that is more excited to work with you.

Helpful resource: If Capital One keeps telling you no, my 9 Credit Cards That Reveal Your Starting Limit Before Approval can help you find cards where you may be able to see your limit before fully committing.

Frequently Asked Questions

Does Capital One do a hard pull for credit limit increases?

Capital One says it uses soft inquiries to review credit limit increases, so requesting or receiving a Capital One credit limit increase does not impact your credit score. Always review the language in your own account before submitting because issuer processes can change. (Capital One)

How often can you request a Capital One credit limit increase?

I personally tested requests about every 30 days, usually after the statement cut. But Capital One says accounts that recently had a credit line change may not be considered again right away, and newer accounts may be too new to qualify. Your timing can vary. (Capital One)

Do you need heavy spending to get a Capital One credit limit increase?

Not always. My biggest lesson was that light usage worked for me once I was in a stronger Capital One bucket. I received increases after spending under $300 per month, and my latest $10,000 increase happened while the card only had a small recurring charge. But lower-tier or rebuilding profiles may need heavier responsible usage to show Capital One the limit is needed.

Should you update income before requesting a credit limit increase?

Yes, if your income has changed and you can accurately report it. Capital One asks for income and employment information during the credit limit increase process, and ability to repay matters in credit decisions. Do not inflate income you cannot reasonably support. (Capital One)

Can you include household income for a credit card limit increase?

If you are at least 21 and have reasonable access to household income or a spouse/partner’s income, issuers may consider ability to pay based on combined income or assets. The key is that the income needs to be reasonably accessible to you, not just a random number in the household. (Consumer Financial Protection Bureau)

Why does Capital One keep denying my credit limit increase?

Common reasons can include a new account, recent credit line change, low usage, high utilization, weak credit score, recent delinquencies, low income compared to the requested line, or being in a lower-limit bucket. A good internal link here would be a post like “Why You Were Denied Even With a Good Credit Score.”

Conclusion

I grew my Capital One limit from $15,000 to $39,000 because I stayed consistent.

I started with a strong approval.

I product changed up to Venture X.

I kept the card active without forcing heavy spend.

I requested increases manually.

I updated my household income before asking.

And I kept testing even after getting denied.

That is the real strategy.

Capital One can feel unpredictable, but my data points show there is a pattern if you pay attention.

You do not need perfect credit to start building higher limits. I didn’t start with perfect credit. But you do need patience, clean habits, accurate income, and enough consistency to let the algorithm trust you.

Because once one bank trusts you with a high limit, the whole credit game can start changing.