Capital One Cards Moving to Discover? Why Travelers Should Pay Attention

Jun 29, 2026

Capital One is quietly setting the stage for a major card network shift.

And if you travel internationally, this is not something I would ignore.

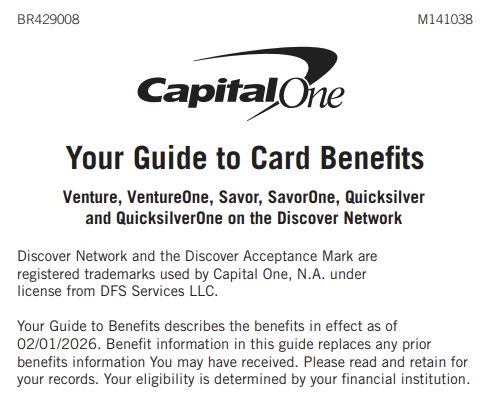

Capital One’s official Cardholder Benefits Guide page now includes a Discover Network guide for several major consumer cards, including Venture, VentureOne, Savor, SavorOne, Quicksilver, and QuicksilverOne. The guide says those cards are on the Discover Network and lists benefits in effect as of February 1, 2026. (Capital One ECM)

That does not automatically mean every existing cardholder is being switched overnight.

But it does mean this is more than a random rumor.

It is live on Capital One’s own benefits guide system. And that matters.

Quick Answer

Capital One’s official Discover Network benefits guide now lists Venture, VentureOne, Savor, SavorOne, Quicksilver, and QuicksilverOne on the Discover Network. Venture X is not listed in that Discover guide, and Capital One currently describes Venture X as part of the Visa Infinite network. (Capital One ECM)

My take: if you use Capital One for international travel, do not rely on one setup. Keep a Visa or Mastercard backup in your wallet before a network change catches you at the worst possible time.

What Happened With Capital One and Discover?

Capital One completed its acquisition of Discover on May 18, 2025. Capital One said Discover, PULSE, and Diners Club International would join its suite of offerings. (Capital One)

That part was already known.

The new concern is what showed up on Capital One’s benefits guide page.

Capital One says cardholder benefits may be handled through Visa, Mastercard, or Discover, depending on the card network. Capital One also tells cardholders to check the logo on the card or account statement to find the network. (Capital One)

And now, the Discover Network benefits guide lists these Capital One cards:

-

Venture

-

VentureOne

-

Savor

-

SavorOne

-

Quicksilver

-

QuicksilverOne

These are not tiny side products.

These are core Capital One consumer cards.

These are the cards a lot of people use every day.

And for years, many people built a simple Capital One travel setup around cards like Venture and Savor.

Why This Is Bigger Than It Sounds

From Capital One’s side, this move makes sense.

If Capital One owns Discover, why keep relying on Mastercard for a bunch of mass-market cards forever?

That is the business logic.

But from the customer side, the network matters.

A credit card can have the same issuer, same app, same rewards program, and same name. But if the payment network changes, the way that card works in real life can change too.

That is especially true overseas.

Inside the U.S., Discover acceptance is strong. Discover says it is accepted at 99% of places that take credit cards nationwide. (Discover)

But international travel is a different story.

Discover Global Network says it is accepted in more than 185 countries and territories and at millions of locations across the globe. That sounds solid, but “accepted in a country” does not mean “accepted at every hotel, restaurant, train kiosk, rental car counter, or ATM you personally need.” (Discover® Network)

And when you are 4,000 miles away from home, “maybe it works” is not good enough.

The Debit Card Preview

We have already seen a version of this with Capital One debit cards.

Capital One says it is switching its debit card network to Discover. It also says Mastercard network benefits will no longer be available once customers activate the new Capital One debit card on the Discover network. (Capital One)

That is not the same thing as a credit card migration.

But it gives you a preview of the problem.

Capital One specifically says international acceptance for the new debit or ATM card may be different than before. (Capital One)

That one sentence says a lot.

The bank can stay the same.

The account can stay the same.

The app can stay the same.

But once the network changes, acceptance can change too.

Why International Travelers Are Worried

The people who should pay the closest attention are international travelers.

If you built your wallet around Capital One because you liked no foreign transaction fees, simple rewards, and global acceptance, this could change how useful those cards are overseas.

For years, a Capital One setup could be very simple:

-

Venture for 2X miles everywhere

-

Savor or SavorOne for dining and grocery-type spend

-

No foreign transaction fees on key travel cards

-

Broad Mastercard acceptance in many places

That setup was easy.

It worked.

It was affordable.

But if those lower-tier or mid-tier cards start moving to Discover, the setup may not feel the same for travel.

Rewards are nice.

But when you are overseas, reliability matters more than rewards.

You do not want to wonder if your card will work.

You want it to work.

The Venture X Exception

The most interesting detail is what is missing.

Venture X is not listed in the Discover Network benefits guide.

Capital One currently describes Venture X as part of the Visa Infinite network, with Visa Infinite benefits tied to the card. (Capital One)

I do not think that is an accident.

If Venture, Savor, and Quicksilver families move toward Discover, then Venture X becomes the obvious premium lane for people who still want Visa acceptance inside the Capital One ecosystem.

Think about the positioning.

Before, you could run a clean Capital One setup for $0 or $95.

Now, if the lower-cost cards move to Discover while Venture X stays on Visa, the conversation changes.

If you want:

-

Visa Infinite benefits

-

Better travel protections

-

Lounge access

-

Stronger international reliability

-

A premium travel card setup

You may feel pushed up the ladder.

Capital One’s Venture vs. Venture X comparison lists Venture at a $95 annual fee and Venture X at a $395 annual fee. It also shows Venture X carrying premium benefits like a $300 annual Capital One Travel credit and 10,000-mile anniversary bonus. (Capital One)

That is the new positioning.

They may not need to add a new benefit to Venture X.

They may have just made Visa access itself more valuable.

That is what I call an upgrade path created by a downgrade.

What This Means for Capital One Cardholders

This may not matter much if you rarely leave the country.

If you mostly use your cards inside the U.S., Discover acceptance is strong, and your day-to-day spending may barely change. (Discover)

But if you travel overseas, live abroad part-time, or use Capital One as your main travel setup, you need a backup plan.

Before your next trip, check:

-

The network logo on your physical card

-

The network shown on your online or paper statement

-

Whether your card was recently reissued

-

Whether your card still has no foreign transaction fees

-

Whether your backup card is Visa or Mastercard

-

Whether your backup card has enough available credit

Capital One says the way to find your card network is to look for the Visa, Mastercard, or Discover logo on the front or back of your card, or check your account statement. (Capital One)

Do not assume.

Check it.

Do Not Rely on One Credit Card Setup

This is exactly why I always tell people not to rely on one setup.

Banks change rules.

Networks change.

Benefits change.

Approvals tighten.

Credit limits get cut.

Cards get refreshed.

And sometimes the card you loved still exists, but it does not work the same way anymore.

That is why backup cards matter.

Not because you need to carry 20 cards everywhere.

But because you do not want to be overseas depending on one issuer, one network, one app, and one customer service line.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you are building a backup card setup, my Free Credit Card & Loan Pre-Approval Master List can help you check which banks may pre-approve you before you submit a full application.

Should You Cancel Your Capital One Card?

No.

Do not panic-cancel a card just because a benefits guide changed.

That can backfire.

Closing a credit card can reduce your available credit, raise your utilization, and weaken your overall setup if you do not have a plan.

The smarter move is simple:

Keep the card if it still helps you.

Watch for any official account notice.

Check your network.

Build a backup before you need one.

Capital One said after the Discover acquisition that customer accounts and banking relationships remained unchanged at that time, and customers would receive information in advance of future changes. (Capital One)

So wait for your specific account details.

But do not wait to prepare.

What I Would Do Right Now

If I were using Capital One as my main travel setup, I would not panic.

But I would tighten up the wallet.

I would keep at least one strong Visa or Mastercard backup with:

-

No foreign transaction fees

-

Solid travel protections

-

Enough available credit for emergencies

-

A bank I can actually reach while traveling

-

Rewards that still make sense for my spending

I would also keep a backup debit card and a little emergency cash when traveling internationally.

That is not fear.

That is basic financial defense.

Suggested internal links to add during publishing: Best Credit Cards With Soft-Pull Pre-Approval, Best No Foreign Transaction Fee Credit Cards, Capital One Pre-Approval Guide, Visa vs Mastercard vs Discover for International Travel, and What to Do Before Applying for a Credit Card.

Frequently Asked Questions

Is Capital One moving Venture, Savor, and Quicksilver to Discover?

Capital One’s official Discover Network benefits guide lists Venture, VentureOne, Savor, SavorOne, Quicksilver, and QuicksilverOne on the Discover Network. That is official website evidence, but cardholders should still wait for account-specific notices to confirm whether their individual card will change and when. (Capital One ECM)

Is Capital One Venture X moving to Discover?

Based on the current public benefits guide, Venture X is not listed in the Discover Network guide. Capital One currently describes Venture X as part of the Visa Infinite network. (Capital One ECM)

Is Discover accepted internationally?

Discover Global Network says it is accepted in more than 185 countries and territories and at millions of locations worldwide. But acceptance can still vary by country, merchant, terminal, and ATM network, so I would not rely on Discover as my only card overseas. (Discover® Network)

How do I know what network my Capital One card is on?

Capital One says to look for the Visa, Mastercard, or Discover logo on the front or back of your card, or check your account statement. (Capital One)

Should I stop using Capital One for travel?

Not automatically. But if your Capital One card moves to Discover and you travel internationally, I would carry a Visa or Mastercard backup. Rewards do not matter if the card gets declined when you need it.

Will my Capital One rewards change if the network changes?

That needs account-specific confirmation. A network change does not automatically mean your rewards program changes, but card benefits, travel protections, and acceptance can change. Review any notice Capital One sends and check your current benefits guide.

Conclusion

Capital One moving major cards toward the Discover Network would be a big deal.

Not because Discover is useless.

It is not.

Inside the U.S., Discover acceptance is strong.

But international travel is where this gets uncomfortable.

If Venture, Savor, and Quicksilver card families move to Discover, the old Capital One setup may not work the same way for travelers who relied on broad Mastercard acceptance.

And Venture X not showing up in that Discover guide makes the strategy look even more interesting.

The lower-cost cards may be moving toward Discover.

The premium lane may stay Visa.

That is not random.

So do not wait until your card gets declined overseas.

Check your card network.

Build a backup.

And make sure your wallet still works in the real world, not just on a rewards chart.