How to Get a Business Credit Card Without an LLC

Jun 30, 2026

You do not always need an LLC to get a business credit card.

That surprises a lot of people.

They think they need to form a company, get an EIN, hire a lawyer, open business accounts, build a full website, and bring in revenue before a bank will even look at them.

Not always.

If you have a side hustle, freelance work, resale activity, gig work, consulting, content creation, delivery work, handyman jobs, or even a real plan to start earning money, you may be able to apply as a sole proprietor.

That is the simplest legal business setup.

No LLC required.

No corporation required.

No fancy paperwork required.

Just you, your Social Security number, and a real business purpose.

Quick Answer

You can apply for many business credit cards without an LLC by applying as a sole proprietor. A sole proprietor is an individual who runs a business without forming a separate legal entity, and many issuers allow sole proprietors to apply using their legal name and Social Security number. Approval still depends on your personal credit profile, income, application details, issuer rules, and business activity, and data points show people can be approved with low or even $0 business revenue when the rest of the profile is strong.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you are comparing business cards, my 0% APR Business Credit Card Database can help you research cards with intro APR offers, bureau-pull data points, and approval details before applying.

You Can Skip the LLC at First

A lot of people are sitting on the sidelines because they think they are “not official” yet.

Maybe you are selling items on eBay.

Maybe you do a few handyman jobs.

Maybe you deliver food after work.

Maybe you freelance a little.

Maybe you are planning to start consulting.

Maybe you have a small idea and want to separate expenses before things get bigger.

You may not be ready to form an LLC yet.

That does not automatically mean you have to use personal credit cards for everything.

You may be able to apply for a business credit card as a sole proprietor.

That is the key.

What Is a Sole Proprietor?

A sole proprietor is someone who owns and operates a business on their own without forming a separate legal entity like an LLC or corporation.

It is the simplest way to operate a business.

There is no separate company structure.

You are the business.

The business is you.

That means when you apply as a sole proprietor, you are basically telling the bank:

“I am operating this business activity under my own name.”

That can be enough for many business credit card applications.

Who Qualifies as a Sole Proprietor?

You do not need a giant company to qualify.

You may qualify if you do things like:

-

Freelance work

-

Consulting

-

Online sales

-

eBay selling

-

Etsy selling

-

Amazon selling

-

DoorDash or Uber Eats

-

Rideshare driving

-

Handyman work

-

Lawn care

-

Cleaning jobs

-

Content creation

-

Photography

-

Tutoring

-

Real estate work

-

Small local services

The business does not have to be huge.

It just has to be real or genuinely intended.

If you are making money, trying to make money, or setting up to make money, a sole proprietor application may be an option.

What If You Have $0 Revenue?

This is where people get nervous.

They ask:

“Can I apply for a business credit card with $0 revenue?”

Sometimes, yes.

Plenty of data points show people getting approved with low or even $0 business revenue.

But do not misunderstand that.

$0 revenue does not mean the bank ignores everything.

The bank may look heavily at:

-

Your personal credit score

-

Your personal income

-

Your existing credit limits

-

Your utilization

-

Your inquiry history

-

Your relationship with the bank

-

Your estimated business spend

-

Your business type

-

Your overall risk profile

So yes, $0 business revenue can still work.

But the rest of the application needs to make sense.

Banks Are Often Betting on You

For small business credit cards, banks are often underwriting the person behind the business.

That is especially true when the business is new or small.

If your side hustle only made $500, the bank may still approve you if your personal profile is strong.

If your business has $0 revenue, but you have high personal income, low utilization, and a clean file, the bank may still be comfortable.

That is why business cards are not only for established companies.

They are often for people building something.

The bank is not always saying:

“Show me two years of business tax returns.”

Sometimes the bank is saying:

“Do you, the applicant, look like a responsible borrower?”

How to Fill Out the Personal Info Section

The personal information section usually feels familiar.

It is similar to a personal credit card application.

You may be asked for:

-

Legal name

-

Date of birth

-

Social Security number

-

Home address

-

Phone number

-

Email

-

Gross annual income

This part is about you.

Even though the card is for business use, the issuer still needs to evaluate the owner.

Your personal credit and income can play a major role in the approval.

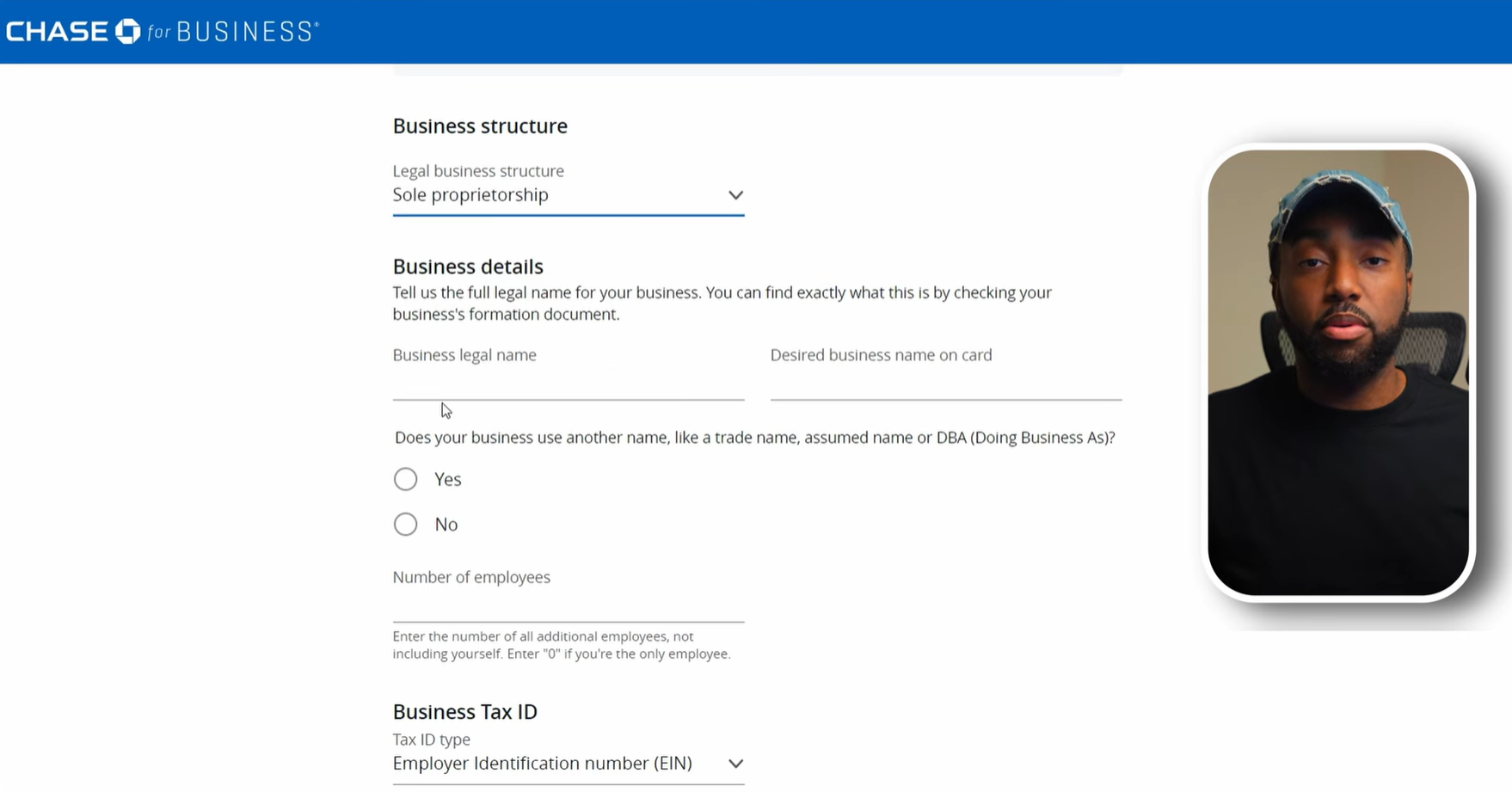

How to Fill Out the Business Structure

When the application asks for your legal business structure, choose:

Sole proprietorship

That is the setup for someone operating individually without forming an LLC, corporation, or partnership.

Do not choose LLC if you do not have an LLC.

Do not choose corporation if you do not have a corporation.

Do not try to make the business look more formal than it is.

Accurate beats fancy.

What Business Name Should You Use?

If you are applying as a sole proprietor, you can often use your personal legal name as the business name.

For example:

John Smith

That is simple and clean.

If you actually use a business name or DBA, you may be able to use that, depending on the application and whether the name is properly set up.

But if you do not have a registered business name, your personal name is usually the safest route.

Do not invent a formal-sounding company name just because it looks better.

If the bank asks for verification, that can create problems.

SSN vs. EIN

If you apply as a sole proprietor, you may be able to use your Social Security number instead of an EIN.

That is one of the biggest advantages of this setup.

You do not need a separate EIN just to apply as a sole proprietor in many cases.

Your SSN identifies you as the business owner.

That said, some applications may ask for both personal and business identification details depending on the issuer.

Always follow the application instructions.

Do not enter fake information.

What Business Address Should You Use?

If you run the business from home, you can usually use your home address.

That is normal for a sole proprietor.

A lot of small businesses start at home.

Do not rent an address just to look bigger unless it is a real business address you can verify and receive mail at.

Banks want consistency.

If your address does not match other records or looks suspicious, you can create unnecessary verification problems.

What Should You Put for Employees?

If it is just you, enter 0 employees if the application asks for employees excluding yourself.

Some applications may ask in different ways, so read the wording carefully.

Do not inflate employee count to make the business look bigger.

If you are the only person working in the business, keep it simple.

Banks would rather see a small truthful business than a big fake one.

What Established Date Should You Use?

Use the date your business activity actually started.

If you started selling online two years ago, use that timeframe.

If you began freelancing last month, use that.

If you are just starting now, use a recent date.

Do not make up a long history to look better.

The established date should match reality.

If the bank asks questions, your answer should be easy to explain.

What Should You Put for Annual Business Revenue?

This is one of the most important fields.

If your business made money, use your business revenue.

Not profit.

Revenue.

Revenue is the total amount the business brought in before expenses.

Profit is what is left after expenses.

A lot of people accidentally undersell themselves here because they enter profit instead of revenue.

That can hurt your starting limit.

For example, if your business brought in $10,000 but you only profited $2,000, the revenue field usually wants the $10,000 number.

Read the application carefully.

If it asks for revenue, do not enter profit.

If you truly have $0 revenue, entering $0 may be acceptable with some issuers.

But do not lie.

What If You Are Still in the Idea Phase?

This is where you need to be careful.

Having a business idea is not the same as pretending you have an operating business.

If you are preparing to start a business and need a card for startup expenses, some issuers may allow that.

But your application still needs to be honest.

If you have no revenue, say that.

If the business is new, say that.

If you are estimating monthly spend, make it realistic.

Banks understand that businesses start somewhere.

But they do not like fake numbers.

How to Choose a Business Category

The business category should match what you actually do.

For example:

-

Freelance writing: Professional services

-

Consulting: Business services or consulting

-

eBay reselling: Retail or online sales

-

DoorDash delivery: Transportation or delivery

-

Photography: Professional services

-

Handyman work: Construction, repair, or services

-

Content creation: Media, advertising, or online services

The category should be boring and obvious.

Boring is good.

A banker or underwriting system should be able to understand your business in a few seconds.

How to Estimate Monthly Spend

Estimated monthly spend is not a test of how brave you are.

It should be realistic.

Think about what you may actually put on the card:

-

Supplies

-

Software

-

Inventory

-

Shipping

-

Ads

-

Gas

-

Tools

-

Equipment

-

Phone bill

-

Internet

-

Travel

-

Contractor expenses

Do not claim $10,000 per month in spending if you realistically plan to spend $500.

But also do not undersell yourself if you have real business expenses coming.

Your estimate should make sense for your business type, revenue, and goals.

Data Point #1: Chase Ink Unlimited With $500 Freelance Income

One person applied for a Chase business card as a sole proprietor while planning to do more freelance development.

They had made about $500 from the side work over the past year.

They applied for the Chase Ink Business Unlimited.

At first, they received the 7-to-10-day message.

Then about 10 minutes later, they got an approval email.

Their data points:

-

TransUnion: 667

-

Experian: 718

-

Equifax: 662

-

Total gross income: $90,000

-

Projected business revenue: $2,000

-

Pulled personal Experian

-

Starting limit: $4,000

-

Existing Chase relationship with 3 personal cards

This is a great example.

The business revenue was tiny.

But the applicant had personal income and an existing Chase relationship.

That helped.

Data Point #2: Chase Ink Preferred With $3,000 Revenue

Another person opened the Chase Ink Business Preferred for the sign-up bonus.

They reported:

-

Experian FICO 8: 844

-

Utilization: 1%

-

Business revenue: $3,000

-

Personal income: $160,000

-

Sole proprietor for 20 years

-

Estimated monthly spend: $2,700

-

Existing Chase business checking relationship

-

Starting limit: $6,000

They first got a 7-to-10-day message, likely because they had a fraud alert.

They called in, verified identity, and got the approval email about 3 hours later.

This is another lesson.

Even with an excellent score and strong income, the starting limit was only $6,000.

That can happen.

Business card approval is one thing.

A huge starting limit is another.

Data Point #3: Approved With $0 Revenue

Another person reported being approved with $0 revenue.

They listed estimated monthly spend around $2,700, which they said would be accurate for the first three months to meet the sign-up bonus.

That is important.

The spend estimate had a purpose.

It was tied to real expected card use.

The lesson is not “make up $2,700.”

The lesson is:

If you have real planned business spending, list a realistic estimate.

Data Point #4: $2,000 Business Income and $5,000 Limit

Another person applied through the Chase app as a sole proprietor.

Their business was about three years old.

They reported:

-

Annual business income: $2,000

-

Personal income: $180,000

-

Estimated monthly spend: $7,000

-

7-to-10-day message at first

-

Approval email about 1.5 hours later

-

Credit line: $5,000

Again, the business revenue was not huge.

But personal income was strong.

That is a recurring theme.

Data Point #5: $1,000 Business Income and $5,000 Limit

Another person applied the same day and was approved within about an hour.

They reported:

-

Annual business income: $1,000

-

Personal income: $240,000

-

Credit line: $5,000

They also mentioned that they may have entered profit instead of revenue.

That matters.

If the application asks for revenue and you enter profit, you may be underselling the business.

That can potentially lead to a lower starting limit.

The Biggest Lesson From These Data Points

The lesson is not that everyone gets approved.

The lesson is that low business revenue does not automatically block you.

Across these examples, the approvals were supported by other strengths:

-

Personal income

-

Personal credit profile

-

Chase relationship

-

Low utilization

-

Existing credit history

-

Real business activity

-

Reasonable monthly spend

-

Identity verification when needed

Banks are not only looking at the business revenue number.

They are looking at the whole risk picture.

Why Chase Is Popular for Sole Proprietor Business Cards

Chase is one of the most popular issuers for sole proprietor business cards because the Ink lineup is strong.

The Chase Ink Business Unlimited currently offers:

-

No annual fee

-

Unlimited 1.5% cash back on purchases

-

0% intro APR offer

-

Employee cards at no additional cost

That makes it simple.

No rotating categories.

No complicated earning structure.

No annual fee.

It can be a good starter business card for someone who wants basic business rewards and a simple setup.

Helpful resource: If you want to compare business cards that may not report normal activity to personal credit, my No PG Business Credit Card Master List can help you research options separately from traditional sole proprietor business cards.

But Do Not Confuse Business Cards With No-PG Cards

This is important.

A business credit card is not automatically a no-personal-guarantee card.

Many small business cards still require the owner to personally guarantee the account.

That means you can still be personally responsible for the debt if the business does not pay.

So do not hear “business card” and think:

“No personal risk.”

That is not how this works.

If you want true no-PG corporate cards, that is a different category.

Those cards often care more about business revenue, bank balances, time in business, and cash flow.

A sole proprietor business card is usually still tied heavily to you.

Do Business Cards Report to Personal Credit?

Many small business credit cards do not report normal monthly activity to personal credit bureaus.

That is one reason people like them.

If the balance does not report to personal credit, it may help keep your personal utilization cleaner.

But reporting rules vary by issuer.

Some cards may report all activity.

Some may only report negative activity.

Some may report if the account becomes delinquent.

So always verify before applying.

Do not assume every business card stays off personal credit.

Why Business Cards Can Help Your Credit Strategy

Business cards can be useful because they may help you:

-

Separate business and personal spending

-

Track expenses more easily

-

Earn rewards on business purchases

-

Access 0% APR offers

-

Keep business balances off personal credit

-

Build issuer relationships

-

Prepare for larger business credit later

That is powerful.

But only if you use the card correctly.

Do not use business cards to hide personal overspending.

Do not max them out because the balance may not report.

Do not treat intro APR like free money.

Use the card for a plan.

Not chaos.

What to Do Before Applying

Before applying for a business credit card as a sole proprietor, clean up the basics.

Check:

-

Personal credit score

-

Personal utilization

-

Recent inquiries

-

New accounts

-

Existing relationship with the issuer

-

Business activity

-

Business revenue

-

Estimated monthly spend

-

Business category

-

Application accuracy

-

Whether the card reports to personal credit

-

Whether there is a personal guarantee

If you are applying with Chase, also think about your Chase relationship and recent new accounts.

Chase can be sensitive to people opening too many cards too fast.

Common Mistakes to Avoid

Do not make these mistakes on a business credit card application:

-

Listing an LLC when you do not have one

-

Inventing a business name

-

Entering profit when the field asks for revenue

-

Inflating revenue with fake numbers

-

Claiming employees you do not have

-

Using a business category that does not match

-

Estimating monthly spend unrealistically

-

Applying with high utilization

-

Applying after too many recent inquiries

-

Assuming approval means a high limit

-

Assuming every business card avoids personal reporting

Most denials are not shocking.

They happen because the profile, application, or timing did not make sense.

Frequently Asked Questions

Can I get a business credit card without an LLC?

Yes. Many issuers allow sole proprietors to apply for business credit cards without an LLC. You may be able to use your legal name as the business name and your Social Security number instead of an EIN.

Can I apply for a business credit card with no revenue?

Yes, it can happen. Data points show some people getting approved with $0 or very low business revenue. But approval depends on the full profile, including personal credit, personal income, utilization, inquiries, issuer relationship, and application details.

What should I put as my business name as a sole proprietor?

If you do not have a registered business name or DBA, your personal legal name is usually the simplest option. Do not invent a business name you cannot verify.

Should I use revenue or profit on the application?

If the application asks for annual business revenue, use revenue, not profit. Revenue is the total money the business brings in before expenses. Profit is what remains after expenses.

Do I need an EIN for a business credit card?

Not always. Sole proprietors can often apply using a Social Security number. Some issuers may allow or request an EIN, but an EIN is not always required for a sole proprietor application.

Is a business credit card the same as a no-PG card?

No. Many small business credit cards still require a personal guarantee. True no-PG corporate cards are different and usually rely more on business revenue, cash flow, bank balances, and company strength.

Conclusion

You do not need an LLC to start using business credit cards.

You can apply as a sole proprietor.

That means your side hustle, freelance work, gig income, online sales, or early business idea may be enough to get started.

But do not get sloppy.

Use the right business structure.

Tell the truth.

Use your real revenue.

Estimate spending realistically.

Do not inflate the business.

Do not confuse business cards with no-PG cards.

And remember that your personal credit profile still does a lot of the heavy lifting.

The real goal is not just getting approved.

The goal is using business credit to separate expenses, protect your personal credit strategy, earn rewards, and build toward bigger business funding later.