Best Debt Consolidation Loans in 2026: When They Help and When They Trap You

Jun 26, 2026

Most people look at debt consolidation loans like a last-ditch move.

But when you use the right one the right way, consolidation can actually speed up your payoff instead of trapping you longer.

Think about logging into your bank account and seeing five or six different minimum payments staring back at you. Credit cards. Store cards. Personal loans. Random payments due on different days.

Then imagine replacing all of that chaos with one clear number you can actually attack.

That is when your finances finally start to feel manageable again.

But there is a catch.

Debt consolidation only works when the math actually improves. If you use it just to lower your monthly payment while stretching the debt out for years, you did not solve the problem.

You just made the problem quieter.

And quiet debt is dangerous.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

The best debt consolidation option depends on your credit, debt amount, and payoff plan. LendingClub can be strong for middle-credit borrowers, SoFi can work well for larger loan amounts, Upgrade may fit borrowers with lower or thinner credit, and Happy Money can be worth checking for credit card payoff loans. A 0% balance transfer card from a credit union may beat a consolidation loan if you can pay the balance down before the promo ends. Rates, approvals, credit pulls, loan terms, and lender rules can change, so verify the current offer before applying.

What Is Debt Consolidation?

Debt consolidation is not magic.

It does not erase debt.

It does not fix spending habits.

And it definitely does not work if you are just shuffling balances around and hoping something changes.

At its core, debt consolidation is simple.

You take multiple high-interest debts, usually credit cards, and replace them with one new account that has:

-

A lower interest rate

-

A fixed term

-

One predictable payment

-

A clear payoff timeline

That is it.

When debt consolidation is done intentionally, it can help in three big ways.

First, it can lower the interest you are bleeding every month.

Second, it can simplify your payments so you are more consistent.

Third, it can give you a real finish line instead of an endless credit card loop.

That last part matters.

Credit cards are dangerous because the minimum payment can make you feel like you are doing something, even when most of your money is going toward interest.

A good consolidation loan can turn that mess into a plan.

But only if you use it correctly.

The Number One Rule: Only Consolidate If the Math Improves

Here is the rule most people skip:

You only consolidate if the math improves.

That means you need at least one of these:

-

A lower APR

-

A shorter or equal payoff timeline

-

Ideally, both

If you consolidate just to lower your monthly payment but extend the debt another five to seven years, you may not be saving yourself.

You may just be making the debt feel less painful today.

And that is where people get trapped.

A lower payment can feel like relief. But if that lower payment comes with a much longer term, you might pay more interest over time.

So before you accept any debt consolidation loan, look at the full picture:

-

What is the APR?

-

What is the loan term?

-

What is the monthly payment?

-

What is the total interest paid?

-

Are there origination fees?

-

Will you actually stop using the credit cards after consolidating?

That last question is the one nobody likes to answer.

Because if you consolidate the credit cards and then run the cards back up again, now you have the loan payment and new credit card balances.

That is how consolidation turns into a disaster.

LendingClub: A Strong Middle-Ground Debt Consolidation Option

One of my top picks for many people is LendingClub.

The reason LendingClub stands out is because they sit in the middle of the credit spectrum.

They are not only for perfect credit.

But they are also not in the same category as expensive, last-resort lenders that can make your situation worse.

That middle ground matters.

LendingClub can be useful for borrowers who have decent credit but are not walking in with an 800 score and a perfect file.

Why LendingClub can work:

-

Competitive starting APRs for strong applicants

-

Potential approval for borrowers in the low-to-mid 600s

-

Loan amounts that can start around $1,000

-

A structure that may work for smaller consolidation needs

That loan size point is important.

Not everybody needs a $40,000 personal loan.

Some people need to wipe out $6,000, $8,000, or $12,000 of revolving debt before it gets out of control.

That is where LendingClub can make sense.

But do not get distracted by the best advertised rate.

Their best rates go to their best profiles.

If your credit is rough, you may still get approved, but probably not at the headline rate. Even then, it still might be better than sitting on credit card debt at 25% to 30% APR.

The key word is “might.”

You still have to compare the actual offer against your current debt.

SoFi: A Better Fit for Larger Debt Consolidation Loans

For larger, more serious debt consolidation, I like SoFi.

SoFi is built more for borrowers who want larger loan amounts, cleaner underwriting, and multiple offer options at approval.

Instead of giving you one loan structure and forcing you to take it or leave it, SoFi often shows different options.

You may see different:

-

Loan terms

-

Interest rates

-

Monthly payments

-

Payoff timelines

That matters because it lets you choose based on strategy, not panic.

And here is the strategy I would use:

Pick the shortest term you can realistically afford.

Do not automatically choose the smallest payment.

Choose the fastest exit that still gives you room to breathe.

That is how you use debt consolidation like a weapon instead of a bandage.

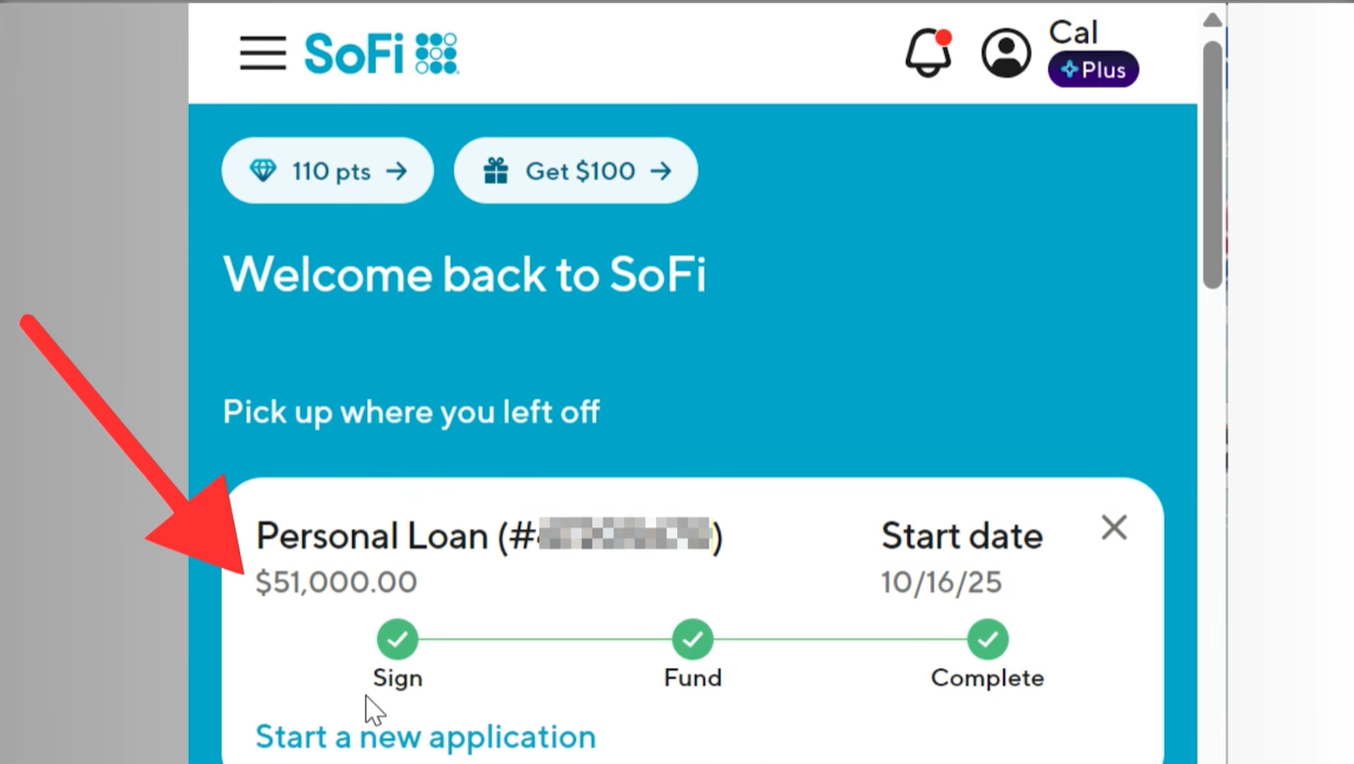

I was personally approved by SoFi for a $51,000 personal loan with no documentation required and same-day funding.

What mattered most was not just the amount. It was the process.

In my case, SoFi did not force me into one offer. I was shown multiple structures, they pulled Experian only, and I had the flexibility to choose what fit my plan.

That is why SoFi can work well for larger consolidation.

It gives you room to think instead of forcing you to panic.

Helpful resource: If you are considering SoFi for debt consolidation, you can review the SoFi Personal Loans option here before deciding whether the math makes sense for your situation.

Upgrade: A More Flexible Option for Lower Credit Scores

Let’s be honest.

Not everyone looking for a debt consolidation loan has a 750 credit score.

Some people have a low 600s score.

Some people have a thin credit file.

Some people still have past mistakes sitting on their report.

That is where Upgrade may be worth looking at.

Upgrade is often more forgiving than lenders that only want clean, higher-credit borrowers.

They may be a better fit for people dealing with:

-

Lower credit scores

-

Thin credit files

-

Recent credit mistakes

-

Limited loan options elsewhere

Upgrade also offers secured options in some cases.

That can matter because a secured loan may improve approval odds or lower the interest rate compared to an unsecured option.

But let me be clear.

Upgrade is usually not the cheapest option.

It may be more of a bridge option.

And sometimes a bridge option is still useful if it keeps someone away from payday loans, extreme-interest products, or sketchy debt consolidation companies.

The same rule still applies, though.

Only move forward if the math improves.

If the offer is barely better than your credit cards, or if the fees make it unattractive, keep looking.

Happy Money: A Debt Payoff Option People Overlook

Happy Money takes a different angle.

Instead of acting like a traditional big bank, Happy Money works with credit unions behind the scenes.

That is worth paying attention to because credit unions can sometimes be:

-

More flexible

-

Lighter on fees

-

More focused on member relationships

-

More reasonable with rates

Happy Money is especially interesting if your debt is mostly credit card debt and your credit is good to excellent.

That is the sweet spot.

This is not necessarily the first lender I would look at if your credit is damaged or your income is hard to verify.

But if you are trying to pay off credit cards and you have a strong enough profile, Happy Money deserves a look.

Again, do not just look at the payment.

Look at the APR, fees, term, and total cost.

A good consolidation loan should help you escape the credit card trap, not give you a new trap with a nicer name.

The Zero-Interest Wild Card: 0% Balance Transfer Cards

Now let’s talk about the option that is not technically a loan.

A 0% balance transfer card can outperform almost every debt consolidation loan if you use it correctly.

The reason is simple.

With a loan, even a good one, you are usually still paying interest.

With a true 0% balance transfer offer, your payments can go straight toward the principal during the promo period.

That can be powerful.

But the key phrase is “during the promo period.”

If you transfer a balance and then coast, you are just delaying the pain.

If you transfer a balance and attack it aggressively, that is different.

That can save serious money.

Why Credit Unions Can Be Better for Balance Transfers

Instead of only looking at big banks or fintech cards, I would pay close attention to local credit unions.

A great example is PSECU’s Classic Card.

This route deserves serious attention because the offer can be stronger than many people expect.

The PSECU Classic Card has offered:

-

0% APR on balance transfers through mid-2027

-

Transfers made in 2026 staying interest-free until June 30, 2027

-

A post-promo APR around 12.9%

That is a very different fallback point compared to many credit cards.

Right now, average credit card interest rates are around 20%, and I have seen some cards as high as 33%, which is wild.

So here is the play:

Transfer high-interest balances.

Lock in a long 0% window.

Pay the balance down aggressively while every dollar goes toward principal.

If you actually commit to the timeline, this approach can save thousands in interest.

In some cases, it can save more than a consolidation loan.

Helpful resource: If you are researching credit unions that may be easier to join, my 150+ Credit Unions Anyone Can Join Database can help you find more credit union options to compare.

The Trade-Offs With Credit Union Balance Transfers

Credit union balance transfer cards are not perfect.

They can be slower.

They can be more paperwork-heavy.

And they may not give you a giant limit right away.

Credit unions may:

-

Take longer to approve than fintech lenders

-

Ask for documentation like paystubs or W-2s

-

Offer smaller credit limits than you hoped for

-

Require membership before you can apply

That means a credit union balance transfer card may not cover your entire balance.

And that is okay.

Even if it only covers part of the balance, it can still help if it moves your most expensive debt to 0%.

The upside is what happens after the promo period.

If you do not finish the payoff in time, you may not fall back into a 25% to 30% APR trap.

With the right credit union card, you may land in a much lower APR range, which gives you more breathing room.

That does not mean you should drag it out.

It means the downside may be less painful than a high-interest card.

Also, some credit unions are more accessible than people realize.

For example, even if you are not in Pennsylvania, PSECU membership may be available nationwide through groups like the Pennsylvania Recreation and Parks Society or the Pennsylvania Consumer Council.

That is why I always tell people not to ignore credit unions.

Sometimes the best debt payoff tool is not the loudest lender online.

Personal Loan vs. Balance Transfer Card: Which Is Better?

This depends on your situation.

A personal loan may be better if you need a fixed payment, a fixed term, and a structured payoff plan.

A balance transfer card may be better if you can qualify for a large enough limit and you can aggressively pay the balance down before the promo ends.

Here is how I would think about it.

A debt consolidation loan may make more sense if:

-

You want one fixed monthly payment

-

You need a larger amount

-

You want a clear end date

-

You do not trust yourself with open credit card limits

-

You can get a lower APR than your current cards

A 0% balance transfer may make more sense if:

-

You can qualify for the card

-

The balance transfer fee still makes the math work

-

You can pay the balance before the promo ends

-

The post-promo APR is reasonable

-

You will not run the old cards back up

The best option is not always the one with the lowest payment.

The best option is the one that gets you out of debt faster for less total cost.

When You Should Not Consolidate Debt

Do not consolidate if you are still actively running balances back up.

Do not consolidate if you do not know why the debt happened.

Do not consolidate if you are using the loan to avoid lifestyle changes.

Debt consolidation should be a strategy, not an emotional relief button.

Because the first few days after consolidating can feel amazing.

Your cards are paid down. Your payments are simplified. Your credit utilization may look better. Everything feels cleaner.

But if the spending habits do not change, the old debt comes back.

And now you have a personal loan too.

That is the danger.

Before consolidating, be honest with yourself.

Are you consolidating because you have a plan?

Or are you consolidating because you want the stress to go away for a few weeks?

Those are not the same thing.

How to Compare Debt Consolidation Offers

Before accepting any debt consolidation loan or balance transfer offer, slow down and compare the numbers.

Here is what I would check:

-

Current APR on each debt

-

New APR

-

Origination fee

-

Balance transfer fee

-

Loan term

-

Monthly payment

-

Total interest paid

-

Promo expiration date

-

Post-promo APR

-

Whether the lender does a soft pull first

-

Whether the lender verifies income

-

Whether funding is fast enough for your situation

Do not apply blindly if you can avoid it.

Pre-qualification or pre-approval tools can help you compare possible offers before committing to a hard pull, but they are not guarantees.

And remember, the lowest monthly payment is not always the best deal.

Sometimes a higher monthly payment with a shorter term saves you far more money.

The goal is not comfort.

The goal is freedom.

The Best Debt Consolidation Strategy

The best debt consolidation strategy is not complicated.

First, stop adding new debt.

Second, compare your current interest rates against the new offer.

Third, choose the shortest payoff timeline you can realistically afford.

Fourth, keep the old cards from becoming a new problem.

That might mean locking the cards, lowering limits, removing saved payment methods, or using a strict budget until the loan is paid off.

Because consolidation is not the finish line.

It is the setup.

The real win happens after you consolidate, when you keep making the payment, avoid new balances, and finally get out of the loop.

Frequently Asked Questions

Is debt consolidation a good idea?

Debt consolidation can be a good idea if it lowers your APR, creates a clear payoff timeline, and helps you stay consistent. It is a bad idea if you only use it to lower the monthly payment while extending the debt for years.

Does debt consolidation hurt your credit?

It can affect your credit in different ways. A loan or balance transfer application may involve a credit check. Paying down revolving credit card balances may help utilization, but opening new accounts and carrying debt can also affect your profile. The exact impact depends on your credit report.

What credit score do you need for a debt consolidation loan?

It depends on the lender. Some lenders prefer stronger credit, while others may work with borrowers in the low-to-mid 600s. Your income, debt-to-income ratio, credit history, and current balances can also matter.

Is a personal loan better than a balance transfer card?

A personal loan may be better if you want fixed payments and a fixed payoff date. A balance transfer card may be better if you can qualify for 0% APR and pay the balance before the promo ends. The better option is the one that saves the most money and fits your behavior.

Should I consolidate credit card debt with a loan?

You should only consolidate credit card debt with a loan if the math improves. That means the APR, fees, term, and total cost should put you in a better position than staying where you are.

What is the biggest mistake people make with debt consolidation?

The biggest mistake is consolidating the debt and then running the credit cards back up again. That leaves you with the new loan plus new card balances, which can put you in a worse position than before.

Conclusion

Debt consolidation is not a magic trick.

It is a tool.

Used the right way, it can lower your interest, simplify your payments, and give you a real payoff plan.

Used the wrong way, it can make your debt quieter while keeping you trapped longer.

LendingClub can make sense for borrowers in the middle of the credit spectrum.

SoFi can be strong for larger consolidation loans and borrowers who want multiple offer structures.

Upgrade may work for people with lower or thinner credit.

Happy Money is worth checking if your debt is mostly credit cards and your credit is good to excellent.

And a 0% balance transfer card from a credit union can sometimes beat almost every loan if you can stick to the payoff timeline.

Just remember the rule:

Only consolidate if the math improves.

Not if the payment just feels better.

Not if you are still spending.

Not if you are avoiding the real problem.

If the math improves and you have a plan, debt consolidation can help you get out faster.

If not, it is just another account with a new name.