BECU $34,000 Approval: Credit Card and Line of Credit With One Hard Pull

Jul 03, 2026

Our community member Mario got approved for $34,000 from BECU with only one hard pull.

That approval included:

-

$19,000 personal credit card

-

$15,000 personal line of credit

-

One TransUnion hard inquiry

That is the kind of approval that can change your whole credit profile when used responsibly.

More available credit can help lower utilization, protect your score from big balance swings, and give you more flexibility when life or business opportunities show up.

But Mario’s approval did not happen by accident.

He rebuilt his credit.

He restored his banking relationship.

He kept utilization extremely low.

He walked into the branch instead of applying randomly online.

And he knew how to ask for more than one product from the same pull.

This is the BECU playbook.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Mario got approved for $34,000 from BECU with one TransUnion hard pull by applying for a personal credit card and personal line of credit during the same branch visit. His profile was strong: FICO scores between 807 and 849, 1% to 3% utilization, over 20 clean tradelines, about $96,000 stated income, and a rebuilt relationship with BECU. The key strategy was applying in person, asking about multiple products under one pull, and having a bankable profile before walking into the branch.

What Is BECU?

BECU is one of the largest credit unions in the country.

It started as Boeing Employees’ Credit Union, but today it serves a much wider membership base.

BECU is a not-for-profit credit union, which means it is member-owned instead of shareholder-owned. That structure is one reason credit unions can sometimes offer strong rates, relationship-based underwriting, and more flexible banking experiences than big banks. BECU describes itself as a member-owned, not-for-profit credit union.

That is why BECU is worth paying attention to.

Especially if you like credit unions that can approve multiple products and reward a strong member relationship.

Mario’s Starting Point Was Not Perfect

Mario’s story matters because he did not start from perfect.

When he came home to Washington state, life looked very different than it used to.

He had been behind bars.

He had lost time, stability, and financial momentum.

His old BECU account had been closed while he was away.

So the first move was not chasing approvals.

The first move was rebuilding.

He went back to BECU, reopened checking and savings, and restarted the relationship.

No shortcuts.

No flashy moves.

Just steady deposits, clean credit behavior, and time.

That is the part people skip.

They want the $34,000 approval.

But they do not want the months of rebuilding that came before it.

Why Mario Rebuilt With BECU

Mario had trusted BECU for almost a decade before everything fell apart.

So when he came back, he did not treat BECU like a random lender.

He treated it like a relationship he needed to rebuild.

He split deposits between Navy Federal and BECU so both institutions could see activity.

That matters because credit unions often care about relationship.

Not always in a magical way.

But banking activity can help tell a story.

Deposits.

Account seasoning.

Responsible usage.

Low-risk behavior.

Those things can matter when you are asking a credit union for serious exposure.

The Personal Reason Behind the Rebuild

Mario’s rebuild was not just about credit cards.

It was personal.

He had recently lost both his mother and grandmother within a 90-day span.

And losing his mother hit him hard.

He told me:

“My mother died, but she died on the phone with me. I had to listen to the flatline. That night I made a decision to make some changes in my life.”

That moment changed him.

It pushed him to live differently.

To rebuild.

To become more disciplined.

To honor his mother with how he moved going forward.

That is why this story is bigger than a credit approval.

The approval was just proof that the work was paying off.

The Credit Issues Mario Had to Fix

Mario’s file still had old scars.

One of the biggest was a back child support tradeline that stayed on his report even after the debt had been resolved.

He worked with a credit repair specialist for about two years to get that situation handled.

He did not know every technical detail of how the specialist got it done.

But he knew the result:

That old issue stopped holding his profile hostage.

That matters because old negative items can make lenders nervous even when your current behavior is strong.

Mario had to clean that up before his profile looked bankable.

Why Qualstar Denied Him First

Even after rebuilding, Mario still hit setbacks.

He had recently completed a personal credit stack, which means he added several new accounts in a short window.

That can strengthen your profile over time.

But in the short term, it can also make you look risky.

When he applied at Qualstar Credit Union, they denied him for too many recent accounts.

That is an important lesson.

You can have strong scores and still get denied.

Lenders care about velocity.

If you open too many accounts too quickly, some banks and credit unions will see that as risk.

Mario did not let that stop him.

He learned from it and moved smarter with BECU.

The Branch Visit That Changed Everything

Most people apply online and hope.

Mario walked into the branch.

That decision mattered.

He sat down with a banker who understood how BECU applications could work.

The banker told him he could apply for up to three products with one hard pull.

That could include:

-

Credit card

-

Personal line of credit

-

Auto loan or personal loan

Mario did not go for all three.

He asked for two:

-

A personal credit card

-

A personal line of credit

That is how he turned one inquiry into $34,000 in new credit exposure.

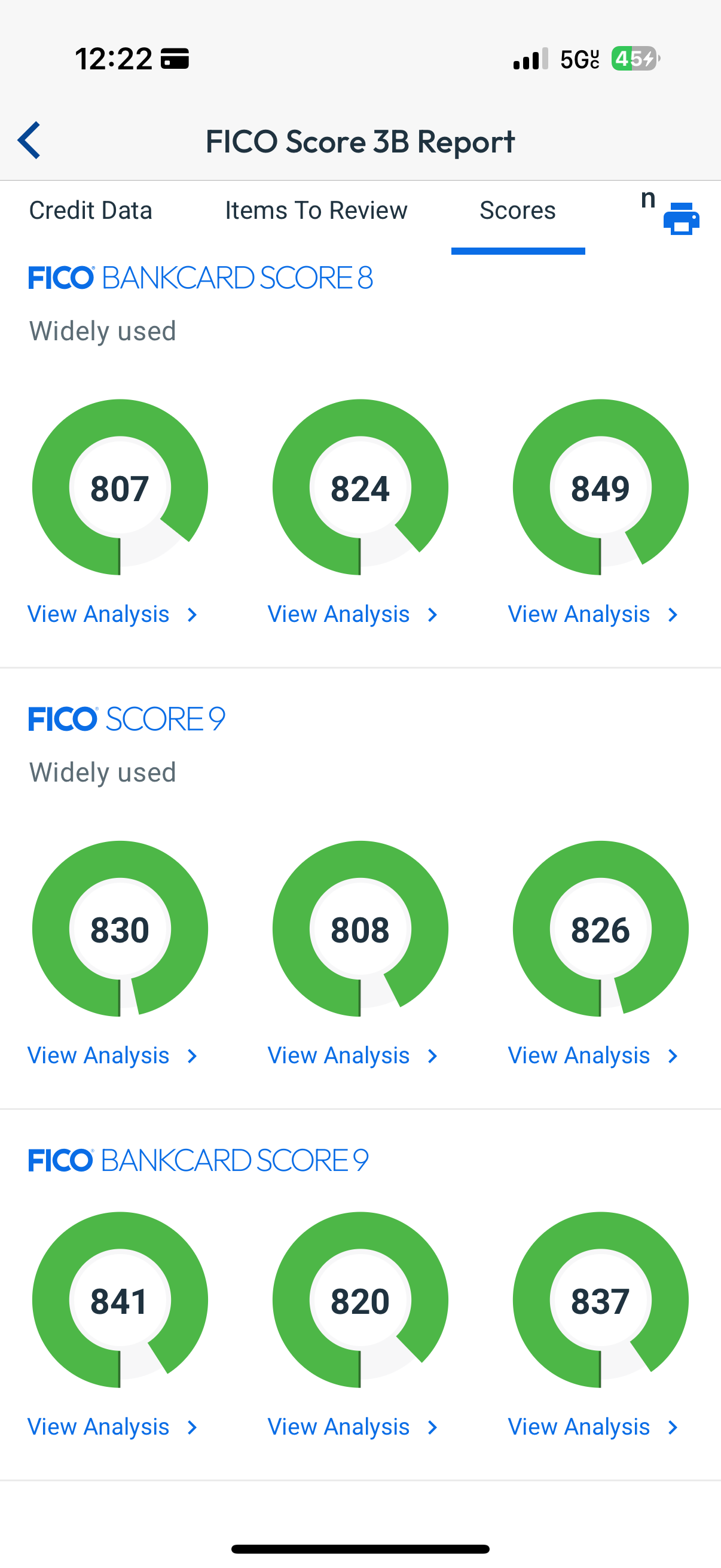

Mario’s Credit Profile at the Time

Mario’s profile was strong when he walked into BECU.

Here is what it looked like:

-

FICO scores: 807 to 849 across Bankcard 8 and 9 models

-

Utilization: 1% to 3%

-

Open tradelines: 20+

-

Late payments: none reporting

-

Income: about $96,000 stated

-

New accounts: several, but all clean and paid properly

-

Banking relationship: reopened BECU checking and savings

This is what I call a bankable profile.

Low utilization.

Strong scores.

Clean payment history.

Real income.

Established tradelines.

A credit union relationship.

That does not guarantee approval.

But it gives the lender a lot more reasons to say yes.

The Final BECU Approval

Within minutes, Mario was approved.

The final result:

-

$19,000 BECU personal credit card

-

$15,000 BECU personal line of credit

-

$34,000 total approval

-

One TransUnion hard pull

That is a serious win.

And it shows why you do not always want to waste a hard inquiry on one product if the lender allows multiple applications under the same pull.

One pull.

Two approvals.

$34,000 total.

That is how you maximize an inquiry.

Why the Personal Line of Credit Matters

Most people only think about credit cards.

But a personal line of credit can be just as useful.

BECU says its personal line of credit can be tied to a checking or money market account, can provide overdraft protection, and has no annual fees or transfer fees. Interest accrues when an advance or transfer is made.

That gives you another flexible credit tool.

You do not want to abuse it.

You do not want to treat it like free money.

But having access to a personal line of credit can help with emergency liquidity, overdraft protection, and overall financial flexibility.

That is why Mario’s approval was stronger than just a credit card.

He got a card and a line.

Why One Hard Pull Matters

Hard pulls matter because they can affect your credit score and remain on your credit report.

One inquiry is usually not the end of the world.

But multiple inquiries in a short period can make lenders nervous.

Experian explains that a hard inquiry happens when you apply for new credit and can affect your score, although the impact is usually brief.

That is why this BECU strategy is so powerful.

If you can apply for more than one product under one pull, you may get more credit exposure without stacking multiple inquiries.

That is the whole point.

BECU Usually Pulls TransUnion in These Datapoints

Mario’s approval was from one TransUnion pull.

There are also community datapoints suggesting BECU often uses TransUnion and that a pull may be usable for multiple products for a period of time.

One MyFICO datapoint says a BECU underwriter confirmed they only pull TransUnion and that the pull was good for 30 days, though that is a community datapoint and should be verified directly with BECU before applying.

So the working assumption is:

BECU may be a TransUnion-heavy credit union.

But do not treat that as guaranteed.

Credit bureau pulls can vary by product, applicant, state, timing, and internal policy.

Ask before applying.

BECU Video Banking Can Help If You Are Not Near a Branch

Mario applied in person.

But BECU also offers video banking.

That matters if you are not close to a branch.

BECU says video banking lets members get live, personalized banking assistance from home, and its video banking services can support membership applications, account openings, loan applications, and credit card applications.

That is huge.

Because the whole strategy is not just “apply.”

The strategy is to talk to a person, ask about multiple products, and confirm how the pull will be handled.

Video banking may give you a way to do that without physically walking into a branch.

Can Anyone Join BECU?

This is where you need to be careful.

The source story says anyone in the U.S. can join BECU by becoming a BECU Foundation member for $1.

BECU’s current eligibility page says some people may be eligible based on where they live, work, worship, or attend school, family or household relationships, employment, Boeing or credit union connections, and other criteria. It also says people in South Carolina may be eligible by visiting the North Charleston Neighborhood Financial Center and donating $1 or more to support the BECU Foundation.

So I would not publish “anyone nationwide can join online for $1” without verifying the exact current process.

The $1 BECU Foundation path appears to exist in some form, but BECU’s own eligibility page currently frames it around visiting the North Charleston location for South Carolina.

That does not mean the strategy is dead.

It means this part needs verification before readers rely on it.

The BECU Playbook

Now let’s talk about the actual playbook.

This is how I would approach BECU if I wanted to maximize my chances.

Step 1: Confirm Membership Eligibility First

Do not assume.

Check BECU’s current membership rules first.

If you are in Washington, certain counties in Oregon or Idaho, parts of South Carolina, connected to Boeing, connected to a credit union, or meet another eligibility path, you may qualify. BECU’s official eligibility page should be the final source before you apply.

And if you are trying to join through the BECU Foundation route, call BECU and confirm the exact steps.

Do not rely on old datapoints.

Membership rules can change.

Step 2: Open Checking and Savings

Once you are eligible, open checking and savings.

Do not treat the account like a shell.

Use it.

Make deposits.

Set up recurring transfers.

Let the account show activity.

Mario reopened his relationship and let BECU see him as an active member again.

That is the kind of relationship signal credit unions often care about.

Step 3: Season the Relationship for 30 to 60 Days

Do not open the account and apply the same day unless you have a very strong reason.

Let the relationship season.

Thirty to sixty days is a better starting point.

That gives the credit union time to see activity.

Even a small direct deposit or recurring transfer can help your account look alive.

Dormant accounts do not tell a strong story.

Active accounts do.

Step 4: Get Utilization Extremely Low

Mario kept utilization between 1% and 3%.

That is excellent.

Low utilization makes your profile look cleaner.

It also gives lenders confidence that you are not desperate for credit.

If your utilization is high, a big approval is harder.

Before applying, clean up your reports.

Pay down balances.

Let low utilization report.

Do not walk into a credit union asking for $30,000 while your cards are maxed out.

Step 5: Avoid Looking Too Aggressive

Mario had recent accounts, but they were all clean.

That still created some risk.

Remember, Qualstar denied him for too many recent accounts.

So if you have been stacking credit lately, be careful.

Too many new accounts can make a lender nervous even if your score is high.

If your file looks aggressive, consider waiting until the accounts age a bit before applying.

Step 6: Apply In Branch or Through Video Banking

This is the pro move.

Do not blindly apply online for multiple products.

Mario heard of people getting separate hard pulls because they clicked through online applications separately.

Instead, talk to a banker.

Go in branch if possible.

Use video banking if needed.

Ask directly:

“Can I apply for a credit card and personal line of credit under one hard pull?”

Then let the banker guide the process.

BECU says video banking can help with loan and credit card applications, which makes this a strong option if you cannot visit in person.

Step 7: Ask About the Double or Triple Dip

The key strategy is maximizing the pull.

If BECU allows multiple products under one inquiry, ask what can be included.

Possible products may include:

-

Personal credit card

-

Personal line of credit

-

Auto loan

-

Personal loan

You do not need to take every product.

But you should know your options.

The banker can tell you what makes sense for your profile.

This is how you avoid wasting a hard inquiry on a single small approval.

Step 8: Be Ready With Documentation

If your profile is strong, the application may be simple.

But be ready anyway.

Have your income information.

Employment details.

Housing information.

Identification.

And if you are self-employed or have unusual income, be ready to explain it.

A clean, confident application process matters.

What Mario Did After the Approval

Mario did not use the approval to go wild.

That is what I respect.

Across all his cards and lines of credit, his total available credit grew to more than $275,000.

But he still lives simply.

He drives a 1998 Toyota Corolla that he calls his “little scooter.”

No big car payment.

No fake flex.

No pressure to look rich.

That is the part people need to understand.

Credit is not about looking wealthy.

Credit is about flexibility.

Control.

Leverage.

Options.

When used right, it gives you room to move.

When used wrong, it becomes a trap.

Building Credit for the Next Generation

Mario also used what he learned to help his daughter.

He added her as an authorized user early, helping her build credit age and history before she turned 18.

Then when she applied on her own, Navy Federal approved her instantly for a $10,900 credit card on day one.

That is powerful.

She also opened accounts with BCU and KeyBank, following the same diversification strategy her dad taught her.

When BCU offered her a secured card, Mario told her to decline because she was already positioned for better.

That is what financial education can do.

It changes the next generation’s starting line.

Is BECU Better Than Navy Federal?

Mario said BECU might be better than Navy Federal.

That is a bold statement.

Especially coming from someone who has been with Navy for years.

His reason was simple:

BECU gave him strong approvals, competitive rates, and a smooth branch experience.

Does that mean BECU is better for everyone?

No.

Navy Federal is still powerful.

But BECU deserves to be in the conversation.

Especially if you can join, build a relationship, and apply strategically.

Who This BECU Strategy Is Best For

This strategy is best for people who:

-

Can qualify for BECU membership

-

Have strong TransUnion data

-

Keep utilization very low

-

Have clean payment history

-

Want a credit card and personal line of credit

-

Are willing to build a relationship first

-

Can apply in branch or through video banking

-

Want to maximize one hard pull

This is not a beginner strategy.

It works best when your profile is already built.

Who Should Wait

You may want to wait if:

-

Your utilization is high

-

You have recent late payments

-

You have unresolved collections

-

You just opened several new accounts

-

Your income is unstable

-

You cannot verify BECU membership

-

You are not ready for a hard pull

-

You would use the credit to overspend

Do not chase a $34,000 approval if your foundation is weak.

Build first.

Apply later.

Helpful resource: Before applying for a new card, it may be worth checking soft-pull pre-approval options so you can compare offers before risking unnecessary hard pulls.

Frequently Asked Questions

Can you get multiple BECU approvals with one hard pull?

Mario was approved for a BECU credit card and personal line of credit with one TransUnion hard pull. There are also community datapoints saying BECU may allow multiple products from one pull, but you should verify directly with BECU before applying.

What credit bureau does BECU pull?

Mario’s approval used TransUnion. Community datapoints also point to TransUnion, but BECU’s bureau behavior should be verified before applying because pulls can vary by product, timing, and policy.

Can anyone join BECU?

BECU has several membership paths, including geographic, employment, family, household, and certain organizational eligibility options. BECU’s current eligibility page also mentions a $1 or more BECU Foundation donation path tied to visiting the North Charleston Neighborhood Financial Center for South Carolina eligibility. Verify the exact current membership route before applying.

Does BECU offer video banking?

Yes. BECU says video banking provides live assistance from home and can support membership applications, account openings, loan applications, and credit card applications.

What made Mario’s BECU profile strong?

Mario had 807 to 849 FICO scores, 1% to 3% utilization, over 20 clean tradelines, no late payments reporting, about $96,000 stated income, and a rebuilt BECU relationship.

Should you apply online or in branch with BECU?

For this strategy, in branch or video banking may be better than applying online because you can ask whether multiple products can be reviewed under one hard pull. Online applications may not combine products the same way.

Conclusion

Mario’s BECU approval was not luck.

It was preparation.

He rebuilt his credit.

He cleaned up old issues.

He reopened the relationship.

He kept utilization low.

He walked into the branch with a bankable profile.

Then he asked for more than one product under one pull.

The result was $34,000 in new credit exposure:

$19,000 credit card.

$15,000 personal line of credit.

One TransUnion hard pull.

That is how you use a credit union strategically.

Not by applying randomly.

Not by hoping.

Not by chasing approvals before your file is ready.

Build the profile.

Season the relationship.

Ask the right questions.

Maximize the pull.

And when the approval comes, use the credit like a tool, not a trap.