BCU Credit Union $55K Approval Strategy: One Hard Pull, Four Decisions

Jun 28, 2026

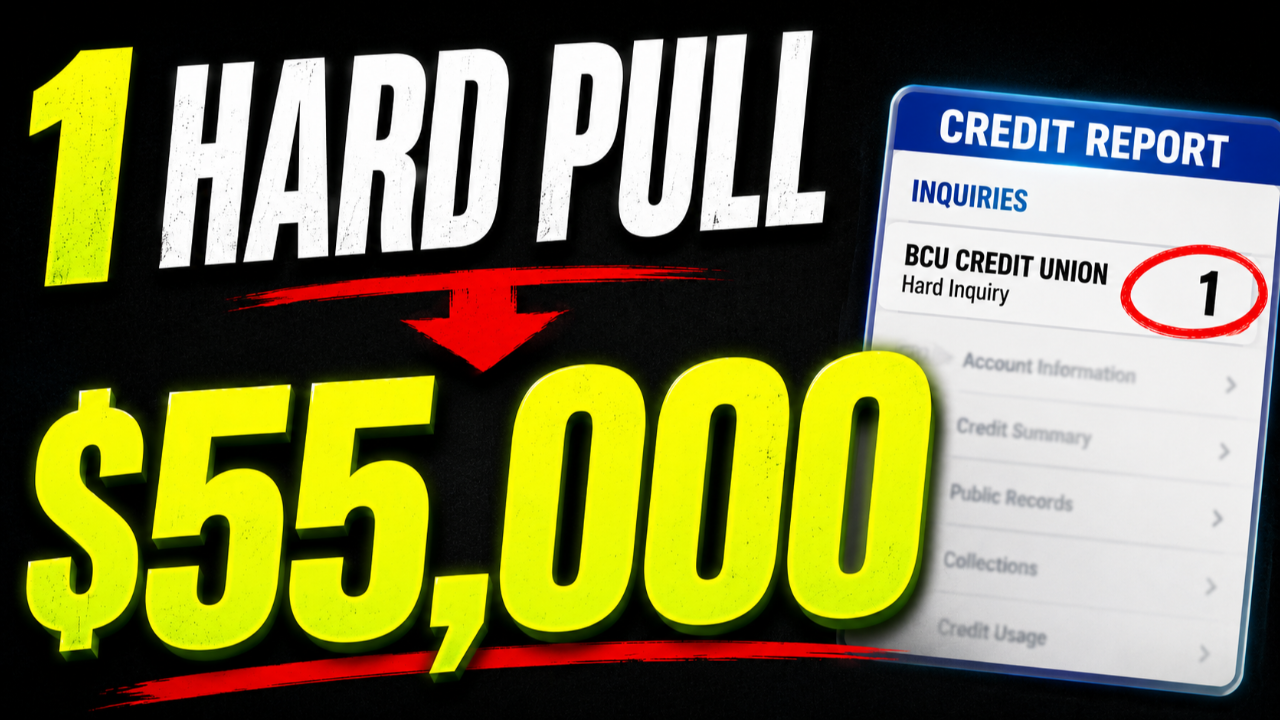

One BCU Credit Union member got approved for $55,000 in new unsecured credit plus an auto loan refinance with only one hard pull.

That is the part worth studying.

This was not just one approval.

It was four separate lending decisions inside the same credit review window:

-

A credit limit increase on an existing BCU card

-

A second BCU credit card

-

A BCU personal line of credit

-

An auto loan refinance

That is powerful because most people are used to banks treating every application like a separate event.

One card application.

One inquiry.

One loan application.

Another inquiry.

Another product.

Another inquiry.

But some credit unions operate differently. If your credit report is already pulled, they may be able to use that same report for multiple lending decisions during a short window.

That is exactly what makes this BCU data point so interesting.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

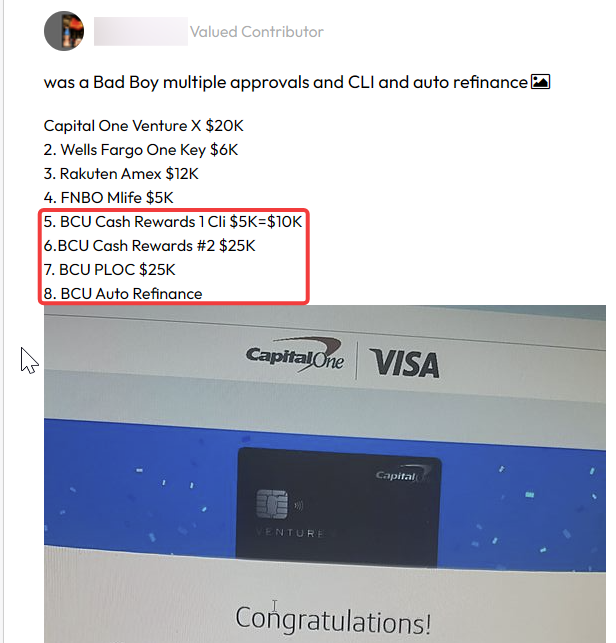

One BCU member reportedly turned one TransUnion hard pull into four lending decisions: a credit limit increase, a second credit card, a $25,000 personal line of credit, and an auto loan refinance. The member already had a BCU card with a $5,000 limit, which was increased to $10,000, and also received a new $25,000 BCU card and a $25,000 personal line of credit. This is a real data point, not a guaranteed result, and the missing piece is how much account activity or relationship seasoning happened before the applications.

What Happened With This BCU Approval

This person was not brand new to BCU.

They already had one BCU credit card with a $5,000 limit.

Then, during the same 30-day hard pull window, they were able to do four things:

-

Increase the original BCU card from $5,000 to $10,000

-

Open a second BCU credit card with a $25,000 limit

-

Open a BCU personal line of credit for $25,000

-

Refinance their auto loan through BCU

That means they added $55,000 in new unsecured credit:

-

$5,000 increase on the original card

-

$25,000 second credit card

-

$25,000 personal line of credit

Then they also refinanced the car loan.

One bureau pull.

Four lending decisions.

That is the type of credit union data point I pay attention to because it shows how much can happen when the lender is willing to evaluate the full relationship instead of treating every request as separate.

The BCU Membership Path Most People Miss

BCU is not usually thought of as a normal nationwide credit union.

Many people assume you need to live or work in certain areas, qualify through an employer group, or have a traditional connection.

But BCU also has a Life. Money. You. membership path.

That matters because Life. Money. You. can make people eligible for BCU membership even if they do not live in BCU’s main geographic footprint or work for a partner employer.

That is the overlooked part.

A credit union that looks restricted at first glance may still have an alternative membership path.

Helpful resource: If you like credit union data points like this, my 150+ Credit Unions Anyone Can Join Database can help you find more credit unions with accessible membership paths: https://courses.calbartoncashback.com/CreditUnions

What We Know About the Member’s Credit Profile

Here is what I was able to confirm from the data point:

-

Around a 750 TransUnion score

-

Low credit card utilization

-

Very few recent inquiries

-

TransUnion was the bureau pulled

-

Existing BCU relationship with one credit card already open

That is a strong profile.

Not perfect.

But strong enough to make the approvals believable.

The most important detail is that they already had a BCU card before this happened.

That means BCU was not looking at a completely unknown person.

There was already an account on file.

That matters.

What We Do Not Know

This is where people need to be careful.

We do not know exactly how they used the BCU account before the approval spree.

We do not know if they had deposits.

We do not know if they had regular transactions.

We do not know if they kept money sitting in checking or savings.

We do not know if they had direct deposit.

We do not know if the existing credit card had steady usage.

That missing information matters.

It would be a mistake to look at this data point and assume:

Open BCU account today.

Wait a short time.

Apply for everything.

Get approved for $55,000.

That is not what we can prove.

All we know is that the approvals happened inside the same credit review window and that the member already had an existing BCU relationship.

Why Credit Unions Sometimes Allow Stacked Approvals

Many big banks treat every application like a separate risk event.

Credit card application?

New decision.

Personal loan?

New decision.

Auto refinance?

New decision.

Credit limit increase?

New decision.

Many credit unions can be more relationship-based.

Once they pull your credit, they may look at the full picture and decide how much total exposure they are comfortable giving you.

That is why you sometimes see credit union members get multiple approvals off one credit pull.

From your perspective, it feels like you stacked applications.

From the credit union’s perspective, they may simply be evaluating how much they are comfortable lending to one member during the same underwriting review.

That is a very different model than a large national bank.

The Real Lesson: Exposure Matters

The most important word here is exposure.

A lender is not just asking:

“Can we approve this one card?”

They are asking:

“How much total risk are we willing to take on this person?”

In this BCU data point, the credit union was comfortable with:

-

A higher limit on the first card

-

A second card

-

A personal line of credit

-

An auto refinance

That means the member’s profile supported more total exposure.

This is why low utilization and few inquiries matter.

A clean profile gives the lender more room to say yes.

If the person had high balances, recent missed payments, or a lot of new accounts, the result could have looked completely different.

Why the Existing BCU Card Helped

The existing BCU card is a major part of the story.

This was not a cold application.

The member already had a $5,000 BCU card.

That means BCU had at least some history with them.

They could see account behavior.

They could see payment behavior.

They could see whether the member handled the first card responsibly.

That does not guarantee anything.

But it helps explain why BCU may have been comfortable expanding the relationship.

A lot of people want the big approval first.

Sometimes the smarter move is to get in with the credit union, manage the first account well, then expand later.

How I Would Season the BCU Account First

Since we do not know exactly how this member used the account before applying, I would take the safer route.

I would make the relationship look real before asking for multiple products.

That means opening checking and savings, funding the accounts, and letting them show normal activity.

You do not need to look rich.

You need to look predictable.

Banks and credit unions like patterns they can understand.

My BCU Seasoning Strategy

If I were trying to build a BCU relationship before applying, I would keep it simple.

First, I would open checking and savings.

Then I would fund the accounts right away.

A minimum deposit may be enough to open the account, but ideally I would keep at least $1,000 sitting there consistently if possible.

Then I would let the account behave like a real personal account for 30 to 60 days.

Weekly activity could include:

-

1 to 2 debit card purchases

-

1 to 5 ACH deposits or transfers in

-

1 to 2 outgoing payments

-

Occasional utility, subscription, or credit card payments

Balance behavior matters too.

I would avoid letting the account sit near zero.

I would avoid depositing money and immediately pulling all of it back out.

I would try to keep a stable average balance.

I would also log in periodically and use the account like it actually matters.

The goal is not to trick the credit union.

The goal is to show normal financial behavior.

Why Predictability Matters to Credit Unions

Credit unions are still lenders.

They want to get repaid.

So when you ask them for unsecured credit, they want signals that you are stable.

Those signals can include:

-

Low utilization

-

Clean payment history

-

Few recent inquiries

-

Stable income

-

Existing membership relationship

-

Deposit activity

-

Responsible use of existing accounts

-

No signs of credit desperation

That last one is important.

If your report looks like you are chasing credit everywhere, the credit union may hesitate.

But if your profile looks clean and your relationship looks stable, they may be more open to increasing exposure.

Why One Hard Pull Can Be So Valuable

A hard inquiry is not the end of the world.

But it still matters.

If you can turn one credit pull into multiple useful lending decisions, that is a much better use of the inquiry.

That is the real play here.

Not just getting one approval.

Getting the most value from one underwriting event.

That could mean asking about:

-

A credit limit increase

-

A second card

-

A personal line of credit

-

A personal loan

-

An auto refinance

-

Other lending options you actually need

The key phrase is “actually need.”

Do not apply for products just because they are available.

Stacking approvals only makes sense when the products fit your financial plan.

What I Would Ask BCU Before Applying

Before attempting something like this, I would ask BCU a few direct questions.

I would ask:

-

How long is the credit report valid after a hard pull?

-

Can the same pull be used for multiple products?

-

Can I apply for a credit card and personal line of credit from the same pull?

-

Can a credit limit increase be considered from the same credit review?

-

Does an auto refinance require a separate pull?

-

Which credit bureau do you typically pull in my state?

-

Is there a maximum total exposure limit for unsecured products?

You may not get every answer.

Some representatives may not know.

Some policies may vary.

But asking gives you a better chance of understanding how to structure the applications.

Helpful resource: If you want to compare more pre-approval and soft-pull options before risking hard inquiries, my free Credit Card & Loan Pre-Approval Master List can help you plan smarter applications: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Who This BCU Strategy Makes Sense For

This kind of strategy makes the most sense for someone with a clean credit profile.

Ideally, you want:

-

Around a 700+ score

-

Low utilization

-

Few recent inquiries

-

No recent late payments

-

Stable income

-

A real reason for the products

-

Some relationship activity with the credit union

The member in this data point reportedly had around a 750 TransUnion score and low utilization.

That is not an accident.

A cleaner profile gives the credit union more room to approve multiple products.

Who Should Be Careful

You should be careful with this strategy if your credit profile is not ready.

If you have high utilization, recent late payments, lots of inquiries, or too many new accounts, trying to stack approvals could backfire.

You could waste the hard pull and get denied for multiple products.

You also need to be careful about taking on too much credit at once.

A $25,000 personal line of credit sounds great.

A second $25,000 card sounds great.

But access to credit is not the same thing as free money.

You still need discipline.

If you use the credit poorly, the approvals can turn into a problem.

Frequently Asked Questions

Can anyone join BCU Credit Union?

BCU has several membership eligibility paths, including employer, community, family, and Life. Money. You. eligibility. The Life. Money. You. path is the one that can make BCU more accessible to people outside the usual county or employer routes.

What credit bureau did BCU pull in this data point?

In this data point, BCU pulled TransUnion. That does not guarantee BCU will always pull TransUnion for every applicant, product, or state.

Can BCU use one hard pull for multiple products?

This data point suggests BCU used one hard pull during a 30-day credit review window for multiple lending decisions. You should verify the current policy with BCU before applying.

How much credit did this person get from BCU?

They received $55,000 in new unsecured credit: a $5,000 credit limit increase, a $25,000 second credit card, and a $25,000 personal line of credit. They also refinanced an auto loan.

Should you open a BCU checking and savings account before applying?

I would. It may not be required for every approval, but opening and using deposit accounts can help the relationship look more real before asking for multiple lending products.

How long should you season the account?

A practical starting point is 30 to 60 days of normal activity. That does not guarantee approval, but it gives the credit union more behavior to evaluate than an empty new account.

Final Thoughts

This BCU data point is powerful because it shows what can happen when a credit union is willing to evaluate the full member relationship.

One hard pull turned into:

-

A higher limit on an existing card

-

A new $25,000 credit card

-

A $25,000 personal line of credit

-

An auto loan refinance

That is not normal with most big banks.

But it can happen with credit unions when the profile is strong, the relationship exists, and the timing is right.

The smart move is not to rush in and apply for everything blindly.

The smart move is to join correctly, season the account, keep your credit profile clean, ask how their credit review window works, and then apply strategically.

Banks and credit unions do not approve chaos.

They approve patterns.

If your profile looks predictable, low-risk, and worth expanding, your odds of getting meaningful approvals can improve dramatically.