6 Banks Giving Small Business Owners $10K+ Credit Card Limits

Jun 30, 2026

Over the past 60 days, I found 6 banks handing out business credit card starting limits over $10,000.

And yes, some of these approvals came from newer businesses.

That matters.

Because a lot of small business owners assume they need years of tax returns, 12 months of bank statements, perfect business credit, and a fully built company before a bank will approve them for real business credit.

Not always.

Some banks are still approving strong applicants for high-limit business credit cards based on a mix of personal credit, business revenue, existing relationships, low utilization, and clean recent activity.

The key is knowing which banks are active right now — and what kind of profile they seem to like.

Quick Answer

Bank of America, Chase, U.S. Bank, Citi, American Express, and Wells Fargo all have recent business credit card data points showing starting limits over $10,000. Approval is not automatic, and each bank has its own style: Bank of America and U.S. Bank can reward clean profiles and relationships, Chase likes strong credit and low recent inquiries, Citi can be useful if your Equifax report is cleaner, Amex may approve existing customers with a soft-pull data point, and Wells Fargo has recent Signify Business Cash approvals even for newer businesses. Bureau pulls, limits, offers, and documentation can vary by state, product, profile, and timing.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Helpful resource: If you want to research business credit cards with 0% APR offers, bureau-pull data points, and recent approval patterns, my 0% APR Business Credit Card Database can help you compare banks before applying.

Why $10K+ Business Credit Limits Matter

A $10,000 business credit card limit is not just a number.

For a small business owner, it can help with:

-

Inventory

-

Ads

-

Equipment

-

Software

-

Travel

-

Contractor payments

-

Shipping

-

Supplies

-

Cash-flow timing

-

Startup expenses

But it can also create problems if you use it recklessly.

Business credit is leverage.

Used correctly, it can help you grow.

Used emotionally, it can turn into expensive debt fast.

That is why the goal is not just “get approved.”

The goal is to get approved with a bank that fits your profile and gives you credit you can actually manage.

What These 6 Banks Have in Common

The banks in this article are different, but the successful applicants had several things in common.

They usually had:

-

Strong personal credit

-

Low utilization

-

Few recent inquiries

-

Existing bank relationships

-

Solid comparable credit limits

-

Clean payment history

-

Real business revenue or realistic business activity

-

Good timing

-

The right application order

That last one matters.

If you are going after multiple business cards, order matters.

Some banks are more inquiry-sensitive than others.

Some pull different bureaus.

Some like existing relationships.

Some care more about revenue.

Some are more forgiving of older negatives.

The strategy is not random.

Bank #1: Bank of America

Bank of America is one of the first banks I would look at for business funding if you already have a strong relationship with them.

Why?

Because Bank of America can be generous when your profile is clean and they already know you.

Their business credit cards may not always have the longest 0% APR offers compared to some competitors, but they can still be powerful because of high-limit data points, relationship value, and the possibility of applying for more than one product strategically.

What Makes Bank of America Stand Out

Bank of America business cards can be attractive because:

-

They have multiple business card options

-

They may pull TransUnion in some data points

-

Existing relationships can help

-

Personal card history may support business approvals

-

Some people report multiple approvals with one hard pull

-

High starting limits are possible with strong files

The biggest theme with Bank of America is relationship.

If you already have personal cards, business checking, personal checking, savings, or prior history with Bank of America, that may help your business application look stronger.

It does not guarantee approval.

But it can help.

Bank of America Data Point: $35K Starting Limit

One applicant reported a strong Bank of America business card approval:

$35,000 starting limit.

They had:

-

A 2-year-old LLC

-

FICO score in the 820s

-

Strong personal credit

-

Existing Bank of America success on the personal side

-

Business checking and savings opened online

-

No major paperwork drama

That is the kind of profile banks love.

High score.

Clean file.

Real business age.

Existing relationship.

No chaos.

Why This Bank of America Approval Worked

The approval likely worked because the applicant looked low risk.

The business was not brand new.

The personal credit score was excellent.

The relationship with Bank of America already existed.

And the applicant did not appear to be credit-hungry.

Two things can kill business card approvals fast:

-

Too many recent inquiries

-

Identity verification problems

If your name, address, business name, or documents do not match cleanly, the application can slow down or get denied.

Before applying, make sure your identity details are consistent.

Have your driver’s license, utility bill, business documents, EIN letter, and address history ready if needed.

Bank of America Double-Dip Strategy

One of the more interesting Bank of America strategies is applying for two business cards close together.

One data point said:

-

First card approved as sole proprietor using SSN

-

Second card approved under EIN about 26 hours later

-

One TransUnion personal inquiry

-

First approval: $15,000

-

Second approval: $15,000

That is $30,000 in business credit from one reported inquiry.

That is powerful.

But do not treat it as guaranteed.

Double-dip strategies can change quickly.

Banks can split pulls.

Applications can go pending.

Manual review can happen.

Internal exposure limits can stop the second approval.

Why the Double-Dip Worked

This applicant had major strengths:

-

Two Bank of America personal cards

-

One personal card with about 20 years of history

-

Existing business credit card

-

Personal and business checking accounts

-

Significant deposits

-

Business EIN around 4 years old

-

Stated business income around $90,000

-

Six-figure personal income

-

Average age of accounts around 16 years

-

Strong credit mix

That is not a weak profile.

That is a well-seasoned borrower using a well-planned strategy.

Bank #2: Chase

Chase is one of the strongest banks in the business credit card world.

The Ink lineup is popular for a reason.

Chase business cards can offer strong welcome bonuses, 0% APR offers, and useful rewards.

But Chase is not a bank I would approach casually.

They can be sensitive to recent accounts and inquiries.

If you are planning a business card strategy, Chase is often one of the banks to hit early — before your reports get crowded.

What Makes Chase Stand Out

Chase stands out because:

-

Ink cards are strong business products

-

Welcome bonuses can be valuable

-

0% intro APR offers can help with business expenses

-

Strong limits are possible

-

Existing Chase relationships can help

-

Some people receive “already approved” offers in their Chase account

Chase may not always require an existing relationship.

But having one can make a big difference.

If Chase already trusts you with personal cards, strong limits, and clean payment history, your business application may have a better shot.

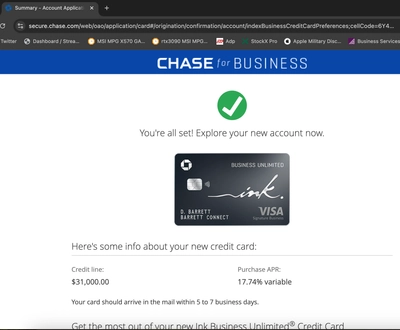

Chase Data Point: $31K Instant Approval

One applicant reported:

Instant approval for $31,000.

This was their first Chase business card.

That is a serious starting limit.

Why This Chase Approval Worked

The applicant had several strengths.

First, they kept seeing “You’re already approved” offers for Ink Cash, Ink Unlimited, and Ink Premier inside their personal Chase account.

Those offers can be very strong signals.

They are not the same as “no hard pull,” and they are not a magical guarantee for every person.

But if Chase is showing you targeted already-approved business offers, that is a serious green light.

Second, the applicant had a strong Chase relationship:

-

Amazon card: $18,000 limit

-

United Club Infinite: $16,300 limit

-

Sapphire Reserve: $31,000 limit

That shows Chase already trusted them with high personal limits.

Third, the credit profile was strong:

-

FICO score over 800

-

About 5% credit usage

-

Personal income around $160,000

-

Business revenue around $90,000

-

About 2.5 years of business credit history

That is the kind of file Chase can say yes to.

How to Approach Chase

If you want a Chase business card, timing matters.

I would think about:

-

Recent inquiries

-

5/24 position

-

Existing Chase relationship

-

Personal card limits

-

Utilization

-

Business revenue

-

Business age

-

Whether Chase is showing targeted offers

If your file is clean and Chase is showing strong offers, that can be a good time to move.

If your file is loaded with recent accounts and inquiries, Chase may be less forgiving.

Bank #3: U.S. Bank

U.S. Bank is not always the loudest bank in the room.

But for strategic business credit, it is one of the most important banks to watch.

U.S. Bank can be conservative.

They can be inquiry-sensitive.

They may not always hand out giant limits to everybody.

But when your profile fits, they can approve strong business limits with valuable 0% APR offers.

The U.S. Bank Triple Cash Rewards Visa Business Card currently offers 0% intro APR on purchases and balance transfers, along with no annual fee and business-friendly cash back categories.

What You Need to Know About U.S. Bank

U.S. Bank tends to like:

-

Clean credit reports

-

Low recent inquiries

-

Low utilization

-

Existing relationship

-

Stable income

-

Strong comparable limits

-

Good timing

The big warning with U.S. Bank is inquiry sensitivity.

If you have been applying everywhere, U.S. Bank may not love that.

I would want fewer than 3 inquiries in the past 6 months before applying, and preferably even cleaner if possible.

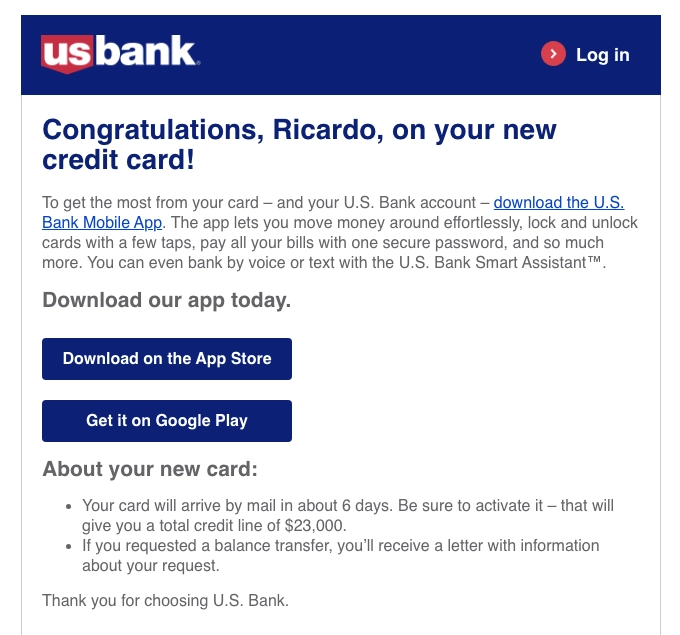

U.S. Bank Data Point: $23K Starting Limit

One applicant reported:

They started a personal relationship with U.S. Bank first by getting the personal Visa Cash+ card.

Then they opened a Smartly Checking account.

Then they applied for the U.S. Bank Triple Cash Rewards Visa Business Card.

Result:

$23,000 starting limit.

No docs.

No approval delay.

Why This U.S. Bank Approval Worked

This strategy worked because the applicant did not go in cold.

They built a relationship first.

They got a personal card.

They opened checking.

Then they applied for the business card.

That makes the business application look less random.

U.S. Bank already had context.

That can matter with a conservative lender.

U.S. Bank and Elan Financial

One thing people forget is that U.S. Bank owns Elan Financial Services.

Elan underwrites credit card programs for many local banks and credit unions.

That means if you already have several Elan-backed cards, U.S. Bank may be aware of that exposure.

This can matter for business credit.

If a bank thinks you already have enough exposure through related platforms, it may limit your starting credit or deny additional credit.

That does not mean you should avoid U.S. Bank.

It just means you need to understand the ecosystem.

Bank #4: Citi

Citi is not always the first bank people mention for business credit cards.

But Citi can still be useful.

The biggest reason?

Citi has Equifax pull data points.

That matters because many major business card issuers lean heavily on Experian.

If your Experian report is crowded with inquiries but Equifax is cleaner, Citi can become more interesting.

Citi’s Limitations

Citi’s business card lineup is limited compared with Chase, Amex, or Bank of America.

Citi is not the strongest option if you want a huge menu of business cards or long 0% APR business financing.

But Citi can still make sense if:

-

You want a travel-focused business card

-

You have a Citi relationship

-

Your Equifax report is clean

-

You have strong comparable credit limits

-

You want to diversify beyond Chase and Amex

Citi is not the flashiest business card bank.

But the right profile can still get a strong approval.

Citi Data Point: $16K Starting Limit

One applicant reported receiving several “pre-selected to apply” emails from Citi and seeing a pre-selected offer inside their Citi account.

They applied for the business version and received:

Instant approval for $16,000.

That is a solid business starting limit.

Pre-Selected Does Not Mean Pre-Approved

This is important.

Pre-selected does not mean guaranteed approval.

A pre-selected offer can be based on general marketing criteria.

It does not always mean Citi already fully underwrote you.

It does not always mean a soft pull happened.

It does not always mean you will be approved.

So treat pre-selected offers as a signal.

Not a promise.

Why the Citi Approval Worked

This applicant had several things going for them.

First, they had an existing Citi relationship:

-

Citi Custom Cash for about one year

-

Citi Strata Premier for about three months

Second, they had excellent comparable credit:

-

13 credit cards

-

Navy Federal Flagship with a $40,000 limit

-

Navy Federal More Rewards with a $30,000 limit

-

Chase Sapphire Reserve with a $26,300 limit

That matters.

Banks like seeing that other issuers already trust you with big limits.

Third, their FICO score was in the 780s.

That is a strong file.

This was not a weak applicant getting lucky.

It was a strong applicant using a less crowded bureau and an existing relationship.

Bank #5: American Express

Amex is one of the most important banks for business credit cards.

Why?

Because Amex can be flexible, relationship-driven, and forgiving when the current profile is strong.

Amex also has one major advantage:

Existing Amex customers often report soft-pull approvals on additional Amex cards.

That can be huge.

No new hard inquiry.

No inquiry score drop.

No extra inquiry clutter.

But be careful.

Do not treat “existing Amex customer = guaranteed soft pull” as a law.

It is a very common data point, but Amex can still perform credit checks depending on the application and profile.

What Makes Amex Stand Out

Amex stands out because:

-

Strong business card lineup

-

Blue Business Plus and Blue Business Cash are popular starter options

-

Existing relationship can help

-

Soft-pull approval data points are common for existing customers

-

Amex may be more forgiving of older negative marks

-

Business limits can be stronger than personal Amex limits

Amex is often one of the best banks to build with early because the ecosystem can reward relationship.

Amex Data Point: Blue Business Plus $10K Approval

One applicant reported:

Amex Blue Business Plus approval with a $10,000 starting limit.

It was their first business credit card.

They already had a personal Amex Blue Cash Everyday card with an $18,000 limit that had been open for about 1 year and 10 months.

The approval was reportedly a soft pull.

Why the Amex Approval Worked

The applicant had:

-

Existing Amex relationship

-

Personal Amex card with strong limit

-

Only 1 inquiry in the past 6 months

-

2% utilization

-

FICO score in the low to mid-700s

-

Six late student loan payments from about five years ago

That last part matters.

The report was not perfect.

But the negatives were older, and the current profile looked strong.

Banks care about recent behavior.

A late payment from five years ago is not the same as a late payment from five months ago.

Amex looked at the bigger picture.

Why Amex Can Work With Older Negatives

Amex can be more forward-looking than people expect.

If your old mistakes are truly old, and your current profile is clean, you may still have a shot.

That means:

-

Low utilization

-

Clean recent payments

-

Low inquiries

-

Existing Amex relationship

-

Strong income

-

Responsible card usage

Older lates can still hurt.

But they do not always block approval forever.

That is the lesson.

Bank #6: Wells Fargo

Wells Fargo was not always at the top of my business credit card list.

But the recent approval data points have made it harder to ignore.

The Wells Fargo Signify Business Cash Card is a simple business cash back card that earns unlimited 2% cash rewards on qualified purchases and has no annual fee.

That is strong.

No confusing categories.

No cap on 2% cash rewards mentioned on the public page.

No annual fee.

For business owners who want simple cash back, that is worth paying attention to.

Why Wells Fargo Is Getting Attention

Wells Fargo is interesting because recent data points show approvals for:

-

Newer businesses

-

In-branch applications

-

Online applications

-

Applicants with thick credit files

-

Applicants with existing Wells Fargo checking

-

Applicants with older serious credit negatives

That does not mean Wells Fargo is easy.

But it does mean they may be worth considering if your profile fits.

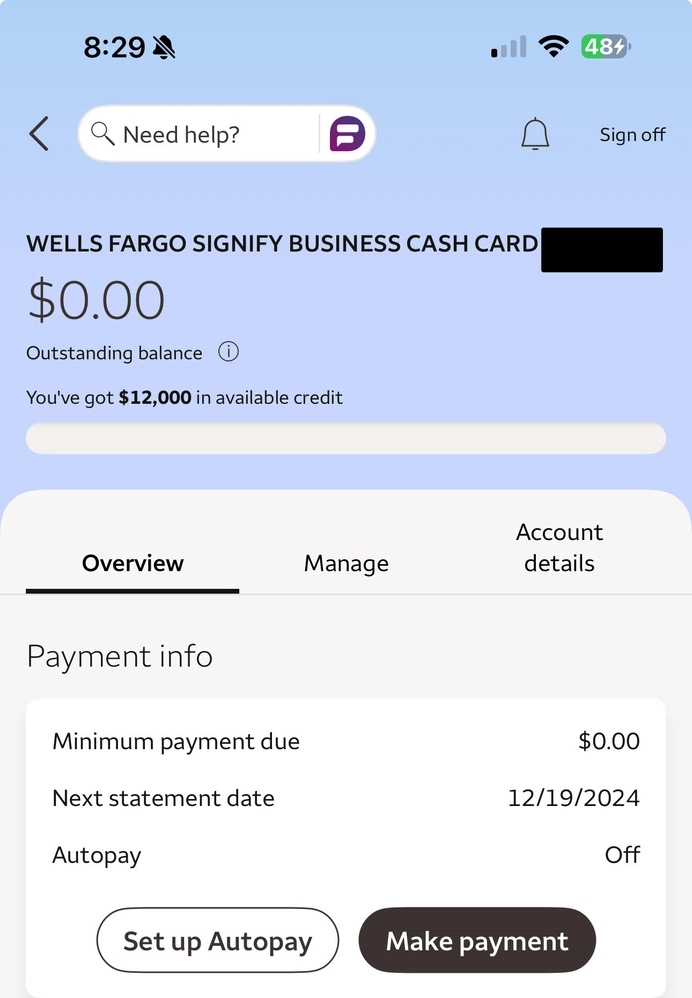

Wells Fargo Data Point #1: $12K Approval

One applicant applied online and received a message that the application was under review or verification.

They called the business line.

An agent asked a few questions.

Then they were approved with a:

$12,000 limit.

Why This Wells Fargo Approval Worked

This applicant had:

-

Wells Fargo checking opened about two months earlier

-

15 personal credit cards

-

Personal limits up to $25,000

-

6 business cards

That is a thick credit profile.

Wells Fargo had a lot of history to evaluate.

The existing checking relationship likely helped too.

Again, relationship matters.

Wells Fargo Data Point #2: $12K In-Branch Approval

Another applicant went into a Wells Fargo branch to apply for the Signify Business Cash card.

The application went pending in branch.

About 30 minutes later, the banker sent the approval notification.

Starting limit:

$12,000.

The applicant was able to add the card to their mobile wallet the next day.

Why This Wells Fargo Approval Worked

This applicant had:

-

Zero inquiries in the past 6 months

-

Zero new accounts in the past 6 months

-

FICO score over 800

-

In-branch application

-

Business banker support

That is exactly the kind of profile banks like.

Clean.

Stable.

Low risk.

And the in-branch application likely helped move things along.

Wells Fargo Data Point #3: Approved After Chapter 7

One of the most surprising data points involved a business owner who reported a $12,000 approval even though they had a Chapter 7 bankruptcy filing about 2.5 years earlier.

Even more surprising:

The LLC was reportedly filed the same month.

That is not a normal approval.

But it shows Wells Fargo may be willing to consider more than just one negative mark if the rest of the profile supports the application.

Why This Wells Fargo Approval Is Important

A bankruptcy is one of the worst items you can have on a credit file.

But time matters.

Current behavior matters.

Relationship matters.

Underwriting context matters.

The data point suggested the applicant may have repaid Wells Fargo during the bankruptcy process, which could have helped internally.

That part needs verification.

But the bigger lesson is useful:

A serious negative does not always mean every bank is permanently closed to you.

It just means your strategy needs to be tighter.

What These 6 Banks Teach Us

These data points all point to the same truth.

High-limit business approvals usually do not happen by accident.

They come from some combination of:

-

Clean personal credit

-

Low utilization

-

Strong income

-

Business revenue

-

Business age

-

Existing bank relationships

-

Strong comparable credit limits

-

Low inquiry activity

-

Correct application timing

-

Knowing which bureau the bank may pull

You do not need perfection.

But you do need a profile that makes sense.

Which Bank Should You Try First?

Here is how I would think about it.

Try Chase early if:

-

You are under 5/24

-

Your Experian is clean

-

You have low recent inquiries

-

You have Chase relationship offers

-

You want strong bonuses and 0% APR

Try Bank of America if:

-

You already have a BofA relationship

-

Your TransUnion is clean

-

You have strong deposits or long history

-

You want to try for multiple business cards strategically

Try U.S. Bank if:

-

Your TransUnion is clean

-

You have few recent inquiries

-

You are willing to build a relationship first

-

You want long intro APR options

Try Citi if:

-

Your Equifax is cleaner than Experian

-

You already have Citi personal cards

-

You want a travel-focused business card

-

You have strong comparable limits

Try Amex if:

-

You already have a personal Amex card

-

You want possible soft-pull data points

-

Your current utilization is low

-

You want business cards that may not add new hard inquiries

Try Wells Fargo if:

-

You want simple 2% business cash back

-

You have a Wells Fargo relationship

-

You have low recent credit activity

-

You want to apply in branch with banker support

What to Do Before Applying

Before you apply for any high-limit business credit card, clean up the file.

Check:

-

Personal FICO scores

-

Utilization

-

Recent inquiries

-

New accounts

-

Existing bank relationships

-

Business revenue

-

Business age

-

Business address

-

EIN records

-

Application details

-

Personal guarantee terms

-

Whether the card reports to personal credit

Do not apply just because you saw a big approval data point.

Ask yourself:

Does my profile look like that profile?

If not, fix the weak spots first.

Frequently Asked Questions

What banks give high-limit business credit cards?

Recent data points show $10K+ business credit card approvals from Bank of America, Chase, U.S. Bank, Citi, American Express, and Wells Fargo. Limits vary based on credit profile, income, business revenue, relationship history, and underwriting.

Can a brand-new business get a $10K+ business card?

Yes, it can happen. Wells Fargo and Chase data points show newer businesses getting strong approvals. But brand-new businesses usually need strong personal credit, low utilization, low inquiries, and a credible application.

Which bank is best for a first business credit card?

Chase, Amex, and Wells Fargo can all be strong starter options depending on your profile. Chase is popular for Ink cards, Amex is strong for existing Amex customers, and Wells Fargo Signify is simple with unlimited 2% cash rewards.

Do business credit cards require proof of income?

Not always. Some approvals happen without bank statements, tax returns, or profit and loss documents. But banks can request documents at any time, especially for larger limits, manual reviews, or higher-risk profiles.

Which business credit card banks may use soft pulls?

Existing Amex customers often report soft-pull approvals on additional Amex cards, including business cards. But this is not guaranteed. Amex’s official Apply With Confidence flow can use a soft credit check before acceptance when available.

Should I apply for multiple business cards at once?

Be careful. Some banks are inquiry-sensitive, and applying in the wrong order can hurt approvals. If you are stacking business cards, research bureau pulls, timing, issuer rules, and whether same-day applications may combine inquiries.

Conclusion

These 6 banks are worth watching if you want high-limit business credit cards.

Bank of America can reward strong relationship profiles.

Chase is still one of the best business card issuers in the game.

U.S. Bank can be powerful if your file is clean and your timing is right.

Citi can be useful if your Equifax report is stronger than Experian.

Amex can be one of the best ecosystems for existing customers.

And Wells Fargo is showing enough recent Signify Business Cash approvals that it deserves attention.

But do not copy data points blindly.

Use them as clues.

Look at the profile behind the approval.

Look at the relationship.

Look at the bureau pull.

Look at the utilization.

Look at the timing.

That is how you stop applying randomly and start applying strategically.

The goal is not just more business credit.

The goal is smarter business credit.