3 Banks That May Approve a New LLC for $20,000 in Business Credit Without Proof of Income

Jun 29, 2026

Getting business credit for a new LLC sounds impossible when every lender acts like they need your entire life story.

Some banks want 12 months of bank statements.

Some want two years of tax returns.

Some want profit and loss statements, business financials, revenue verification, and enough paperwork to make you question why you even started the business.

But not every bank works that way.

There are business credit cards that may approve a new LLC for $20,000 or more in credit without asking for proof of income. That means no tax returns, no bank statements, and no formal revenue documents in many cases.

And the best part?

Some of these cards also come with 0% intro APR offers, which can give you over a year to invest in your business without paying interest.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Some banks may approve a new LLC for $20,000 or more in business credit without proof of income, especially if you have strong personal credit, low recent inquiries, high existing limits, and a prior relationship with the bank. Chase, U.S. Bank, and American Express all have strong data points for new or newer businesses. Your result may vary based on your credit profile, business structure, relationship with the bank, stated revenue, and current underwriting rules.

Can a New LLC Really Get $20,000 in Business Credit?

Yes, a new LLC can get approved for $20,000 or more in business credit.

But let’s be clear.

The bank is not approving you just because your LLC exists.

When your business is new, the bank usually leans more heavily on your personal credit profile. That means your personal FICO score, credit card limits, payment history, inquiries, new accounts, utilization, and relationship with the bank can all matter.

This is why someone with a brand-new LLC but a strong personal credit profile can sometimes get a huge business credit limit without showing business income documents.

The lender may ask for basic business verification, like your articles of organization. But in many cases, they may not ask for bank statements, tax returns, or formal proof of business revenue.

That is what makes these cards so powerful.

Why 0% APR Business Credit Cards Matter

A 0% intro APR business credit card can be one of the best funding tools for a new business.

You can use the card for startup costs, inventory, equipment, software, ads, travel, supplies, or other business expenses. Then, during the intro period, you can pay the balance down without interest.

That gives you breathing room.

But do not confuse 0% interest with free money.

You still have to repay the balance. And if you miss payments, max out the card, or carry the balance past the promo period, the strategy can backfire.

Used correctly, 0% APR business cards can be powerful.

Used recklessly, they can become expensive fast.

Helpful resource: If you are comparing 0% APR business credit cards for startup funding or credit card stacking, my 0% APR Business Credit Card Database can help you find cards that match your funding strategy.

1. Chase Business Credit Cards

Chase is one of my favorite banks on the business side.

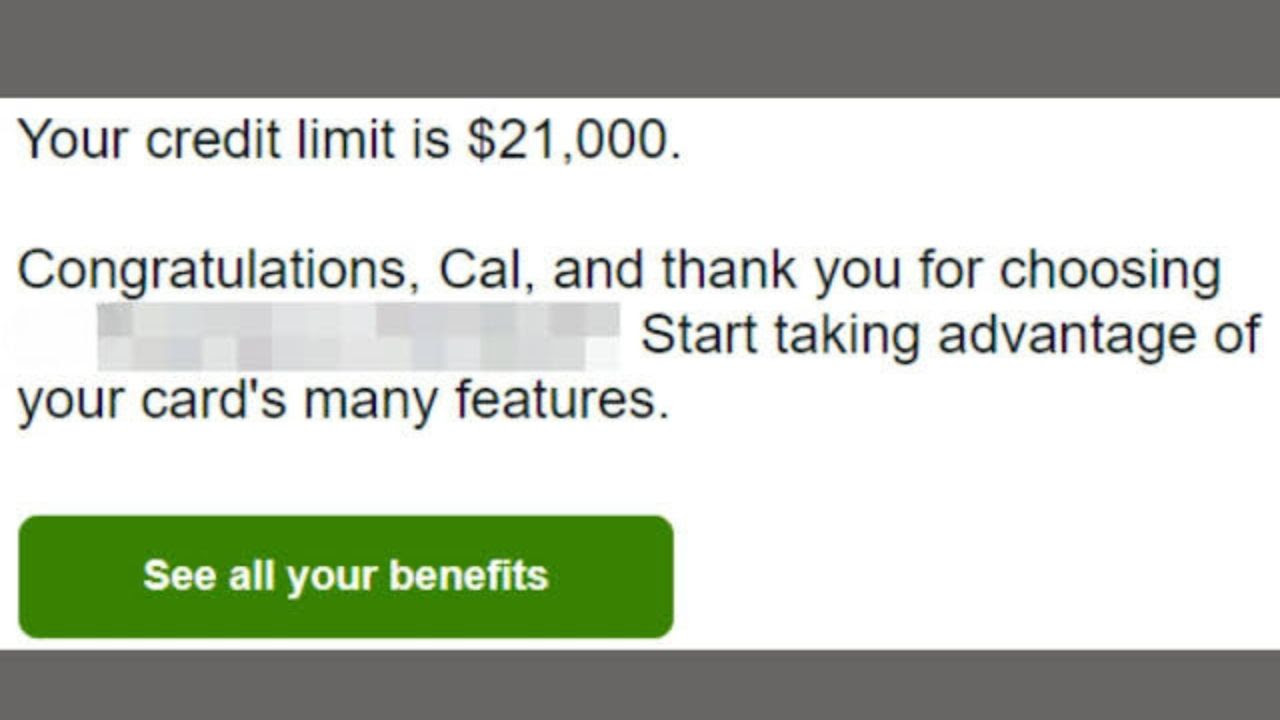

I got approved for the Chase Ink Business Unlimited with a $21,000 starting limit in September 2023.

At the time, my LLC was only about 3 weeks old.

That matters because a lot of people think their business needs to be old, established, and loaded with revenue before Chase will approve them.

That was not my experience.

My Chase Ink Business Unlimited Approval Data Point

When I re-established Barton Media LLC in North Carolina, it was basically a fresh start.

I had dissolved the same business in New York and formed the new LLC in North Carolina. So on paper, the business was brand new.

Here was my profile at the time:

New LLC was around 3 weeks old

Personal FICO score was around 770

Average personal credit limit was around $15,000

Only 3 opened credit card accounts in the past 24 months

Existing Chase Freedom Unlimited card with a $6,400 limit

Target card was the Chase Ink Business Unlimited

I applied because the Chase Ink Business Unlimited had a huge intro bonus at the time.

I did not get instant approval.

Instead, I got the classic message saying Chase would review my application and get back to me.

That message always makes your stomach drop because Chase can be strict.

The next day, Chase asked me to submit a copy of my business articles of organization. I sent it in and waited.

About 7 to 8 days later, I got an email saying the card was approved.

A few days after that, I got the welcome email showing my credit limit: $21,000.

That is still my largest business credit card limit.

What Chase Asked For

Chase did not ask me for bank statements.

Chase did not ask me for tax returns.

Chase did not ask me for profit and loss statements.

They only asked for a copy of my articles of organization.

That is what makes this data point so important. My LLC was extremely new, but Chase still approved me for a strong limit with minimal documentation.

They did hard pull my Experian credit report for the approval.

Why I Think Chase Approved Me

A big factor was likely my existing Chase relationship.

I already had a Chase Freedom Unlimited on the personal side with a $6,400 limit.

I also analyzed over 100 Chase customer data points and found that 80% of people with $20,000 or higher starting limits had a prior relationship with Chase.

That does not mean a Chase relationship guarantees approval.

But it can absolutely help.

Chase already knows how you manage credit. If you have a clean payment history, low utilization, and a strong profile, that prior relationship may make Chase more comfortable giving you a larger business credit line.

My 3/24 status also helped.

Chase is known for being sensitive to recent accounts, so being under 5/24 can matter a lot.

Why Chase Business Cards Are Valuable

Chase business cards are some of the most valuable business cards out there.

They can offer strong intro bonuses, useful rewards, and 0% intro APR periods on certain cards.

That makes them powerful for new businesses that need to buy equipment, pay for ads, cover software, or float expenses during the early growth stage.

Another huge benefit is that Chase business cards usually do not report normal account activity to your personal credit report.

That means the balance usually does not hurt your personal utilization as long as the account stays in good standing.

For business owners trying to grow available credit while protecting personal credit, that is a big deal.

Can You Apply for Chase Business Cards as a Sole Proprietor?

Yes, many people apply for Chase business cards as sole proprietors.

You do not always need a formal LLC to apply for a business card.

If you have a real business activity, side hustle, freelance work, resale business, consulting income, content business, or other legitimate business purpose, you may be able to apply as a sole proprietor.

But do not get it twisted.

An LLC is usually better for long-term business funding.

A sole proprietor setup can be a fast short-term solution, but an LLC gives you more structure and can open the door to more business funding options later.

2. U.S. Bank Business Credit Cards

U.S. Bank has one of the few business cards with 0% intro APR for up to 18 months.

That is nuts.

For a business owner, 18 months at 0% can be a serious funding window.

If you are buying equipment, covering marketing, investing in inventory, or smoothing out cash flow, that extra time can make a major difference.

But U.S. Bank can also be conservative.

They care about your personal profile, your relationship, and your overall risk.

U.S. Bank Triple Cash Approval Data Point

One strong data point involved someone applying during an application spree and getting approved for the U.S. Bank Triple Cash with an $18,000 starting limit.

Here was their profile before applying:

FICO 8: Experian 804, Equifax 815, TransUnion 818

FICO 9: Experian 823, Equifax 801, TransUnion 830

New accounts: 0/6, 0/12, 2/24

Inquiries: low recent inquiry activity

Utilization: around 4% to 5%

Declared household W2 income: $137,000

Declared business revenue: $130,000

Strong personal credit limits

Around $250,000 in business credit limits already

Total personal credit limits near $350,000

Existing U.S. Bank business checking relationship

Existing U.S. Bank business platinum card

They were instantly approved for:

U.S. Bank Triple Cash: $18,000

Navy Federal More Rewards: $7,100

Fidelity Rewards Visa: $25,000

All three pulls were on TransUnion.

This person knew what they were doing.

What Is an Application Spree?

An application spree is when someone applies for multiple credit cards in a short period of time.

The goal is usually to stack approvals, collect intro bonuses, and increase available credit quickly.

But this is not beginner strategy.

If you do this wrong, you can rack up hard pulls, trigger denials, and make banks think you are desperate for credit.

The person in this data point had a strong profile, low recent account activity, low utilization, high FICO scores, high personal limits, and strong business credit.

That is why the spree worked.

Why U.S. Bank Approved a Strong Limit

The $18,000 U.S. Bank Triple Cash approval likely came from a combination of factors.

They had:

High FICO scores

Low utilization

Strong personal credit limits

Good business revenue

Existing business credit limits

U.S. Bank relationship

Business checking account

Existing U.S. Bank business card

Even though their U.S. Bank business checking balance was only $0.11, the relationship still existed.

That is the part people miss.

A bank relationship does not always have to mean you have a huge balance sitting there. Sometimes just having the account open, seasoned, and connected to your profile can help.

Sole Proprietor vs LLC for U.S. Bank Business Cards

Like Chase, U.S. Bank may allow business card applications from sole proprietors.

That means you may not need a formal LLC to apply.

But an LLC is still the better long-term move if you are serious about business funding.

An LLC can help you:

Separate business and personal spending

Improve tax and accounting organization

Build business credit history

Access more corporate card options

Build business age over time

Look more professional to banks and lenders

A sole proprietor setup can work in the beginning, but it should not be your long-term funding foundation if you want larger business credit lines.

Helpful Resource: If you are building a business funding strategy and want the full foundation before applying, the Business Credit Buildout System is designed to help business owners prepare their profile for funding.

3. American Express Business Cards

Amex has one of the strongest business card lineups.

But one thing really stands out:

Amex has been handing out some insane business credit limits.

Several data points show Amex business cards getting approved with $20,000 to $25,000 starting limits, including the Amazon Business Prime Amex, Blue Business Plus, and Blue Business Cash.

Amex Business Prime Approval Data Points

One person applied for the Amex Amazon Business Prime card and was approved for $20,000.

They had an 811 FICO score and wanted to avoid personal accounts and hard pulls because they were considering a mortgage or construction loan.

Another data point showed an Amex Amazon Business Prime approval for $25,000.

Their profile included:

Starting limit: $25,000

Business revenue: $25,000

TransUnion personal score: 800

Soft pull so far

First business card

Card expedited for free

That is a crazy strong approval, especially with $25,000 in stated business revenue.

Pro tip: always ask the rep to expedite your credit card shipping. It never hurts, and they often say yes.

Amex Blue Business Plus and Blue Business Cash Data Points

Another person was approved for the Amex Blue Business Plus with a $25,000 starting limit.

They were shocked because they had two other Amex personal cards with starting limits under $10,000 and had not received credit limit increases on those cards in years.

This was their first business card.

Their FICO Experian 8 score in the Amex app was 752, and utilization was only 1%.

Another data point showed an Amex Blue Business Cash approval with a $25,000 starting limit and an instant soft pull approval.

That is what makes Amex so interesting.

People with good but not perfect profiles can sometimes get surprisingly strong business limits.

Why Amex Business Cards Are Powerful

The best thing about Amex is how they treat existing customers.

If you already have an Amex credit card, future Amex applications are often soft pulls.

That means after your first Amex card, you may be able to apply for additional Amex cards without hurting your credit score with a new hard inquiry.

That is huge.

It makes Amex one of the best banks for people who want to build business credit while protecting their personal credit profile.

But again, do not assume this is guaranteed forever.

Always check the application language before applying.

Why Amex May Give High Starting Limits

Amex seems willing to offer large business starting limits when the profile makes sense.

Factors that may help include:

Existing Amex relationship

Strong personal FICO score

Low utilization

Clean payment history

Stated business revenue

Strong personal credit management

Good internal Amex behavior

Low recent risk signals

The fact that multiple people received $25,000 starting limits is not a fluke.

Amex can be very generous when they like your profile.

What You Need Before Applying for Business Credit Without Proof of Income

If you want a real shot at $20,000 or more in business credit without proof of income, your profile needs to be ready.

Here is what I would focus on first:

Keep personal utilization low

Build higher personal credit limits

Avoid too many recent hard inquiries

Stay under major bank rules like Chase 5/24

Build relationships with target banks before applying

Open business checking accounts early

Keep business and personal finances separate

Use an LLC if you are serious about long-term funding

Make sure your business documents are clean and easy to verify

Be honest with stated business revenue

Banks may not ask for proof of income every time, but that does not mean you should make numbers up.

If a bank does ask for verification and your application does not match reality, you could get denied, shut down, or flagged.

How Bank Relationships Help With Business Credit Approvals

One of the biggest lessons across these data points is that relationships matter.

Chase relationship helped with my $21,000 approval.

U.S. Bank relationship likely helped with the $18,000 Triple Cash approval.

Amex relationship can help reduce hard pulls and improve future approval odds.

This is why I like opening accounts before I need funding.

A checking account, savings account, personal card, business card, or even small existing relationship can help the bank see you as an existing customer instead of a stranger.

That does not guarantee approval.

But it can move you from “unknown applicant” to “known customer.”

That can matter.

Frequently Asked Questions

Can a new LLC get approved for business credit cards?

Yes, a new LLC can get approved for business credit cards, especially if the owner has strong personal credit. Some banks may only require basic business verification, like articles of organization, instead of proof of income.

Do business credit cards require proof of income?

Not always. Some business credit card applications rely on stated income and personal credit instead of asking for tax returns or bank statements. But the bank can still request verification, so you should always provide accurate information.

Which banks approve new LLCs for high-limit business credit cards?

Chase, American Express, and U.S. Bank all have strong data points for business credit approvals. Approval depends on your credit profile, business revenue, relationship with the bank, and underwriting rules at the time you apply.

Do business credit cards hard pull personal credit?

Many business credit cards do hard pull personal credit. Chase and U.S. Bank commonly involve hard pulls based on the data points here. Amex may soft pull existing customers.

Can I apply for a business credit card as a sole proprietor?

Yes, many major banks allow sole proprietor applications. But if you are serious about long-term business funding, forming an LLC can give your business more structure, credibility, and funding options over time.

Do business credit cards report to personal credit?

Many business credit cards do not report normal account activity to personal credit bureaus as long as the account stays in good standing. However, policies vary by issuer, and negative activity may still be reported.

Conclusion

A new LLC can get approved for serious business credit.

You do not always need years in business, tax returns, bank statements, or proof of income to get started.

Chase approved my 3-week-old LLC for $21,000 with only articles of organization. U.S. Bank has strong 0% APR business card options. Amex has multiple data points showing $20,000 to $25,000 business card approvals.

But the real key is your profile.

Strong personal credit, low utilization, higher existing limits, low recent inquiries, clean business documents, and bank relationships can make all the difference.

Do not apply randomly.

Build the profile first, choose the right bank, and apply when the odds are in your favor.