7 Average Credit Card Stats You Should Try to Beat

Jul 01, 2026

Most people want excellent credit.

But they never stop to ask a simple question:

“What does average actually look like?”

Because once you know the average, you can start building a profile that beats it.

The average person has a decent credit score, a few credit cards, a credit limit near $30,000, and a balance that is way too expensive if they are paying interest.

That is the difference between being average and being strategic.

Average can get you approved sometimes.

But above average is where the better approvals, better limits, lower rates, and stronger lending options usually start showing up.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

The average American credit profile is not terrible, but it leaves a lot of room for improvement. A stronger credit profile usually means a higher FICO score, lower credit card balances, lower utilization, more available credit, no missed payments, and a longer account history. If you want better credit card approvals, higher limits, and better loan terms, the goal is not just to be average — it is to beat average in the areas lenders care about most.

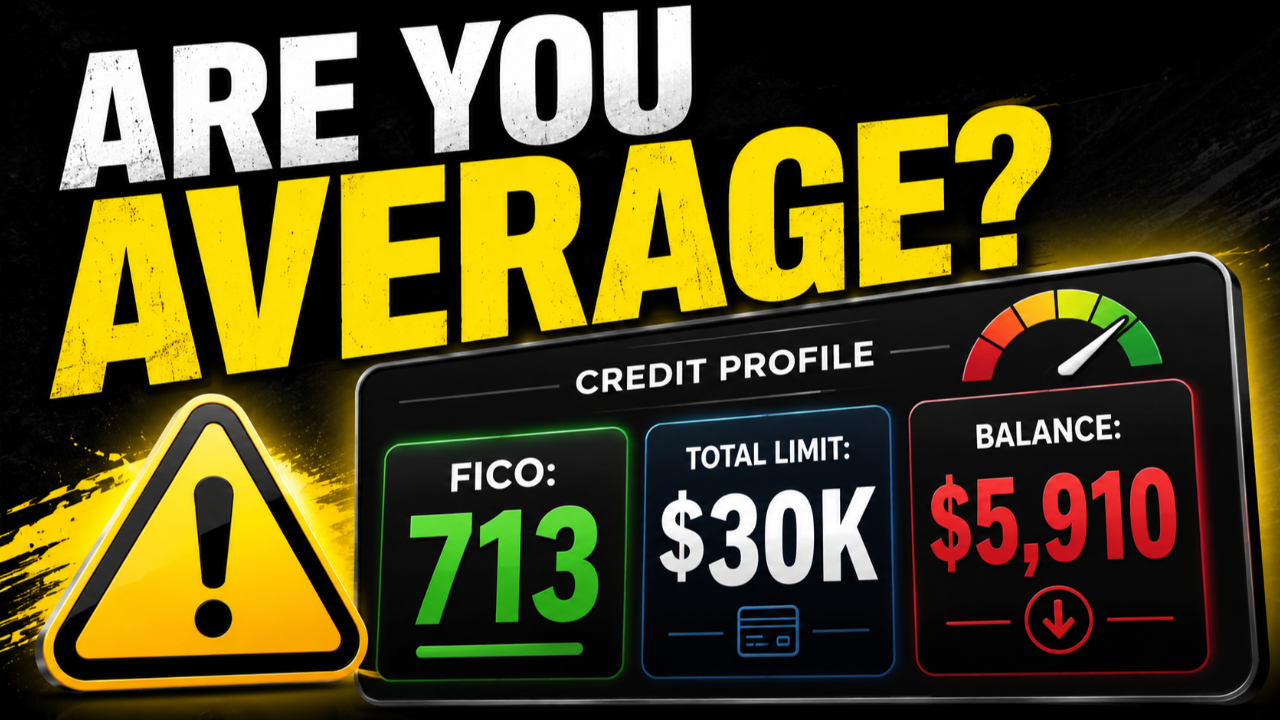

1. Average FICO Score: Around the Low 700s

The average FICO score is around the low 700s.

That is not bad.

In fact, it is good enough for a lot of everyday credit goals.

But if you want the best approvals, best rates, and better odds with lenders, average is not where you want to stop.

Here is how I think about it:

-

680 and up can be workable for many business funding situations

-

700 and up is often a stronger range for many credit cards

-

740 and up can help with better loan and mortgage pricing

-

800 and up is excellent credit

My score is currently around 805, but it still fluctuates.

That is normal.

Even strong credit scores move around depending on balances, utilization, new accounts, inquiries, and reporting dates.

Why a Higher Score Matters

A higher score can save you serious money.

The biggest place this shows up is with loans.

If your score causes you to qualify for a higher mortgage interest rate, that can cost you thousands of dollars over the life of the loan.

That is why credit score improvement is not just about bragging rights.

It is about lowering the cost of borrowing money.

A 716 or 713 score may be average.

But if you are trying to qualify for the best loan terms, I would not aim for average.

I would aim higher.

2. Average Credit Card Balance: Too Expensive If You Carry It

The average credit card balance is thousands of dollars.

And this is where things get dangerous.

A balance of $5,000 or $6,000 may not look insane on paper.

But if you are carrying that balance at a high credit card interest rate, the interest can quietly eat you alive.

For example, if someone carries around $5,910 in credit card debt at a high APR, they could easily be paying close to $100 per month in interest.

That is money going straight to the bank.

Not toward rewards.

Not toward investments.

Not toward savings.

Not toward your business.

Just interest.

Revolvers vs. Transactors

Credit card users usually fall into two groups.

Revolvers carry balances month to month.

Transactors pay in full and avoid interest.

If you want to use credit cards the smart way, you want to be a transactor whenever possible.

That means you use the card for rewards, protections, and convenience, but you do not let the bank win by charging you interest every month.

High achievers usually keep balances much lower, avoid missed payments, and manage their cards like tools instead of emergency loans.

Why Lower Balances Help

Lower balances can help you in several ways:

-

Lower utilization

-

Better credit scores

-

Better debt-to-income ratio

-

Stronger mortgage profile

-

Less interest paid

-

More cash flow

-

Less stress

This matters if you are trying to qualify for a mortgage, personal loan, business loan, or higher credit card limits.

Lenders want to see that you can use credit without depending on it to survive.

3. Average Credit Utilization: Too High for Maximum Scores

Credit utilization is one of the fastest things you can improve.

Utilization is the percentage of your available revolving credit that you are using.

If you have $10,000 in total credit limits and $3,000 in reported balances, your utilization is 30%.

A lot of people hear “keep utilization under 30%” and think they are good.

But 30% is not the target if you want the best scores.

That is more like the warning line.

I like staying much lower.

Personally, I try to keep my reported utilization around 1% to 3%.

FICO high achievers are often reported to keep utilization in the single digits.

That makes sense.

Lower utilization tells lenders you are not maxing out your available credit.

Why Utilization Is So Powerful

Utilization can move your score quickly because it updates when your balances report.

That means you can often improve this part of your profile faster than other areas.

You cannot instantly create a 10-year credit history.

You cannot instantly erase missed payments.

But you can pay down balances before the statement closes and lower what reports to the bureaus.

That is why utilization is one of the easiest short-term score levers.

Helpful resource: If you want to compare cards that may show your starting limit before approval, my 9 Credit Cards That Reveal Your Starting Limit Before Approval resource can help you avoid guessing before you apply.

4. Average Number of Credit Cards: Around 3 to 4 Cards

The average person has around 3 to 4 credit cards.

That can be enough for a basic setup.

But most people put almost no thought into which cards they have.

They open a card at the wrong bank.

They grab a random store card.

They forget what rewards they earn.

They keep everything with one issuer.

They never think about limits, categories, or long-term strategy.

Having multiple cards can be a hidden advantage if you manage them properly.

Why More Than One Card Can Help

Multiple cards can help you:

-

Increase total available credit

-

Lower overall utilization

-

Diversify across banks

-

Separate spending categories

-

Build more account history

-

Protect yourself if one issuer shuts you down

-

Earn better rewards in different categories

This does not mean everyone needs 20 cards.

I have over 20, but that is because I treat credit cards like part of a larger credit strategy.

For most people, the goal is not to collect random cards.

The goal is to build a useful setup.

Do Not Open Cards Just to Open Cards

More cards can help if you pay on time, avoid interest, and keep the accounts open long term.

But if you miss payments, overspend, or forget due dates, more cards can hurt you.

So do not chase quantity first.

Build quality first.

A strong setup might include:

-

A general 2% cash back card

-

A travel rewards card

-

A grocery or dining card

-

A business card if you qualify

-

A high-limit card

-

A credit union card

That is a real system.

Not a random wallet.

5. Average Total Credit Limit: Around $30,000

The average total credit card limit is around $30,000.

At first, that may sound like a lot.

But after you start studying high-limit approvals, you realize it is not that high.

Plenty of people have $30,000 on one card.

Some premium cards and credit union cards can approve limits at or near that level by themselves.

I personally have around $200,000 in total available credit across more than 20 cards.

That did not happen overnight.

It came from building a strong profile, asking for increases, opening the right cards, and spreading relationships across multiple issuers.

Why Higher Credit Limits Matter

Higher limits give you more flexibility.

But the biggest scoring benefit is utilization.

If you have $30,000 in total limits and want to stay around 10% utilization, that only gives you about $3,000 in reported balances to work with.

That can be tight.

If you have $100,000 in total limits, that same 10% utilization gives you $10,000 of room.

That is a completely different game.

Higher limits can help you keep your credit score stable even when your normal spending is higher.

Higher Limits Require Responsibility

A higher limit is not permission to spend more.

It is a tool.

If you use higher limits to run up balances, you are worse off.

But if you use higher limits to keep utilization low, protect your score, and maintain flexibility, they can be powerful.

The goal is not to owe more.

The goal is to have more available credit while owing less.

6. Average Credit Card Transactions: Not Enough to Build Strong Relationships

The average person makes a limited number of credit card transactions per month.

That tells me most people are not really using their cards strategically.

If your card is sitting in a drawer, the bank is not making much money from you.

If you use your card regularly and pay in full, the bank earns interchange fees from your transactions while you avoid interest.

That can help you look like a valuable customer.

Why More Usage Can Help

Responsible card usage can help with:

-

Internal bank relationships

-

Future credit limit increase requests

-

Keeping cards active

-

Avoiding closures for inactivity

-

Earning more rewards

-

Showing consistent repayment behavior

This does not mean you should spend more money.

It means you should route spending you already planned through the right credit cards.

Subscriptions can help.

Groceries can help.

Business expenses can help.

Gas, utilities, dining, travel, software, and vendor payments can all help if the card fits the category and you pay in full.

Use Cards Without Creating Debt

The strategy is simple:

Use the card.

Earn the rewards.

Pay it off.

Repeat.

Do not carry balances just to “build a relationship.”

That is a myth.

You can build a relationship with usage and repayment without paying interest.

Banks like profitable customers, but they also like low-risk customers.

Paying in full shows control.

7. Average Credit Card Interest Rate: Way Too High to Carry Debt

Credit card interest rates are brutal.

Average rates are now in the mid-20% range depending on the source and methodology.

That is expensive money.

At those rates, carrying a balance can get ugly fast.

This is why I say credit cards are great tools but terrible long-term loans.

If you are carrying debt at 24% or 25%, the rewards do not matter.

The interest is eating the rewards alive.

Credit Union Cards Can Be Better for Rates

Credit union cards may offer lower APRs than many major bank cards.

Federal credit unions also have an interest rate ceiling that can keep their card APRs below what you might see from some large commercial banks.

That does not mean every credit union card is perfect.

But if you need a lower-rate backup card, credit unions are worth researching.

The Goal Is to Qualify for the Lowest Rate

Even if you never plan to carry a balance, your APR still matters.

Life happens.

A client pays late.

A car repair hits.

A medical bill shows up.

A business expense comes early.

If you ever need to carry a balance in a pinch, a lower APR can reduce the damage.

The best way to qualify for lower rates is usually the boring stuff:

-

Higher credit score

-

Low utilization

-

Clean payment history

-

Strong income

-

Fewer recent inquiries

-

Longer credit history

-

Better banking relationships

That is why beating average matters.

How to Become Better Than Average

If you want to build a stronger credit profile, focus on the fundamentals.

Start with these:

-

Pay every account on time

-

Keep utilization in the single digits when possible

-

Avoid carrying high-interest balances

-

Ask for credit limit increases strategically

-

Build relationships with multiple issuers

-

Keep older accounts open when they still make sense

-

Use your cards regularly but responsibly

-

Avoid opening too many new cards at once

-

Track your statement closing dates

-

Know which cards report to personal credit

-

Use business cards strategically if you qualify

Average is fine for average outcomes.

But if you want higher limits, better approvals, lower rates, and stronger mortgage terms, you need a stronger profile.

Helpful resource: Before applying for new cards, it may be worth checking whether you are pre-approved first. My Free Credit Card & Loan Pre-Approval Master List can help you find cards and loans that may let you check offers before a hard pull.

Frequently Asked Questions

What is the average FICO score?

The average FICO score is currently in the low 700s. That is a solid range, but if you want better rates and stronger approvals, aiming for 740+ or even 800+ can put you in a better position.

Is a $5,000 credit card balance bad?

A $5,000 balance can become expensive if you carry it month to month at a high APR. It can also hurt your utilization if your total credit limits are not high enough.

What credit utilization should I aim for?

Under 30% is a common guideline, but lower is usually better. If you want stronger scores, single-digit utilization is a better target.

How many credit cards should I have?

There is no perfect number. The average person has around 3 to 4 cards, but the right number depends on whether you can manage them responsibly and whether each card has a purpose.

Is a $30,000 total credit limit good?

A $30,000 total credit limit is around average, but it may still feel low if you spend heavily or want to keep utilization in the single digits. Higher limits can help, but only if you avoid carrying debt.

Should I carry a balance to build credit?

No. You do not need to carry a balance or pay interest to build credit. You can use your card, let a small balance report if needed, and then pay in full.

Conclusion

Average credit is not terrible.

But average is not the goal.

The average consumer may have a decent FICO score, a few cards, a balance that costs real money, utilization that could be lower, and a total credit limit that limits flexibility.

You can do better.

Keep your utilization low.

Pay in full.

Build higher limits.

Use cards strategically.

Avoid missed payments.

Protect your oldest accounts.

And stop letting the bank win with interest.

Credit cards can help you build wealth, travel cheaper, protect purchases, and strengthen your credit profile.

But only if you use them like tools.

Beat average, and the banks start treating you differently.