Amex Personal Loan Approval: Why Daniel Got $45,000 Fast With No Documents

Jun 29, 2026

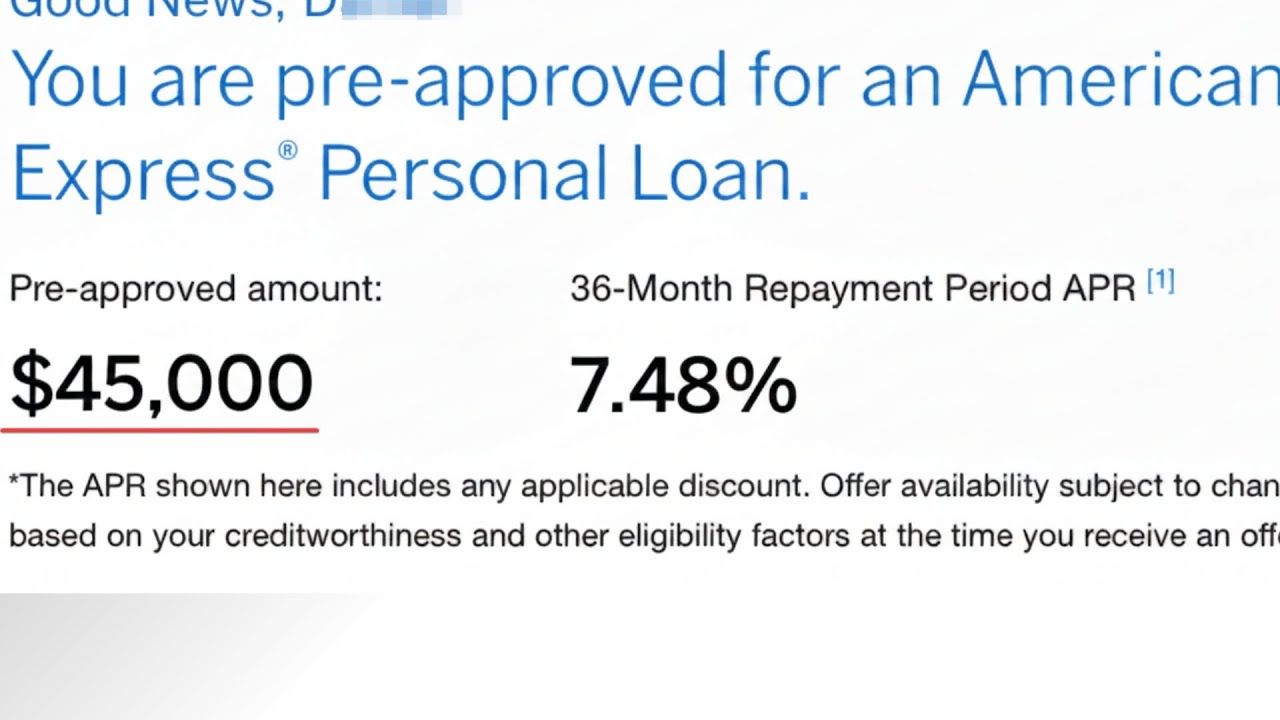

One of our community members Daniel got approved for a $45,000 Amex personal loan.

Funded within two hours.

No documents to chase down.

No long underwriting delay.

No “we’ll get back to you.”

Just a clean approval from a lender that already knew exactly who he was.

And when Daniel checked his Experian report afterward, he did not see a hard inquiry.

That does not mean everyone will get the same result. But his approval gives us a clean lesson in how strong borrowers get treated differently when lenders already trust them.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Daniel was approved for a $45,000 Amex Personal Loan in seconds and said the money was funded within two hours. His approval was likely so fast because he had about 12 years of history with Amex, high-800 credit scores, extremely low utilization, strong income, no negatives, and a long track record of repaying debt responsibly. His result is a personal data point, not a guarantee. Amex says Personal Loans are only available to eligible Card Members who receive an offer, and eligibility does not guarantee approval. (American Express)

Why Amex Approved Him So Fast

By the time Daniel clicked apply, Amex already knew him.

That is the key.

This was not a cold application from someone with no history. This was a borrower Amex had watched for over a decade.

Daniel had been with Amex for around 12 years. He had multiple Amex cards in good standing. His utilization stayed under 1%. His scores lived in the high 800s and sometimes hit 850. He was not carrying credit card debt. He had no negatives. And his income was over six figures.

That kind of profile does not scream risk.

It screams control.

And banks love control.

Amex Personal Loans Are Not Open to Everybody

One important thing about Amex Personal Loans is that you usually cannot just walk in cold and apply like you would with some other lenders.

Amex says its Personal Loans are available to eligible Card Members, and you can only apply if you receive an offer and continue to meet eligibility requirements. You must also be at least 18, be a U.S. citizen or resident of the U.S. or its territories, and have an active American Express Consumer Card.

That matters because Amex is not starting from zero.

If you already have Amex cards, Amex has your internal behavior.

They know how long you have been a customer.

They know how you spend.

They know whether you pay on time.

They know whether your behavior looks stable or messy.

So when someone like Daniel applies, Amex is not just seeing a credit score.

They are seeing years of borrower behavior.

Daniel’s Profile Was Extremely Clean

At the time of the approval, Daniel had the kind of profile lenders fight over.

His file had:

-

No revolving credit card debt for about five years

-

No negative marks

-

Long payment history

-

Multiple Amex cards in good standing

-

Income over six figures

-

Utilization basically near zero

-

Credit scores in the high 800s

That does not mean you need a perfect 850 score to get a personal loan.

But it does show why his approval moved so fast.

Nothing in his profile created friction.

No high utilization.

No late payments.

No recent chaos.

No obvious debt spiral.

No reason for Amex to slow the application down and ask for more proof.

He Uses Debt, But He Does Not Abuse Debt

This is where Daniel’s story gets more interesting.

He is not someone who avoids debt completely.

He uses debt.

But he uses it with a plan.

Years ago, he took a $35,000 consolidation loan to wipe out messy credit card debt, then paid it off. He has also had multiple SoFi personal loans, sometimes between $17,000 and $40,000, and he said those were approved with no documents.

His pattern is simple:

-

Take the loan

-

Use the money strategically

-

Make large payments

-

Pay it off early

-

Avoid falling back into credit card debt

That is a different kind of borrower.

Banks do not hate debt.

Banks hate unmanaged debt.

Daniel’s history tells lenders that he understands repayment. He does not default. He does not treat credit like a panic button. He treats debt like a tool.

That is why a lender can look at him and say, “This person is low risk.”

Banks Compete Hardest for People Who Do Not Need the Money

This is the ugly truth.

Banks compete hardest for borrowers who do not look desperate.

That sounds backward, but it makes perfect sense from the lender’s side.

The person who does not need the money is usually the safest person to lend to.

They have cash flow.

They have credit history.

They have backup options.

They have low utilization.

They are not trying to borrow because everything is falling apart.

Daniel’s $45,000 Amex loan was not about survival. He said he wanted to use other people’s money to pay off other loans.

That is strategy.

Not desperation.

And banks can smell the difference.

The “No Hard Inquiry” Data Point

Daniel said he checked his Experian report and did not see a hard inquiry after the Amex Personal Loan approval.

That is a strong data point.

But I would not publish that as a universal rule without verifying the current application language inside your own Amex offer.

Amex’s public Personal Loan FAQ says you can log in to check eligibility, and before applying, Amex shows the maximum amount you can borrow, maximum APR, and repayment period options. It also says most applicants receive a decision within seconds, though Amex may request more information or deny the application if there is a material change in financial situation or creditworthiness. (American Express)

So the practical takeaway is this:

Daniel did not see a hard inquiry.

But before you apply, read your own Amex offer screen carefully.

If it says there will be a hard pull, believe the screen.

How Fast Can Amex Fund a Personal Loan?

Daniel said his Amex loan funded within two hours.

That was his real-world experience.

Amex’s official language is more conservative. Amex says it can send loan funds to your bank account on file in as fast as one day after you sign the Personal Loan agreement and complete all necessary verification steps, but your bank may take extra time to post the funds.

So Daniel’s two-hour funding was excellent.

But I would treat it as a best-case data point, not the standard promise.

Fast funding can depend on the bank account, timing, verification, business day, and Amex’s internal process.

What Can You Use an Amex Personal Loan For?

Amex Personal Loans are unsecured loans for personal, family, or household expenses.

Amex says they can be used for things like consolidating existing credit card debt, major purchases, home repair or remodeling, or major life events. But they cannot be used for business purposes, post-secondary education, real estate, securities, or to pay down balances on American Express-issued cards.

That last part is important.

You generally cannot use an Amex Personal Loan to pay off Amex cards.

So if your plan is to consolidate Amex credit card balances, read the terms first because that may not be allowed.

Why No Documents Were Needed

Daniel did not have to chase down documents.

No pay stubs.

No tax returns.

No long back-and-forth.

That likely happened because his profile was already strong enough to pass the automated review.

But this is not guaranteed.

Amex says that even if you are eligible to apply, that does not guarantee approval, and Amex may require additional information at any point during the process. (American Express)

So do not assume “no docs” is the rule.

Think of it this way:

The cleaner your profile looks, the fewer questions the lender may need to ask.

The messier your profile looks, the more likely you are to get slowed down.

The Real Lesson From Daniel’s Approval

Daniel’s approval was not luck.

It was the result of years of clean credit behavior.

Here is what you can model from him.

Build Long-Term Banking Relationships

Daniel stayed with Amex for about 12 years.

He used the relationship.

He kept the accounts clean.

And when he wanted a large personal loan, that relationship mattered.

Banks track loyalty and behavior.

Those two things together can create internal trust.

That internal trust can matter more than people think.

Keep Utilization Extremely Low

Daniel was not sitting at 28% utilization thinking, “Well, I’m under 30%, so I’m good.”

He was under 1%.

That is a totally different level of control.

Low utilization tells lenders you are not leaning hard on revolving credit.

It also gives your score room to breathe.

That does not mean everyone needs to live at 0% or under 1% forever. But if you are trying to qualify for a major loan, low utilization helps your file look cleaner.

Use Credit While You Are Stable

This is one of the biggest differences between beginners and pros.

Beginners often use credit when they are desperate.

Pros use credit strategically while they are stable.

Daniel did not need the loan to survive.

He chose the loan because it helped his strategy.

That is a very different signal to a lender.

When you borrow from strength, the lender sees opportunity.

When you borrow from panic, the lender sees risk.

Do Not Consolidate Debt Without a Real Plan

Now let’s be honest.

A story like Daniel’s can make a big personal loan sound like the answer to everything.

And sometimes a personal loan can help.

If you are carrying high-interest credit card debt, a lower-rate personal loan can simplify payments and reduce interest.

But sometimes a new loan just reshuffles the debt instead of fixing the real problem.

That is how people end up with a personal loan and maxed-out credit cards again six months later.

That is the nightmare.

When a Personal Loan Can Make Sense

A personal loan may make sense when:

-

The interest rate is clearly lower than your current debt

-

The payment fits your budget without hurting essentials

-

You stop using the cards you just paid off

-

You want one predictable payment instead of several due dates

-

You have a written payoff plan

-

You are using the loan to reduce total interest, not create breathing room for more spending

That last one is everything.

A loan should move you forward.

Not give you more room to repeat the same mistake.

Helpful resource: If you are comparing personal loan options, SoFi Personal Loans may be worth reviewing because SoFi offers personal loans with same-day funding for many approved borrowers, though same-day funding is not guaranteed and terms depend on underwriting.

When I Would Be Extremely Careful

I would be very cautious with a personal loan if:

-

Your balances keep climbing every month

-

You are using credit cards to survive

-

Your income is unstable

-

You already consolidated before and the debt came back

-

You are only taking the loan to “free up space” on your cards

-

You do not have a written plan to stop the bleeding

This is the part people do not want to hear.

A personal loan can save you money.

Or it can become another layer of debt on top of the debt you already had.

The difference is not the lender.

The difference is the plan.

Why SoFi Kept Showing Up in Daniel’s Story

While Daniel was replying to the email, he received two new pre-approved loan offers in real time.

One from Amex.

One from SoFi.

Both were around 7.5% APR, and SoFi wanted to offer him around $69,000.

That is what happens when lenders like your profile.

They make the first move.

SoFi’s current public personal loan page says rates can be as low as 6.99% with discounts, and its terms show APR examples that vary by term, origination-fee option, financial history, and other factors. SoFi also says most borrowers receive same-day funding when approved and the loan agreement is signed by 5:30 p.m. ET on a business day, but delays can happen and same-day funding is not guaranteed. (SoFi)

That lines up with the bigger lesson:

Strong borrowers get options.

Weak borrowers get conditions.

How to Build Toward a Daniel-Type Approval

Not everybody can copy Daniel’s exact profile.

But you can copy the habits.

Start here.

Pay every account on time.

Keep utilization low.

Avoid unnecessary hard pulls.

Do not carry credit card balances for years if you can avoid it.

Build long-term relationships with lenders.

Use debt with a payoff plan.

Pay off loans early when it makes sense.

Do not apply from desperation.

And before you apply for any personal loan, check whether you are pre-qualified or pre-approved first when the lender offers that option.

A pre-approval does not guarantee final approval, but it can help you avoid applying completely blind.

Helpful resource: Before applying for a new card or loan, my Free Credit Card & Loan Pre-Approval Master List can help you find soft-pull pre-approval options so you are not guessing with your credit.

Frequently Asked Questions

Does Amex offer personal loans?

Yes. American Express offers unsecured personal loans to eligible Card Members who receive an offer to apply and continue to meet eligibility requirements. Amex says you must have an active American Express Consumer Card, be at least 18, and be a U.S. citizen or resident of the U.S. or its territories. (American Express)

How fast can Amex approve a personal loan?

Amex says most applicants receive a decision within seconds, but the decision may be delayed if more information is needed. Daniel’s approval was instant, but your result can vary.

How fast can Amex fund a personal loan?

Amex says funds can be sent to your bank account on file in as fast as one day after you sign the Personal Loan agreement and complete verification. Daniel said his loan funded within two hours, but that should be treated as a personal data point, not a guaranteed funding time.

Can I use an Amex Personal Loan to pay off Amex credit cards?

Amex says Personal Loans may not be used to pay down balances on American Express-issued cards. If your goal is debt consolidation, read the terms carefully before applying.

Does Amex charge origination fees on personal loans?

Amex says its Personal Loans have no application fees, no origination fees, and no prepayment penalties. It can charge a $39 fee for late payments or returned payments.

Should I use a personal loan to consolidate credit card debt?

It can make sense if the rate is lower, the payment fits your budget, and you stop running up the cards you pay off. It can be dangerous if you use the loan to create more available credit and then start swiping again.

Conclusion

Daniel’s Amex Personal Loan approval was not random.

It was the result of years of clean behavior.

He had a long Amex relationship, extremely low utilization, high scores, strong income, no negatives, and a history of using debt without letting it control him.

That is why Amex trusted him.

That is why the approval was fast.

And that is why no document chase was needed in his case.

But here is the bigger lesson:

The best time to borrow is when you do not look desperate.

If you want lenders to compete for you, build the kind of profile that makes them comfortable. Pay on time. Keep balances low. Use credit strategically. Build relationships. And only take personal loans when they move you closer to control, not deeper into debt.

Because a personal loan is just a tool.

Used right, it can create relief and breathing room.

Used wrong, it becomes another payment stacked on top of the problem.