Amex Financial Review: What Triggers It and How to Avoid It

Jun 29, 2026

You have to avoid falling into the Amex financial review trap.

Picture this.

You are on a family trip. You go to pay for dinner with your Amex Gold card, and the card gets declined. Now you are embarrassed. Then you open the Amex app and see something like “Charging Suspended.”

Your heart drops.

You call Amex, and they tell you all your cards are suspended until you submit documents proving your income and financial situation.

That is an Amex financial review.

And based on the 20 data points I reviewed, the biggest trigger was not one missed payment or one random purchase.

It was high-velocity spending.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

An Amex financial review is when American Express pauses or restricts your account while it verifies your financial information, income, spending behavior, or ability to pay. In the 20 data points I reviewed, high-velocity spending triggered 65% of financial review cases. Most people in the sample eventually got their accounts restored, but some had limits reduced, spending limits added, or accounts closed. Amex’s card agreement says it can verify and re-verify income, decline charges, suspend charging privileges, or close accounts under its terms. (American Express)

What Is an Amex Financial Review?

An Amex financial review is a deeper account review where American Express wants to make sure your spending, income, and credit behavior still make sense.

In normal-person language, Amex is basically saying:

“Before we let you keep spending, we need to make sure you can actually pay us back.”

This is not just a casual identity check.

During a true financial review, Amex may freeze your ability to make new charges and ask for documents like tax transcripts, bank statements, or pay stubs. Amex’s agreement says it can obtain credit reports, investigate your ability to pay, and verify or re-verify your employment and income. (American Express)

That is why you do not want to play games with income on an Amex application.

If you tell Amex you make $150,000, you need to be able to prove $150,000.

Not “kind of.”

Not “if you count future income.”

Not “if the business has a good year.”

Prove it.

What an Amex Financial Review Is Not

Not every Amex document request is a full financial review.

If you apply for a credit limit increase and Amex gives you the option to withdraw the request, that is usually not the same thing as a full financial review.

That is more like Amex saying:

“We need more information to approve this specific request. You can continue or back out.”

A true financial review is different.

With a real financial review, you usually do not get to simply withdraw and move on like nothing happened. Your account may be temporarily locked, new charges may be blocked, and you may have to deal directly with the financial review team.

That is the difference.

A credit limit increase document request is about one request.

A financial review is about the whole relationship.

What Happens During an Amex Financial Review?

When Amex hits you with a financial review, your account can change fast.

The most common things people reported were account suspension, a call or email from Amex, document requests, restricted access, and a waiting period while Amex reviewed everything.

Amex’s own card agreement says it may decline charges based on creditworthiness, spending, payment behavior, credit history, credit score, and personal resources known to Amex. It also says Amex may suspend your ability to make charges or cancel the account. (American Express)

So when Amex says “charging suspended,” it is not bluffing.

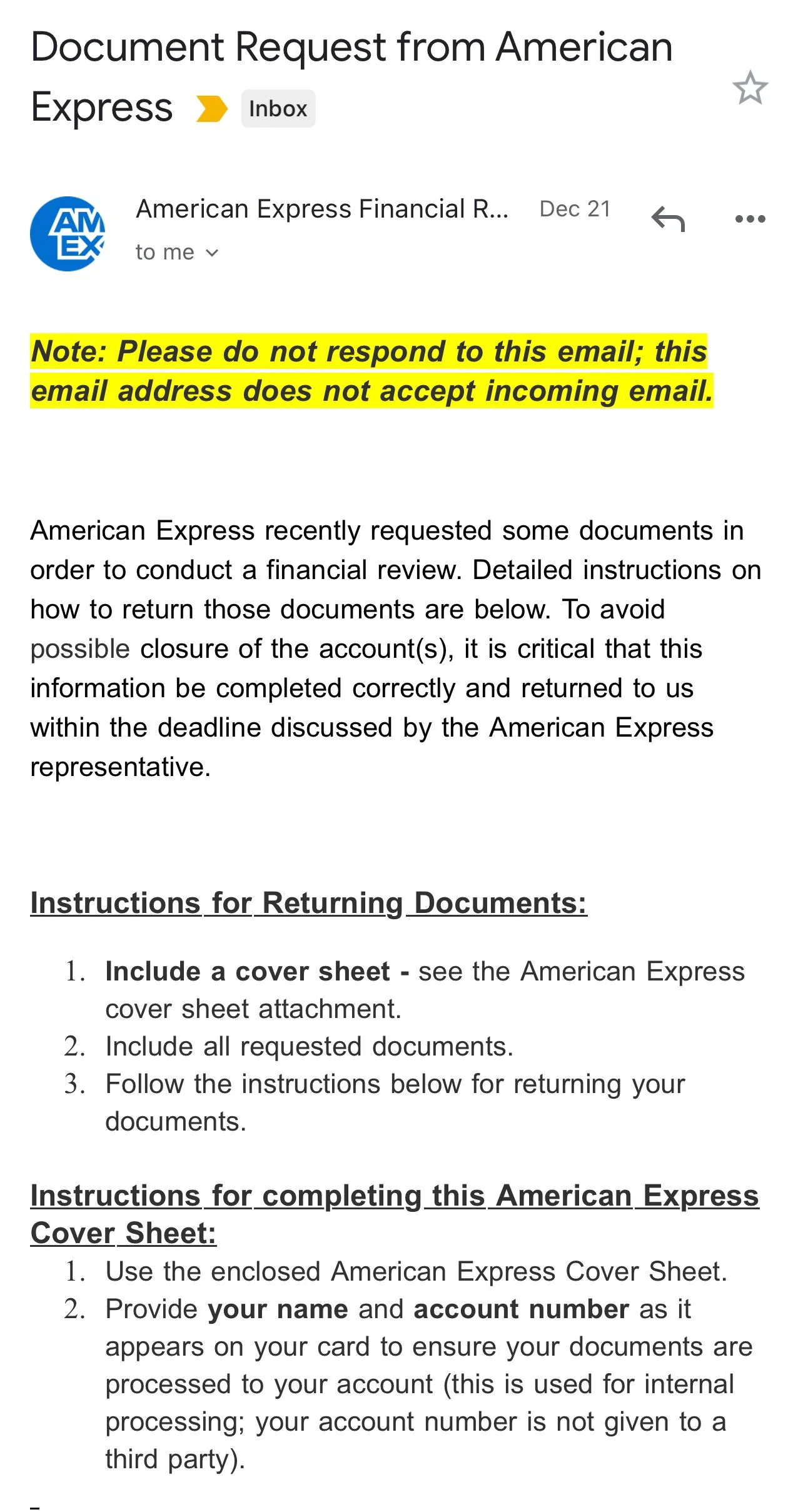

Documents Amex May Request

The documents can vary, but in the 20 data points I reviewed:

-

25% of people were asked for two years of tax returns or tax transcript access

-

66% were asked for either two months of bank statements or two pay stubs

One important note: the script mentioned Form 4506-T, but current IRS and Amex materials commonly reference Form 4506-C for lender tax transcript requests. The IRS says taxpayers can authorize a lender to request tax transcripts through Form 4506-C, and Amex has its own 4506-C instructions for retrieving personal tax transcripts. (IRS)

If Amex asks for documents, do not send messy screenshots and hope for the best.

Send exactly what they ask for.

And send it fast.

What Happens to Your Amex Points During Financial Review?

During a financial review, your ability to use points may be restricted.

That does not automatically mean you lose your Membership Rewards points. But if Amex finds abuse, misuse, gaming, returned payments, or account issues, your points can become a problem.

Amex Membership Rewards terms say Amex may take away points, temporarily suspend your ability to redeem or earn points, cancel your program account, or cancel your cards if it determines there was abuse, misuse, or gaming. The terms also say points can be forfeited if Amex cancels a linked card account for certain reasons.

So if you are under review, this is not the time to panic-transfer points, create weird redemptions, or make yourself look more suspicious.

Be boring.

Boring is good here.

The 3 Main Outcomes of an Amex Financial Review

There are three major ways this can end.

1. Account Reinstatement

This was the most common outcome in the data I reviewed.

About 91% of people who reported an outcome got their accounts restored.

That sounds great, but I think that number may be a little high because some people never came back to report the final result. And let’s be real: people are more likely to disappear when the story ends badly.

Still, reinstatement is very possible.

If your income checks out, your documents match, and Amex does not see anything serious, you may be able to resume using your cards.

2. Credit Limit Reduction or Spending Limit Added

This is the “you survived, but Amex no longer trusts you the same way” outcome.

Some people kept their cards but had limits reduced.

Others had a hard spending limit added to a charge card.

That can sting, especially if you were used to flexible spending power.

But from Amex’s point of view, this is risk control. They are not always trying to kick you out. Sometimes they are just cutting exposure.

3. Account Closure

This is the worst outcome.

Amex may close your accounts if your stated income does not match your real income, you do not submit the requested documents, or Amex believes there was fraud, abuse, money laundering, or serious account risk.

Amex’s agreement says giving false information can be considered default, and if Amex considers an account in default, it may suspend charging, cancel features, or require immediate payment. It also says Amex may cancel or suspend an account at any time and for any reason, subject to the agreement and applicable law. (American Express)

That is why this is serious.

A financial review is not just customer service asking for an update.

It can decide whether you keep your Amex relationship.

The #1 Amex Financial Review Trigger: High-Velocity Spending

This was the biggest pattern by far.

In the 20 data points I reviewed, 65% of financial reviews were triggered by high spending or irregular high-velocity spending.

High-velocity spending means you suddenly spend a lot of money in a short period of time.

This is especially risky when:

-

The card is brand new

-

The card was dormant for a long time

-

You suddenly make a massive purchase

-

You hit a sign-up bonus extremely fast

-

Your spending does not match your stated income

-

Your spending does not match your past Amex behavior

One person opened a business Platinum card and immediately put a large hotel charge on it. Then Amex suspended multiple cards and placed the account under financial review.

Another person got approved, spent around $5,000 in the first week, and then received a call from the Amex financial review department.

That is the pattern.

Amex does not like sudden spikes that make no sense based on your history.

They want to see a normal spending ramp.

Not zero to $18,000 overnight.

Cash-Like Transactions Can Trigger Problems

The second major trigger was cash-like behavior.

In my data set, 15% of financial review cases were caused by cash-like transactions.

This includes behavior that looks like you are turning credit into cash or cash equivalents.

Amex’s card agreement defines cash advances as charges to get cash or cash equivalents, including items like travelers cheques, gift cheques, foreign currency, money orders, digital currency, casino gaming chips, racetrack wagers, and other offline or online betting transactions. It also separately defines person-to-person transactions as charges for funds sent to another person or added to an Amex Send account. (American Express)

The data points I reviewed included examples like precious metals purchases and large PayPal-style transfers.

Those can look risky.

They can look like manufactured spending.

They can look like cash access.

And Amex is very sensitive to that.

If you need to send money through Venmo or PayPal, Amex does have its own Send & Split feature for eligible U.S. consumer cards. Amex says Send & Split lets eligible card members send money to Venmo or PayPal users through the Amex app, but it is not available for prepaid cards, corporate cards, small business cards, or Amex-branded cards issued by other financial institutions.

So do not freestyle cash-like transactions and assume Amex will be cool with it.

That is how people get flagged.

Returned Payments Are a Serious Amex Red Flag

Returned payments were another major issue.

In the 20 data points I reviewed, 20% of financial reviews were triggered by returned payments.

A returned payment happens when your payment bounces. Maybe there were not enough funds. Maybe the bank account was frozen. Maybe the routing or account number was wrong.

Either way, credit card companies hate it.

And Amex is no exception.

The Amex Gold agreement says a returned payment can trigger a penalty APR, and returned payments can come with fees.

But the bigger issue is not the fee.

The bigger issue is trust.

A returned payment tells Amex, “This person may not be able to pay.”

Even if it was an honest mistake, Amex may treat it like a major risk signal.

So before making a payment, make sure the money is actually there.

Do not guess.

Be Careful With the Check Spending Power Button

The Amex “Check Spending Power” tool can be useful.

It lets you test whether a large purchase is likely to be approved. Amex says using the tool does not create a credit inquiry and does not affect your credit score. But Amex also says it limits the number of daily requests to help prevent fraud.

That should tell you something.

The tool is not a toy.

If you check one realistic large purchase before making it, that is one thing.

If you sit there punching in bigger and bigger numbers just to see how high Amex will go, that can look weird.

Use it sparingly.

And only use it when you are actually planning a real purchase.

Do Not Lie About Income

This one should be obvious, but apparently it is not.

Never put income on an Amex application that you cannot prove.

If your tax return says one number, your bank statements say another number, and your application says something totally different, you may have a problem.

This is especially important for self-employed people and business owners.

You might feel like your business is doing well, but if your tax return shows low taxable income because of write-offs, Amex may not view your income the way you view your income.

One data point involved someone who stated income based on what they expected to earn, but their prior-year tax documents showed very little taxable income because of business losses. When Amex asked for tax transcript authorization, that person got nervous.

That is exactly the trap.

Do not state an income unless you can defend it with documents.

Avoid Aggressive Churning Behavior

Amex knows what churning looks like.

Opening cards just for bonuses, spending fast, closing quickly, repeating the cycle, and stacking suspicious transactions can all raise risk.

Is earning bonuses illegal?

No.

But if your behavior looks like you are only there to extract value and leave, Amex may watch you more closely.

That does not mean you can never open multiple Amex cards.

It means you need to move like a normal customer.

Use the cards.

Pay on time.

Keep spending reasonable.

Do not turn every new card into a sprint.

Helpful resource: Before applying for another card, it may be worth checking soft-pull pre-approval tools first so you are not burning hard pulls or adding unnecessary risk to your profile.

Keep Your Financial Information Updated

If your income changes, update it accurately.

If your spending grows because your income grew, Amex needs your profile to make sense.

The problem is when your spending rises, but your stated income, payment history, and known resources do not support the activity.

That is when the account starts looking risky.

You do not need to over-explain your life to Amex every week.

But your profile should not look outdated if you are putting serious spend through the cards.

What To Do If Amex Puts You Under Financial Review

If Amex places you under financial review, do not make it worse.

Here is what I would do:

-

Stop trying to use the cards

-

Call the financial review team directly

-

Ask exactly what documents they need

-

Ask for the deadline

-

Submit clean, complete documents

-

Keep copies of everything

-

Make all payments on time

-

Do not send fake, edited, or incomplete documents

-

Do not argue with front-line reps who cannot help

You want to look calm, organized, and low-risk.

Not defensive.

Not messy.

Not desperate.

Remember, Amex is trying to decide if they can trust you.

Act like someone who should be trusted.

The Good News About Amex Financial Reviews

Here is the good news.

An Amex financial review is not always the end.

In my data set, most people who completed the process and had documentation that matched their profile got their accounts restored.

That is better than some banks that may simply shut you down and move on.

Amex may suspend first and give you a chance to prove yourself.

That does not make financial review fun.

It just means you should not panic if it happens.

Submit what they ask for, be honest, and do not create more red flags during the review.

Frequently Asked Questions

What triggers an Amex financial review?

Based on the 20 data points I reviewed, the biggest trigger was high-velocity spending. Other triggers included cash-like transactions, returned payments, unverifiable income, aggressive account behavior, and unusual use of the Check Spending Power tool.

How long does an Amex financial review take?

Most data points suggested the process can take one to three weeks, depending on what documents Amex asks for and how fast everything gets reviewed. Tax transcript requests may take longer than simple bank statement or pay stub reviews.

What documents does Amex ask for during financial review?

Amex may ask for tax transcript authorization, bank statements, pay stubs, or other documents that verify income and ability to pay. IRS guidance says lenders can request tax transcripts through Form 4506-C, and Amex has its own 4506-C instructions. (IRS)

Can Amex close my account after financial review?

Yes. Amex can close accounts if it finds serious issues, if you do not provide the requested documents, or if your information does not check out. Amex’s agreement says it may cancel or suspend accounts and may treat false information or inability to pay as default.

Can I lose my Amex points during a financial review?

You may lose points if Amex cancels your account for certain reasons or determines there was abuse, misuse, or gaming. Amex Membership Rewards terms say Amex may take away points, suspend earning or redemption, cancel the program account, or cancel cards in those situations.

Does using Check Spending Power trigger financial review?

Using it once for a real purchase is not automatically a problem. Amex says the tool does not affect your credit score, but it also limits daily requests to prevent fraud. The risk comes from abusing the tool, checking unrealistic amounts, or repeatedly testing limits in a way that makes your profile look suspicious.

Conclusion

Amex financial review is not random.

It usually happens when your account starts looking riskier than Amex expected.

The biggest mistake I found was high-velocity spending, especially on new or recently inactive cards. Cash-like transactions, returned payments, unverifiable income, aggressive churning, and weird spending-power checks can also put you on the radar.

The best way to avoid the trap is simple:

Move like a real customer.

Use the card normally. Ramp spending slowly. Pay on time. Avoid cash-like transactions. Do not lie about income. Do not abuse tools. And if Amex asks for documents, send clean proof fast.

Because once Amex suspends your charging privileges, you are no longer trying to earn points.

You are trying to save the relationship.