Amex Credit Limit Increase Strategy: How People Grow Limits Fast

Jun 27, 2026

American Express may be one of the best credit card issuers for growing high credit limits.

Not because every approval is massive.

Not because everyone gets approved for $30,000 on day one.

And not because Amex guarantees everyone a huge increase.

But because Amex has a pattern that makes it very different from many other major credit card companies.

People are seeing fast credit limit increases.

People are seeing large jumps.

And in some cases, people are growing one Amex card from a small starter limit into a $20,000, $30,000, $40,000, or even $50,000 credit line.

That is why Amex deserves serious attention if your goal is to build high-limit personal or business credit.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

Based on real user data points, American Express is one of the strongest major issuers for credit limit growth. Many people report being eligible for their first credit limit increase around three months after opening a card, and some report getting multiple increases about 90 days apart. The popular “3X CLI” strategy is based on reported experiences, not a guaranteed official rule. Larger limits, especially above $25,000 to $35,000, may trigger additional income verification or financial review.

Why Amex Gets So Much Attention for High Limits

A lot of credit card issuers are conservative with credit limits.

You might get approved, but the starting limit can be disappointing.

Some banks will give you $500, $1,000, or $2,000 and make you fight for every increase afterward.

Amex can be different.

Across the data points I reviewed, Amex showed up again and again as one of the strongest issuers for:

-

Higher starting limits

-

Fast first credit limit increases

-

Repeat credit limit increases

-

Large one-time jumps

-

Limits above $20,000

-

Limits above $30,000

-

Business credit card expansion

-

Business line of credit opportunities

That does not mean Amex is easy.

You still need a profile they like.

But if you are trying to build serious available credit, Amex is one of the first issuers I would study.

Starting Limits: Amex Can Start Small or Big

Not every Amex approval starts huge.

In the data points I reviewed, some people started with limits around $1,000.

That may not sound exciting.

But the important part is what happened later.

One person started with a $1,000 Blue Cash Everyday card and eventually grew the limit to $25,000 after about 15 months.

That is a massive change.

And it shows why the starting limit is not always the full story with Amex.

A small starting limit can still become a serious credit line if the account is managed well and Amex continues approving increases.

Blue Cash Everyday Shows Up Often

Across the Amex data points, the Blue Cash Everyday card showed up often.

That makes sense.

It is one of Amex’s more approachable no-annual-fee consumer cards.

For someone trying to start a relationship with Amex, Blue Cash Everyday may be one of the cards worth researching first.

That said, do not assume it is automatically the easiest Amex card for every person.

Approval odds depend on your credit profile, income, debt, existing Amex relationship, and other underwriting factors.

But from the data points, Blue Cash Everyday appears often in Amex credit limit growth stories.

Big Starting Limits Are Possible Too

Amex is not only about small starter limits that grow later.

Some people are approved with large limits right away.

One data point showed an Amex Blue Cash Preferred approval with a starting limit of $31,300.

That is not normal for most issuers.

A lot of banks will not start new consumer cards anywhere near that high unless the profile is very strong.

The interesting part is that this person waited around 91 days, requested a credit limit increase, and was approved for a new $35,000 limit.

That shows two things:

First, Amex can approve high starting limits.

Second, even high starting limits may still have room to grow.

Why the First 90 Days Matter

A lot of Amex credit limit increase data points seem to cluster around the first three months.

Many people report requesting their first increase after the third statement or around the 90- to 100-day mark.

One data point showed someone opening an Amex Blue Cash Everyday card with a $2,000 starting limit, getting increased to $6,000 after about 102 days, and then getting increased again around 96 days later.

Another data point showed someone with a $10,000 starting limit asking for a larger increase after about 93 days and getting approved for $30,000.

That is why people talk so much about Amex and 90-day credit limit increases.

But remember:

This is based on reported data points, not a guaranteed official rule.

The Amex 3X CLI Strategy

One of the most famous Amex credit limit strategies is the “3X CLI.”

CLI stands for credit limit increase.

The idea is simple:

If your Amex card starts with a $1,000 limit, you may request $3,000.

If your card starts with $3,000, you may request $9,000.

If your card starts with $10,000, you may request $30,000.

That is the basic 3X strategy.

Many people have reported success with this.

But again, this is not a promise.

Amex can approve the full amount, counter with a lower amount, ask for more information, or deny the request.

The strategy is popular because it has worked for many people, but your profile still matters.

Why Amex CLIs Can Be So Powerful

Credit limit increases can help your profile in a few ways.

First, they give you more spending power.

Second, they can lower your utilization ratio if your balances stay the same.

Third, they can help you build toward higher-limit approvals with other issuers.

For example, if your highest personal credit card limit is $3,000, some banks may hesitate to suddenly approve you for $25,000.

But if Amex helps you build a $20,000 or $30,000 limit, your profile starts looking different.

Higher limits can create a snowball effect.

One high-limit card can make the next high-limit approval more realistic.

Helpful resource: If you want to find cards that may let you check offers before risking a hard pull, my Free Credit Card & Loan Pre-Approval Master List can help you compare preapproval options: https://courses.calbartoncashback.com/pre-approval-master-list-Blog

Amex Can Allow Repeat Increases

One of the strongest Amex patterns is repeat credit limit growth.

Some issuers make you wait six months or longer between increases.

Some barely approve increases at all.

Some require hard pulls.

Some fintech cards do not let you request increases in any meaningful way.

Amex appears much more flexible in many data points.

One example showed a card going:

-

$3,100 to $9,300

-

$9,300 to $27,900

-

$27,900 to $44,500

That is serious growth.

Again, not guaranteed.

But it shows why Amex gets so much attention from people trying to build high limits.

The $20,000+ Credit Limit Zone

Once you start getting into $20,000 and $30,000 limits, your credit profile matters more.

From the data points I reviewed, people with Amex limits over $20,000 tended to have good credit.

The average score I found was around 750.

The lowest score in that group was around 701.

That does not mean a 701 score guarantees a $20,000 limit.

It just means high-limit Amex approvals and increases usually require a stronger file.

If your score is in the low 600s, your first goal may be getting approved and building history.

If your score is in the 700s with low utilization and clean payment history, higher limits become more realistic.

What Happens Above $25,000 to $35,000?

This is where you need to be careful.

As Amex limits get larger, the chance of additional review can increase.

Many people believe Amex starts asking more questions when credit limits move above the $25,000 to $35,000 range.

That can include income verification or what people often call a financial review.

One data point involved someone asking for more than $35,000, going through review, connecting personal bank accounts for verification, and later getting approved for a $50,000 limit.

That is a huge limit.

But the process was not instant and casual.

Amex wanted more confidence before extending that much credit.

So if you are requesting a very large increase, be ready to support the income number you provide.

Do Not Lie About Income

This should be obvious, but it needs to be said.

Do not lie about your income to get a higher Amex limit.

If Amex asks for verification and your stated income does not match reality, you could create a major problem.

That could lead to a denial, credit limit decrease, financial review, or account issues.

A higher limit is not worth risking your entire relationship with Amex.

Be accurate.

Be realistic.

And only request limits that make sense for your profile.

Amex Credit Limit Increase Requests May Not Always Be Soft Pulls

A lot of people report Amex credit limit increases without hard pulls.

That is one reason Amex is so popular.

But you should not assume every request in every situation will always be a soft pull.

American Express says credit limit increase requests can involve credit review, and issuer-requested increases may sometimes involve a hard inquiry.

So the safe way to frame it is this:

Many Amex customers report soft-pull credit limit increases.

But you should still review current Amex language and understand that hard-pull risk can vary.

If you are trying to protect your credit score before a mortgage or major loan, be extra cautious.

Why Your First Amex Card Matters

Starting a relationship with Amex can be a major turning point.

Many people report that their first Amex card caused a hard pull, often from Experian.

Then later Amex cards were approved with soft pulls.

I have seen data points where people got a first Amex card with a hard pull, then received additional personal or business Amex cards later without another hard inquiry.

That is one reason Amex is so attractive.

Once you are in the ecosystem, the next approval may be easier to check or pursue.

But again, this is not guaranteed.

Amex can still review your profile.

They can still deny you.

They can still ask for more information.

And they can still change processes over time.

Amex Business Cards Can Expand the Relationship

Another reason I like Amex is the business side.

If you have a business or even a legitimate side business, Amex business cards can be powerful.

In many cases, business credit cards may rely heavily on your personal credit profile during approval.

You may not need a long business history for some business credit cards.

You may not need business tax returns.

You may not need established business credit.

That is why Amex business cards can be a good next step for people who already have strong personal credit and legitimate business activity.

But do not apply for business cards if you do not have a real business purpose.

Keep it legitimate.

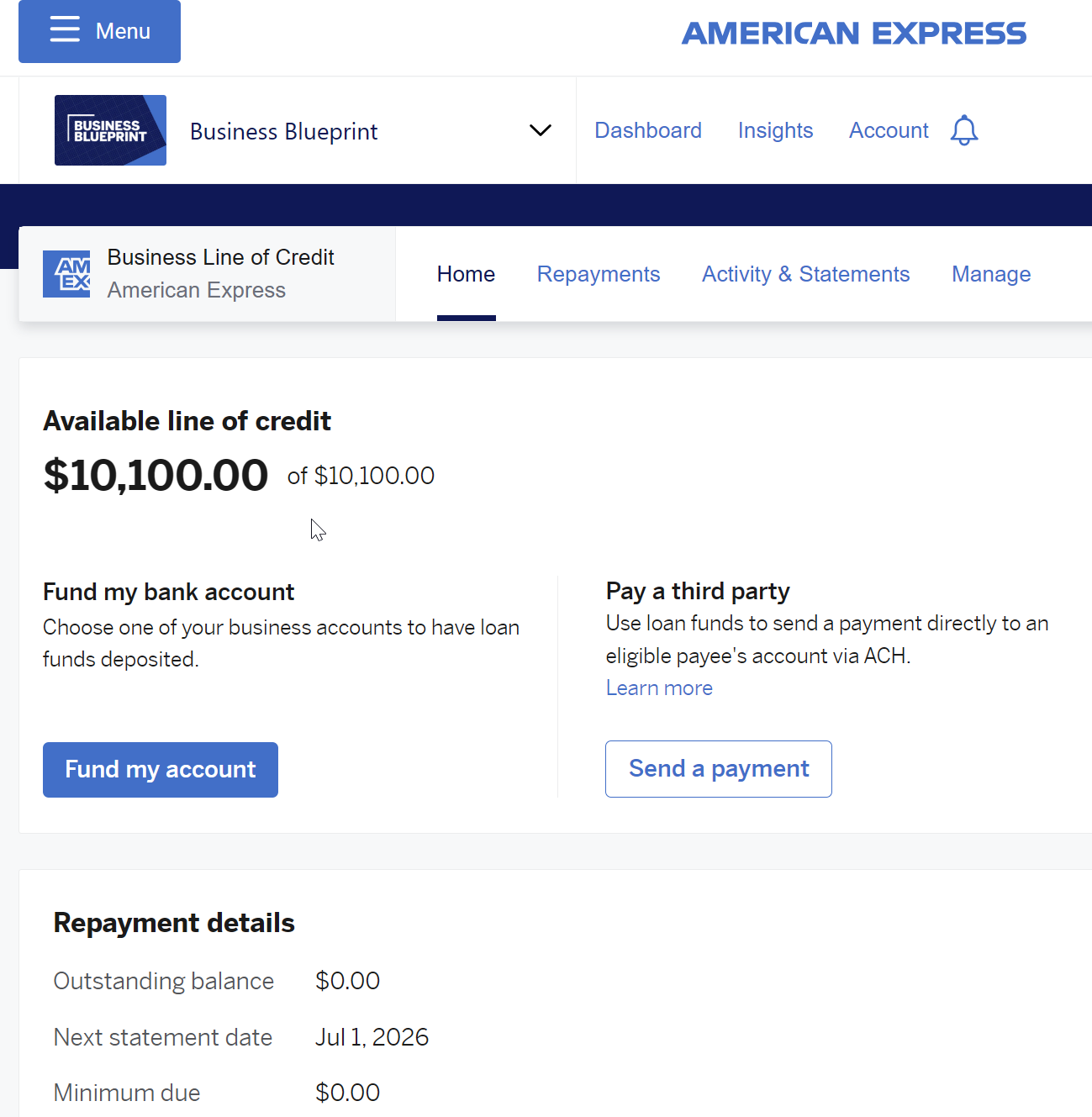

Amex Business Line of Credit

Amex also offers the American Express Business Line of Credit through Business Blueprint.

This is different from a credit card.

A business line of credit gives you access to funds that can be drawn when needed, subject to approval and terms.

That can be useful for:

-

Payroll

-

Inventory

-

Rent

-

Marketing

-

Contractors

-

Short-term working capital

-

Cash flow gaps

In my case, after Barton Media LLC turned one year old, I was approved for a $10,100 Amex business line of credit.

That got my attention because business lines of credit are often harder to get than business credit cards.

Many lenders want two years in business, strong revenue, tax returns, profit and loss statements, or a deeper banking relationship.

Amex’s minimum requirements can be more accessible for some businesses.

Amex Business Line of Credit Requirements

American Express currently lists minimum requirements that include:

-

Applicant at least 18 years old

-

Business started at least one year ago

-

FICO score of at least 660 at the time of application

-

Recent average monthly revenue of at least $3,000

Those requirements do not guarantee approval.

Amex still reviews the overall business and personal profile.

But compared to many business funding products, those minimums are worth knowing.

For newer businesses with real revenue, Amex Business Line of Credit can be an underrated option to research.

Why This Matters for Business Owners

Business owners often need flexible capital.

A credit card can help with purchases.

But a line of credit can give more direct access to working capital.

That can matter when you need cash for expenses that do not fit cleanly on a card.

But debt is still debt.

Do not take a line of credit just because it is available.

Use it only when the business has a clear plan to repay it.

A line of credit can help cash flow.

It can also hurt cash flow if you borrow without a plan.

The Best Amex Strategy

If I were building an Amex strategy from scratch, I would think about it in stages.

First, get into the Amex ecosystem with a card that fits your profile.

Second, use the card responsibly.

Third, pay on time and keep utilization under control.

Fourth, request a credit limit increase after enough account history has built.

Fifth, consider repeat increases only when your income and profile support it.

Sixth, look at business cards only if you have a legitimate business.

Seventh, research the Amex Business Line of Credit if your business has been operating for at least a year and meets the minimum requirements.

That is the clean approach.

Not rushing.

Not lying.

Not forcing limits your profile cannot support.

Just building the relationship.

What to Avoid With Amex

If you want to keep Amex happy, avoid risky behavior.

That means:

-

Do not miss payments

-

Do not carry high utilization

-

Do not inflate income

-

Do not request huge limits you cannot support

-

Do not trigger unnecessary financial reviews

-

Do not open cards with no plan

-

Do not chase business products without a real business

-

Do not treat soft-pull data points as guaranteed rules

Amex can be generous.

But generous does not mean careless.

They will still manage risk.

Frequently Asked Questions

Can you increase your Amex credit limit twice in 90 days?

Some people report getting Amex credit limit increases about 90 days apart, but this is not guaranteed. Many data points suggest Amex can be faster than other issuers, but eligibility depends on your account history, credit profile, income, and Amex’s review.

What is the Amex 3X credit limit increase strategy?

The 3X strategy is when you request up to three times your current credit limit. For example, someone with a $3,000 limit may request $9,000. Many people have reported success with this, but Amex can approve, counter, deny, or request more information.

Does Amex do a hard pull for credit limit increases?

Many people report soft-pull Amex credit limit increases, but Amex says credit limit increase requests can involve credit review and may sometimes involve a hard inquiry. Check current terms before requesting if a hard pull would be a problem.

What credit score do you need for a high Amex limit?

Based on the data points reviewed, people with Amex limits over $20,000 often had good credit, with many around the mid-700s. That does not guarantee approval, but stronger scores, low utilization, and clean payment history can help.

Can Amex ask for income verification?

Yes. If you request a high enough limit or trigger additional review, Amex may ask for income verification or financial documentation. Be honest about income and be prepared to support what you report.

Is the Amex Business Line of Credit easy to get?

It may be more accessible than some business lending products, but it is not guaranteed. Amex currently lists minimum requirements such as 12 months in business, 660+ FICO, and $3,000+ average monthly revenue, but approval depends on the overall profile.

Final Thoughts

Amex is one of the strongest credit card issuers to study if your goal is high credit limits.

The data points are hard to ignore.

Small starter limits growing into $20,000+ cards.

Large starting limits over $30,000.

Repeat credit limit increases around 90-day windows.

Reported 3X CLI approvals.

And some customers reaching $40,000 or $50,000 limits.

But the right takeaway is not that Amex guarantees huge limits.

The takeaway is that Amex can reward clean profiles, responsible usage, and strong income with meaningful credit growth.

Start with a card that fits.

Use it well.

Keep your profile clean.

Request increases strategically.

Be honest about income.

And build the relationship over time.

That is how Amex can become one of the most powerful issuers in your credit card setup.