How to Get an Amex Business Line of Credit With No Hard Pull

Jun 29, 2026

The American Express Business Line of Credit is one of the more interesting business funding options for newer LLCs.

Why?

Because some business owners can check for an offer and get approved without a hard credit pull.

That is a big deal.

A hard pull can drop your personal credit score, add an inquiry to your report, and create problems if you are trying to stack credit cards, apply for loans, or keep your profile clean for future approvals.

But with Amex, if you already have the right relationship and you follow the right pre-approval path, you may be able to access business funding without taking that hit.

I personally got approved for a $10,100 Amex Business Line of Credit just over a year into business while doing around $5,000 to $10,000 in monthly revenue.

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Quick Answer

You may be able to get an American Express Business Line of Credit with no hard pull if you are already an Amex customer and you check through the pre-approval path instead of applying manually. Amex may require your business to be at least one year old, have a personal FICO score of at least 660, and generate at least $3,000 per month in revenue. Your result may vary based on your Amex relationship, business revenue, credit profile, and whether you receive a pre-approved offer.

What Is the American Express Business Line of Credit?

The American Express Business Line of Credit is a business funding product designed to give business owners access to working capital.

This can be useful if you need money for inventory, payroll, marketing, equipment, cash flow gaps, or general business expenses.

The big reason people pay attention to this product is simple: newer businesses may have a real shot.

Most traditional lenders want to see multiple years in business, strong revenue, tax returns, bank statements, and a full underwriting review. Amex can be more accessible if your business is already in their ecosystem and your cash flow supports the offer.

This does not mean everyone gets approved.

But compared to many business funding products, the Amex Business Line of Credit can be one of the better options for business owners who are already building a relationship with American Express.

Key Features of the Amex Business Line of Credit

Here are the main features from the original data:

-

Credit limits may range from $2,000 to $250,000.

-

Larger credit lines may be reserved for select existing Amex customers with stronger relationships and financial history.

-

Repayment terms may include 6, 12, 18, or 24 months.

-

Short-term repayment options of 1, 2, or 3 months may be available to select Amex customers.

-

Amex does not charge origination fees, annual fees, or prepayment penalties on this product.

That sounds strong on the surface.

But you need to understand how the product actually works before calling it a true business line of credit.

Is the Amex Business Line of Credit a True Line of Credit?

This is where things get tricky.

When most business owners hear “business line of credit,” they think of revolving credit.

That usually means you get approved for a limit, borrow what you need, pay it back, and then reuse the available credit again later.

That is how a traditional business line of credit works.

But the Amex Business Line of Credit does not work exactly like that.

Each draw is treated more like a separate loan with its own repayment schedule. That is why some people say it feels more like an installment loan than a true revolving business line of credit.

And honestly, they are not wrong.

How the Amex Business Line of Credit Works

With Amex, each time you take a draw, that draw becomes its own individual loan.

So instead of borrowing, repaying, and freely reusing the same revolving line, you are taking separate draws with structured repayment terms.

That means:

-

Each draw has its own repayment plan.

-

You choose a fixed repayment term.

-

You do not get the same flexibility as a traditional revolving line of credit.

-

You cannot just pay interest and roll the balance forever.

-

You may need to request another draw when you need more funds.

That is not automatically bad.

It just means you need to know what you are getting.

If you want predictable payments, this structure can actually be helpful. But if you want a flexible revolving line where you can borrow, repay, and borrow again freely, this may not feel like the line of credit you had in mind.

Amex Charges Loan Fees Instead of Traditional Interest

Another important difference is how Amex charges for the money.

Instead of a normal APR-based revolving balance, Amex charges a loan fee.

According to the original content, the fee is higher in the first half of the loan term and gradually decreases in later months.

That matters because you may not be able to avoid the fee just by repaying early.

With some loans or lines of credit, paying early can reduce how much interest you pay. With a fee-based structure, the math can work differently.

So before taking any draw, you need to understand the total cost.

Do not just look at the approved limit.

Look at the repayment amount, the term, and the fees attached to that specific draw.

Who Is the Amex Business Line of Credit Good For?

The Amex Business Line of Credit can make sense if you need quick access to business funding and you are comfortable with fixed payments.

It may be a good fit if:

-

You need working capital for business expenses.

-

You already have steady business revenue.

-

You want predictable monthly payments.

-

You already have an American Express relationship.

-

You qualify through a pre-approved offer.

-

You want to avoid a hard pull if possible.

But it may not be the best fit if your business cash flow is unstable.

Fixed payments sound great until business slows down. If your revenue is inconsistent, you need to be careful with any product that locks you into a repayment schedule.

Helpful Resource: Before applying for business funding, it helps to know whether your business looks fundable from a lender’s perspective. My Business Credit Buildout System is designed to help business owners build a stronger profile and prepare for funding.

Amex Business Line of Credit Requirements

Not everyone can get the American Express Business Line of Credit.

Based on the original content, here are the key eligibility requirements:

-

You must be at least 18 years old.

-

Your business must be at least one year old.

-

Your personal FICO score should be at least 660.

-

Your business should generate at least $3,000 in monthly revenue.

-

Amex may verify your revenue by linking your business bank account.

-

Existing Amex customers may have an advantage.

That one-year business age requirement is important.

If you just formed your LLC yesterday, this probably is not the right product yet. You may need to focus on building revenue, opening business accounts, developing business credit, and creating a stronger lender profile first.

The FICO Requirement Has Changed Before

One thing I do not like about funding products is how quietly the rules can change.

According to the original content, this product previously had a lower FICO requirement around 620, but the current requirement discussed here is 660.

That is a big jump.

And this is why waiting can be dangerous.

Lenders tighten up. Requirements change. Score minimums move higher. Revenue requirements increase. Products that were easy to access last year can become much harder the next year.

That does not mean you should rush into a product you are not ready for.

But if you already qualify and the offer makes sense, it may be worth looking at before the requirements get tougher.

Existing Amex Customers Have an Edge

American Express is a relationship-driven lender.

If you already have Amex business credit cards, use them regularly, pay on time, and manage your accounts well, you may have a better shot at seeing a pre-approved offer.

That does not guarantee approval.

But it helps.

Amex already has internal data on you. They can see how you use credit, how you pay, and how long you have been in their ecosystem.

That is much better than applying as a complete stranger.

If you do not have an Amex relationship yet, it may be worth starting with an Amex business credit card and building history before trying for the line of credit.

How to Check for an Amex Business Line of Credit With No Hard Pull

This is the most important part.

Getting approved without a hard pull depends on using the right path.

If you manually apply the wrong way, you may trigger a hard credit inquiry.

The safer strategy is to check whether you are pre-approved through Amex instead of jumping straight into a full application.

One real data point from the original content said:

“They gave me a pre-approval last year. I nibbled at the time, and it was an instant approval—no HP, no docs.”

That is exactly what you want.

Pre-approval first. Full application only if the offer is there and the terms make sense.

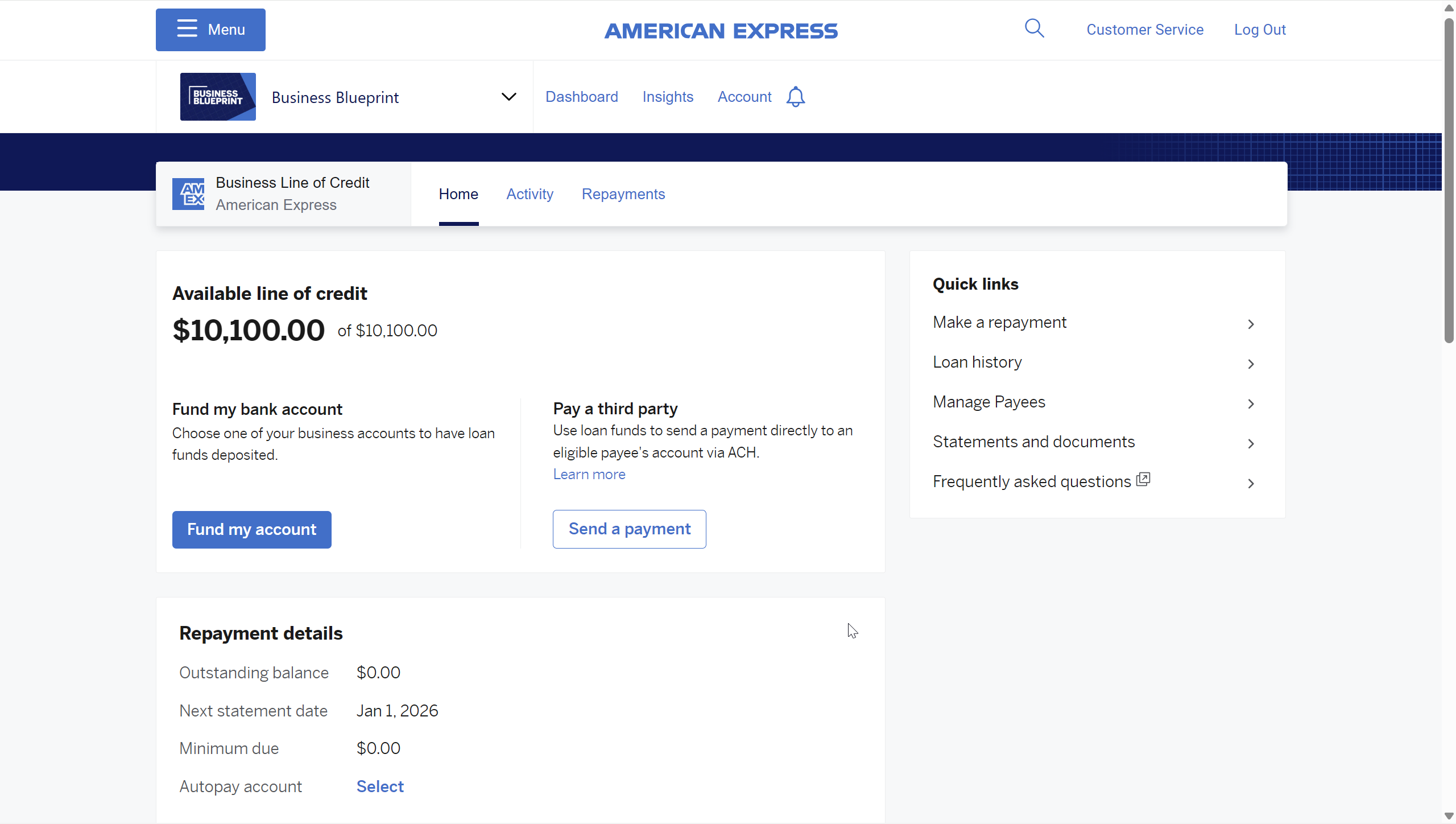

Step 1: Sign Up for American Express Business Blueprint

Before checking for a pre-approved offer, set up American Express Business Blueprint.

Business Blueprint is Amex’s business dashboard that connects business banking, cash flow tools, and credit products.

This is where Amex can evaluate your business profile and cash flow.

The key is to sign up using your existing American Express business credit card login if you already have one.

That matters because if you are already in the Amex ecosystem, you may be able to check offers tied to your existing relationship.

If you do not already have an Amex account, your path may be different, and you may face a higher chance of a hard pull later.

Step 2: Link Your Business Bank Account

Next, link your verified business bank account.

This is not just a random step.

Amex uses your business bank account to review your revenue and cash flow. If the minimum monthly revenue requirement is $3,000, Amex needs a way to verify that money is actually coming into the business.

Linking your account can help Amex see:

-

Monthly revenue

-

Cash flow patterns

-

Deposit activity

-

Business stability

-

Whether your revenue supports the requested funding

This is why having a real business bank account matters.

If your business finances are messy, mixed with personal expenses, or spread across too many accounts, you may make it harder for lenders to understand your business.

Helpful resource: If you are still building your business banking foundation, Bluevine Business Checking may be worth reviewing as part of your setup.

Step 3: Use the Pre-Approval Path, Not the Manual Apply Button

This is where people mess up.

Do not just hit “Apply Now” and hope for the best.

If your goal is to avoid a hard pull, you want to use the pre-approval path.

The original process was:

-

Log out of your Amex account.

-

Go back to the American Express website.

-

Find the Business Line of Credit page.

-

Choose the option to sign in and see whether you are pre-approved.

-

Use your existing Amex login.

-

Review the offer if one appears.

If you see a pre-approved offer, Amex may show you the credit limit they are willing to extend.

If you like the offer and accept it through the pre-approval path, that is where some business owners have reported approval with no hard pull.

But if you do not see an offer, do not force it.

Manually applying may trigger a hard inquiry.

That is the part you need to avoid if protecting your personal credit score is the priority.

My Amex Business Line of Credit Approval Data Point

Here is my personal data point.

I got approved for a $10,100 Amex Business Line of Credit just over one year into business.

At the time, my business was doing around $5,000 to $10,000 in monthly revenue.

That is important because it shows you do not necessarily need a massive, seasoned business doing millions per year to get considered.

But you do need real revenue.

This is not a “say whatever you want on the application” situation. Amex may verify your cash flow by connecting to your business bank account.

So if the revenue is not there, the offer may not be there either.

How Much Can You Get From the Amex Business Line of Credit?

The original content states that Amex credit limits may range from $2,000 to $250,000.

That is a massive range.

But most businesses should not expect the top number.

Banks often size business credit based on revenue, cash flow, existing relationship, payment history, and overall risk. A common rough estimate is that lenders may extend around 10% to 15% of yearly business revenue, but this can vary a lot depending on the lender and the product.

So if your business is doing $36,000 per year, do not assume you are getting $250,000.

That is not realistic.

Larger limits are usually reserved for businesses with stronger revenue, stronger financial history, and stronger relationships with Amex.

How Fast Does Amex Deposit the Funds?

Once approved, Amex can move quickly.

According to the original content, funds may be deposited within 1 to 3 business days to a verified business bank account or vendor account.

If you use an Amex Business Checking account, funds may be deposited instantly.

That speed can matter if you need working capital fast.

But fast money is still debt.

Before taking a draw, make sure the repayment schedule actually works for your business.

What If Your LLC Is Too New?

If your LLC is too new for the Amex Business Line of Credit, do not panic.

You may need to build the foundation first.

That can include:

-

Opening a real business checking account

-

Separating business and personal finances

-

Building consistent monthly revenue

-

Establishing vendor accounts

-

Opening starter business credit cards

-

Keeping clean payment history

-

Building a relationship with business-friendly banks

-

Preparing business documents before applying for funding

This is not as exciting as getting approved today.

But this is how you become fundable.

A lot of business owners want the funding before the foundation. That is backwards.

The better move is to build the business profile first, then apply when lenders can actually say yes.

Helpful Resource: If your business is new and you need a stronger funding foundation, the Fundable Business Plan Template can help you organize your business before approaching lenders.

What to Do Before Applying

Before you check for an Amex Business Line of Credit offer, make sure your profile is ready.

Here is the simple checklist:

-

Make sure your business is at least one year old.

-

Confirm your personal FICO score is strong enough.

-

Make sure your business is generating consistent monthly revenue.

-

Use a real business bank account.

-

Keep your business and personal finances separate.

-

Build or strengthen your Amex relationship.

-

Check for pre-approval before manually applying.

-

Avoid the manual application path if you are trying to avoid a hard pull.

-

Review the repayment terms and loan fees before accepting a draw.

The goal is not just to get approved.

The goal is to get approved without damaging your credit and without taking funding your business cannot comfortably repay.

Frequently Asked Questions

Does the Amex Business Line of Credit do a hard pull?

It may be possible to get approved with no hard pull if you are already an Amex customer and accept a pre-approved offer through the correct path. But if you manually apply without a pre-approval, you may trigger a hard inquiry. Always read the language carefully before submitting.

What credit score do you need for the Amex Business Line of Credit?

Based on the original content, Amex may require a personal FICO score of at least 660. Requirements can change, and Amex may also consider your existing relationship, business revenue, and account history.

Can a new LLC get an Amex Business Line of Credit?

A brand-new LLC likely will not qualify if Amex requires at least one year in business. However, a newer LLC that is over one year old, has consistent revenue, and has an Amex relationship may have a better shot.

How much revenue do you need for the Amex Business Line of Credit?

The original content says the business must generate at least $3,000 per month in revenue. Amex may verify this by linking your business bank account, so the revenue needs to be real and visible.

Is the Amex Business Line of Credit revolving?

Not in the traditional sense. Each draw works more like a separate loan with its own repayment schedule. That is why some people say it behaves more like an installment loan than a true revolving business line of credit.

How fast does Amex fund the business line of credit?

According to the original content, funds may arrive in 1 to 3 business days after approval. If you use an Amex Business Checking account, funding may be instant.

Conclusion

The Amex Business Line of Credit can be a strong option for business owners who want access to working capital without taking an unnecessary hard pull.

But the path matters.

Do not blindly hit “Apply Now.” If you already have an Amex relationship, set up Business Blueprint, link your business bank account, and check for a pre-approved offer first.

That is how you give yourself the best shot at funding without damaging your personal credit score.

Just remember: this product is not a perfect traditional revolving line of credit. Each draw has its own repayment structure, and you need to understand the fees before taking the money.

Business funding is powerful when your foundation is ready.

It is dangerous when it is not.