I Got $54,500 in Credit Card Approvals, But the Real Lesson Was Credit Union Underwriting

Jun 25, 2026

Four banks and credit unions approved me for $54,500.

But what happened afterward completely changed how I look at underwriting.

After testing six different lenders, I’m starting to believe a lot of credit unions have a serious false limit problem.

That means the number you see on the screen during the application process may not always be the real final limit.

Sometimes it is real.

Sometimes it changes.

And sometimes underwriting comes back after the “approval” asking for enough paperwork to make it feel like you accidentally applied for a mortgage.

In this article, I’m going to break down:

-

Which banks and credit unions approved me

-

Which lenders pulled Equifax

-

Which lenders pulled TransUnion

-

Which credit union took me from $500 to $10,000 before the card arrived

-

Why I no longer trust every limit that appears during a credit union application

Disclosure: This article may contain affiliate links, which means I may earn compensation if you click or apply through certain links.

Before applying for any new credit card, it may be worth checking whether you are pre-approved first so you can avoid unnecessary hard pulls when possible.

My Credit Profile Before Applying

Before getting into the results, here is the profile I was applying with.

Equifax FICO 8: 782

Credit utilization: 3%

Oldest account: 17 years, 3 months

Average age of accounts: 5 years, 8 months

Recent inquiries: About 5 in the last six months on TransUnion

In other words, this was not a rebuilding profile.

This was a strong credit profile.

Low utilization.

Long credit history.

Solid score.

And even with that, two credit unions still pushed me into extensive manual underwriting.

That was one of the biggest surprises from this entire experiment.

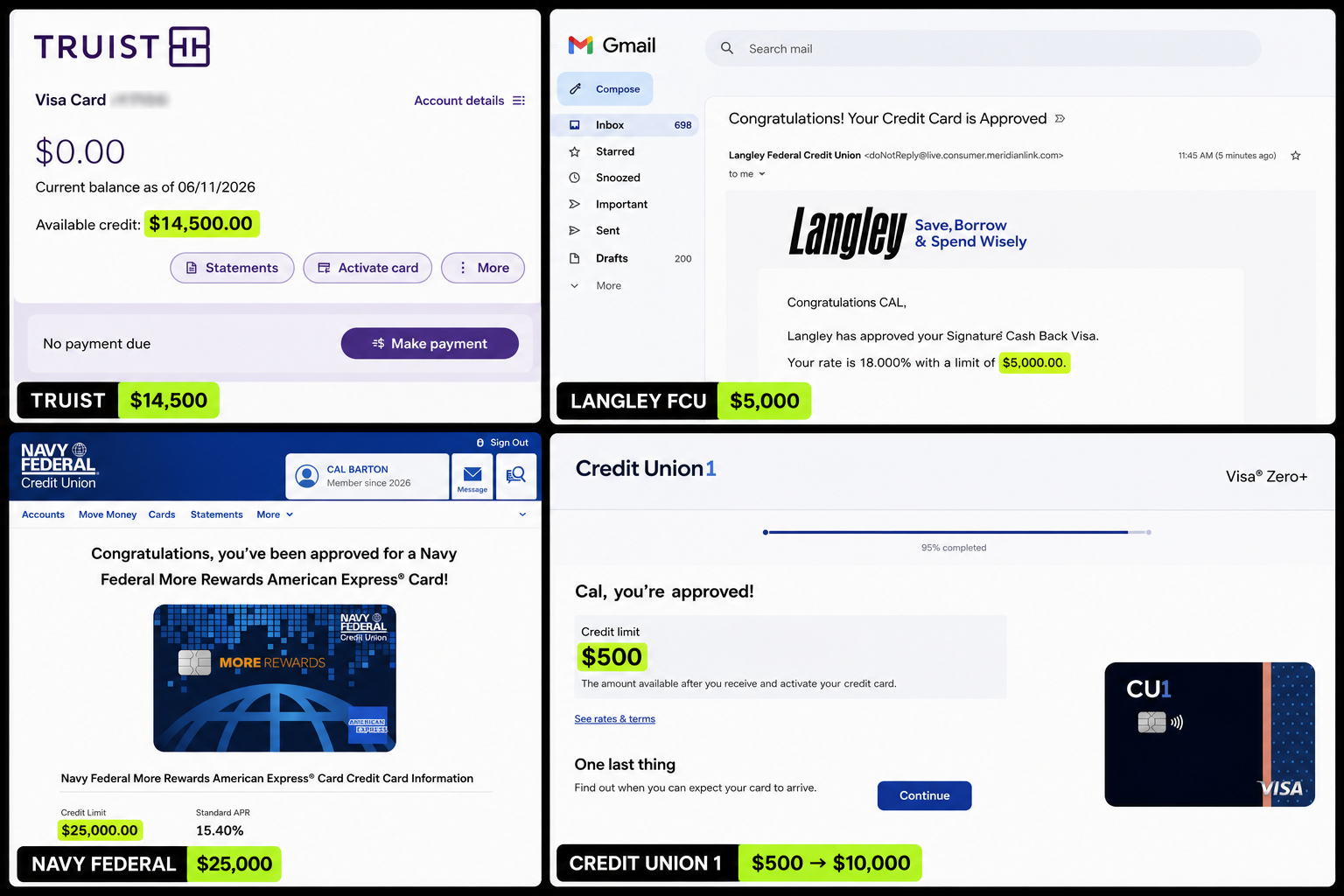

The Final Credit Card Approval Results

Here is the quick breakdown.

Approved

Truist: $14,500 business credit card approval

Langley Federal Credit Union: $5,000 approval

Credit Union 1: $500 approval, later increased to $10,000

Navy Federal Credit Union: $25,000 approval

Total approved credit:

$54,500

What Pulled Equifax?

These lenders pulled Equifax:

-

Truist

-

Langley Federal Credit Union

-

Credit Union 1

-

Pelican State Credit Union

What Pulled TransUnion?

These lenders pulled TransUnion:

-

Navy Federal Credit Union

-

BECU

But the approval amounts only tell part of the story.

The real lesson came from what happened after the applications.

Truist: Relationship Banking Still Matters

Truist gave me one of the clearest lessons from this entire test.

I opened a Truist business checking account back in December.

At first, I applied with roughly $100 sitting in the account.

Denied.

No major explanation.

Instead of forcing it, I left the account alone.

A few months later, I deposited around $8,000 from a business payment and let the money sit for roughly two weeks.

Then I applied again.

This time, I was approved for $14,500 on the Truist Business Cash Rewards card.

Same business.

Same owner.

Same credit profile.

Different banking relationship.

That is why I still believe deposits matter with certain banks, especially when you are applying for business credit products.

Sometimes the bank does not just want to see your credit profile.

They want to see activity.

They want to see deposits.

They want to see a reason to deepen the relationship.

That does not mean deposits guarantee approval.

But in my case, the difference was obvious.

Langley Federal Credit Union: The Surprise Winner

Langley Federal Credit Union was one of the most pleasant surprises from this test.

I only deposited around $100 into checking and another $100 into savings.

That was it.

Nothing crazy.

Nothing complicated.

Then a concierge representative reached out to introduce themselves and offered to answer questions.

That level of service immediately stood out.

I applied for the Langley Signature Cash Back card and was approved for $5,000.

No drama.

No document requests.

No weird underwriting surprises.

Just a normal approval.

Honestly, if every credit union worked like Langley, this article would be a lot shorter.

Credit Union 1: The Weirdest Approval

Credit Union 1 gave me the weirdest approval of the entire experiment.

I did not even have a bank account with them.

Never opened one.

Still have not.

Their card is backed by Elan Financial, and they offer a pre-approval tool.

So I checked the pre-approval.

Then I applied.

And I got approved for…

$500.

Not exactly exciting.

But then a few days later, before the card even arrived, I received an email saying my limit had been increased to $10,000.

That is a massive difference.

And it told me something important.

The first number is not always the final number.

Sometimes that works against you.

Sometimes it works in your favor.

In this case, Credit Union 1 turned a boring $500 approval into a $10,000 credit limit before I even had the card in my hands.

Navy Federal: The Biggest Clean Approval

Navy Federal gave me the biggest clean approval.

I had around $1,000 in deposits and one direct deposit hit the account before applying.

Nothing crazy.

Nothing complicated.

They pulled TransUnion and approved me for $25,000 on the Navy Federal More Rewards card.

No document chase.

No tax returns.

No underwriting scavenger hunt.

Just a normal approval process.

Compared to what happened with some of the other credit unions, that simplicity was very attractive.

Navy Federal was not the most complicated application.

It was not the messiest.

It was not the one with the most back and forth.

It was just the biggest clean approval.

And sometimes, that matters more than people realize.

The Credit Union False Limit Problem

This was the biggest lesson from the entire experiment.

Let’s talk about Pelican and BECU.

At first glance, both looked like wins.

Pelican showed me a $5,000 approval amount.

BECU showed me a $10,000 approval amount.

Most people would see those numbers and assume the deal is done.

But that was not true.

At least not in my experience.

Those numbers were not final.

They were not clean approvals.

They were not “card is on the way” approvals.

They were more like placeholders before manual underwriting really started.

That is what I call the credit union false limit problem.

Pelican State Credit Union: The Paperwork Started After the Approval

Before applying with Pelican, I deposited $1,000 into my account and let the relationship sit for about one week.

Then I applied.

At first, Pelican showed me a $5,000 approval amount.

That looked like a win.

But a few days later, underwriting contacted me.

They noticed a few inquiries.

They wanted explanations.

Then they determined I was self-employed.

And for the first time I can remember on a credit card application, being self-employed became a major issue.

Next thing I know, they were asking for:

-

Two years of tax returns

-

Twelve months of business bank statements

For a credit card.

Not a mortgage.

Not a business loan.

A credit card.

And remember, I already had money on deposit with them.

At that point, I was out.

I am not saying Pelican did anything wrong by verifying information.

Credit unions are allowed to underwrite their own way.

But from a consumer perspective, that did not feel like a normal credit card approval process.

It felt like a much bigger financial application.

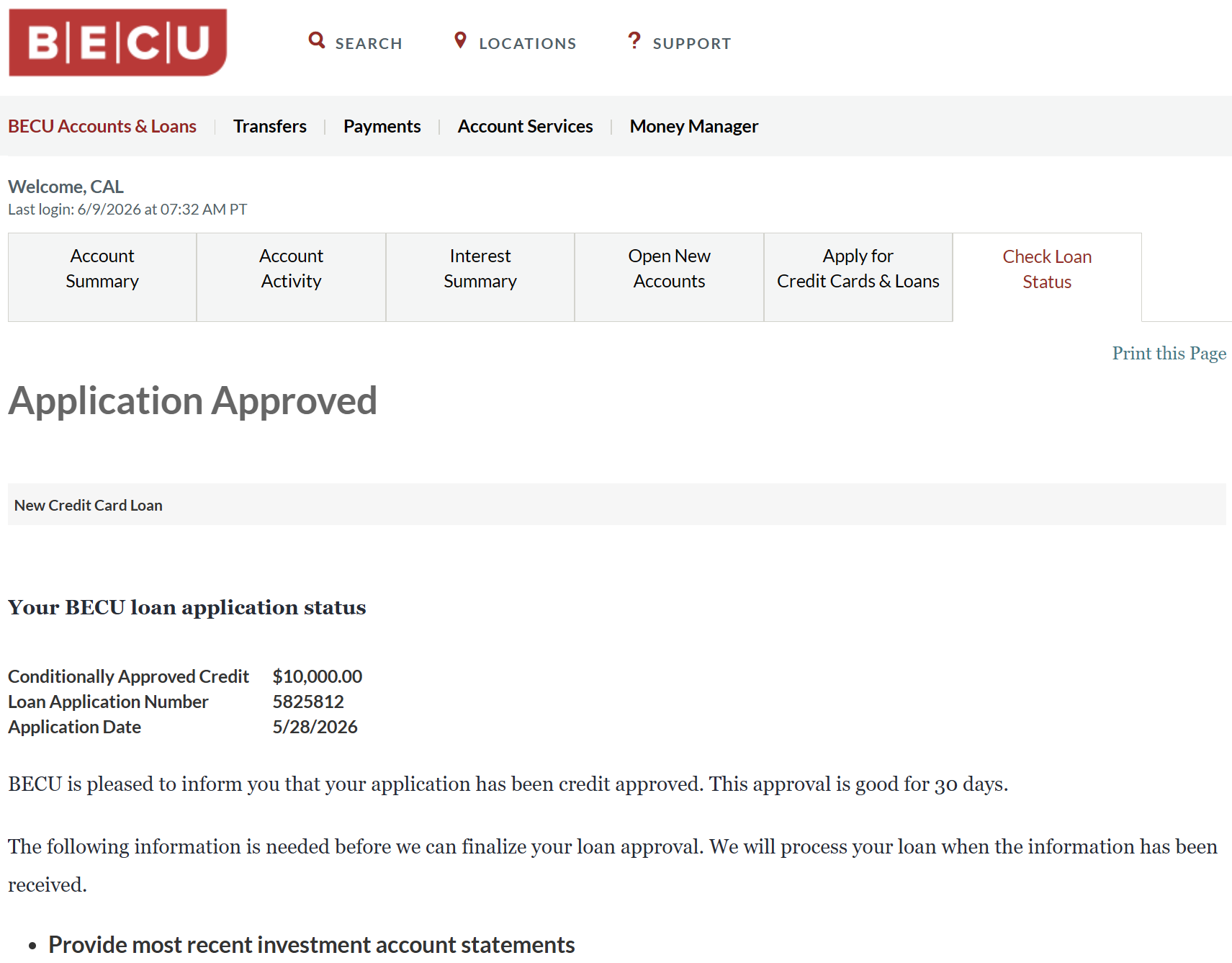

BECU: Even More Documentation

BECU was even worse.

Before applying, I deposited $700 into the account and waited about one month before submitting the application.

They also became the only credit union I have ever joined that required me to call in just to set up external bank transfers.

Honestly, it still boggles my mind that external transfers are not enabled by default in 2026.

Then the underwriting requests started.

They wanted:

-

Two recent pay stubs

-

Two years of W-2s

-

Investment statements

-

Proof of address

-

Copies of my Social Security card

Again…

For a credit card.

Not a business loan.

Not a mortgage.

A credit card.

At that point, I withdrew my money and moved on for now.

Why I Call These “False Limits”

Some people may disagree with me here.

That is fine.

But personally, I do not fully trust the initial limit many credit unions show during the application process.

Not until underwriting is complete.

Not until documentation is complete.

Not until the card is actually on the way.

Because what good is a $10,000 approval amount if underwriting can still come back and ask for a mountain of paperwork?

What good is a $5,000 approval amount if the real decision has not been made yet?

To me, those numbers are not fully real yet.

They are provisional.

They are preliminary.

They are what I call false limits.

And I have seen enough data points online to know this is not unique to me.

Some people see the amount stay the same.

Some see it increase.

Some see it decrease.

Some get fully approved.

Some get denied.

The point is simple:

The first number is not always the final answer.

What Credit Unions Do Not Always Make Clear

I was already aware of this issue before running this test.

But these applications made it painfully clear how common it can be.

Many credit unions use modern software on the front end.

The application feels fast.

The interface feels modern.

The approval message may arrive quickly.

You might even see a credit limit on the screen and think you are done.

But then the application disappears into a manual underwriting department.

And that is where the real process begins.

You may get calls.

You may get texts.

You may get emails.

You may have to explain inquiries.

You may have to verify income.

You may have to send documents.

You may have to wait for someone in underwriting to manually review your file.

And if you miss a message, your application can just sit there.

For days.

Sometimes weeks.

What surprised me most was not that underwriting existed.

It was how often the initial approval seemed more like a placeholder than a final decision.

The real approval process did not begin when I submitted the application.

It began after the application left the automated system and landed on someone’s desk.

So if you are applying with credit unions, understand this:

The application is not always over just because you see a number on the screen.

In some cases, it is only beginning.

Why Credit Union Applications Can Feel Different From Big Bank Applications

One reason credit union applications can feel different is because many of them are more relationship-driven.

That can be a good thing.

Some credit unions may be willing to approve people that larger banks ignore.

Some may offer strong limits.

Some may pull a different bureau than the major banks.

Some may care about deposits, membership history, direct deposit, or how long you have been with them.

But the tradeoff is that some credit unions can also be more manual.

More document-heavy.

More conservative after the automated system gives an initial response.

That is why I think people need to separate the front-end approval from the back-end underwriting.

The front end may say one thing.

The underwriter may say another.

And until both sides are complete, I would be careful about celebrating too early.

The Best Lessons From This $54,500 Credit Card Test

Here are the biggest takeaways from this entire experiment.

1. Deposits can matter

With Truist, the difference between my first denial and later approval appeared to be the relationship.

I applied early with roughly $100 in the account and got denied.

Later, after depositing around $8,000 and letting it sit for about two weeks, I was approved for $14,500.

That does not mean deposits guarantee approval.

But it does show why relationship banking can matter.

2. Not all credit unions are difficult

Langley was smooth.

Navy Federal was smooth.

Credit Union 1 was weird, but it worked out.

So this is not about saying every credit union is a problem.

That is not true.

The real point is that credit union underwriting can vary a lot.

One credit union may approve you cleanly.

Another may ask for tax returns, bank statements, pay stubs, W-2s, proof of address, and more.

3. The first credit limit may not be final

Credit Union 1 started at $500, then moved to $10,000 before the card arrived.

Pelican showed $5,000, then pushed me into heavy documentation.

BECU showed $10,000, then requested a long list of documents.

That is why I call this the false limit problem.

The first number is not always the final answer.

4. Bureau pulls matter

For me, Truist, Langley, Credit Union 1, and Pelican pulled Equifax.

Navy Federal and BECU pulled TransUnion.

That matters because if one credit bureau has too many recent inquiries, you may want to be more careful about which lenders you apply with.

In my case, I already had about five recent TransUnion inquiries in the last six months.

So knowing which bureau a lender is likely to pull can make a big difference.

5. Strong credit does not always prevent manual underwriting

This was the biggest surprise.

I had a 782 Equifax FICO 8 score, 3% utilization, a long credit history, and still got pushed into serious manual underwriting with some credit unions.

That tells me strong credit helps, but it does not always remove friction.

Especially if the lender has concerns about inquiries, self-employment, income verification, or identity documentation.

Helpful Resource for Credit Union Research

There are still a lot of credit unions across the country that may allow people outside their immediate local area to become members.

The hard part is knowing which ones are open to broader membership, which bureaus they may pull, and which products are worth looking at.

Helpful resource: My 150+ Credit Unions Anyone Can Join Database is built for people who want to research credit unions, membership options, bureau pulls, and potential high-limit credit card opportunities.

The Bottom Line

This $54,500 credit card approval test taught me a lot.

Truist reminded me that banking relationships can still matter.

Langley showed me that some credit unions still know how to make the process simple.

Credit Union 1 reminded me that a low starting limit is not always the end of the story.

Navy Federal gave me the biggest clean approval.

But Pelican and BECU changed how I look at credit union underwriting.

Because now, when I see a credit union show an approval amount during the application process, I do not automatically assume the deal is done.

Not until underwriting is finished.

Not until documents are cleared.

Not until the card is actually on the way.

That is the real lesson.

A credit limit on the screen can look exciting.

But with some credit unions, that number may only be the beginning of the process.

Not the end.